Analysis

April 6, 2025

Final Thoughts

Written by David Schollaert

Well, it certainly seems that “Liberation Day” lived up to the hype. I’m not talking just about the White House Rose Garden press conference but also the aftermath.

This week’s steel market survey – which closed before Trump kicked off his presser on Wednesday afternoon detailing reciprocal tariffs on imports – indicated that steel was already on shaky ground. And that was before the stock market turmoil on Thursday and Friday.

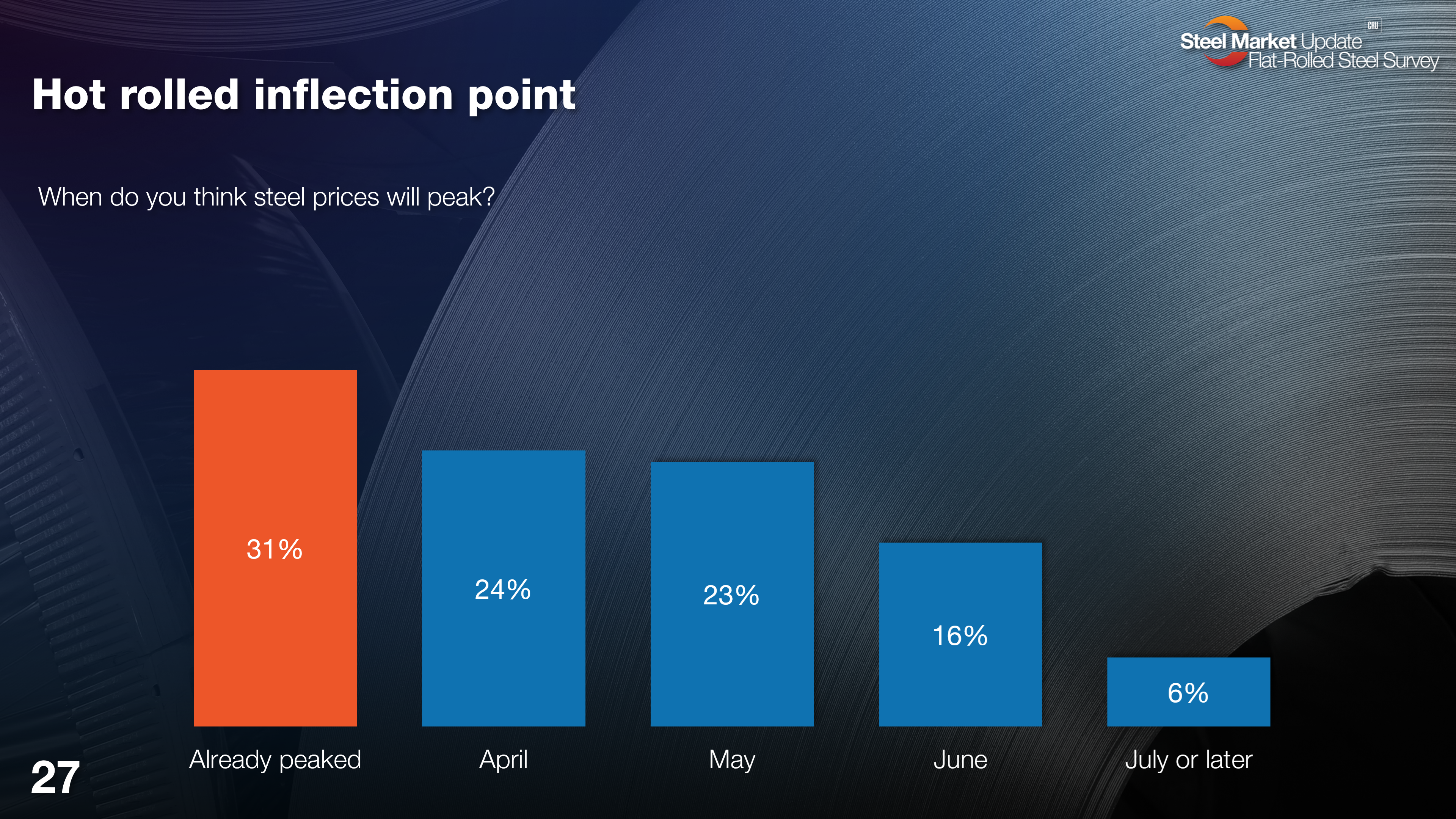

Steel Buyers’ Sentiment is down – both buyers’ current and future outlooks slipped – and most think prices have already peaked. That’s a significant shift from just two weeks earlier, when 61% of respondents thought prices would peak come May or later.

And lead times are slightly shorter, while mills are less willing to negotiate. That doesn’t typically happen. Either lead times should stretch out, or mills should become more willing to negotiate. Let’s just say the impact of tariffs on steel remains unclear.

More people are on the sidelines after loading up ahead of higher prices backed by the threat of tariffs. And with just 25% tariffs on steel and no quotas under Section 232, imports are more attractive than they had been.

There’s a lot to unpack in our latest flat-rolled steel survey data, so be sure to check it out here. And here’s a bit of what stood out to me. I’ll give the results and participant comments a chance to do the talking.

Survey says doubts have crept in

For starters, just two weeks ago less than 8% of you thought the price had or would peak in March. Now about 31% think they’ve already peaked, with another 47% thinking it will happen between now and May. Very few believe the market will have legs come summer. (Editor’s note: You can click on any of the images below to expand them.)

Here is what some survey respondents had to say:

“Ongoing uncertainty provides an opportunity for price increases.”

“Price rise for another month and a half.”

“Core trade cases and reciprocal tariffs will tighten the steel markets.”

“If tariffs stay, steel will continue to climb until you reach the offset in change plus tariffs.”

“It seems to be running out of steam. Customers are willing to wait until they see prices come down.”

“Demand will not support many more increases.”

“Even though this feels purely ‘supply-driven,’ that doesn’t mean it isn’t real.”

“We have not felt the full impact of the redefined steel tariffs and the anti-dumping suits are right around the corner.”

“Think we are close, a lot of steel on order but excitement has died off.”

“Tariffs, and seasonality.”

“No major uptick in real demand.”

$1,000/ton – not for a while?

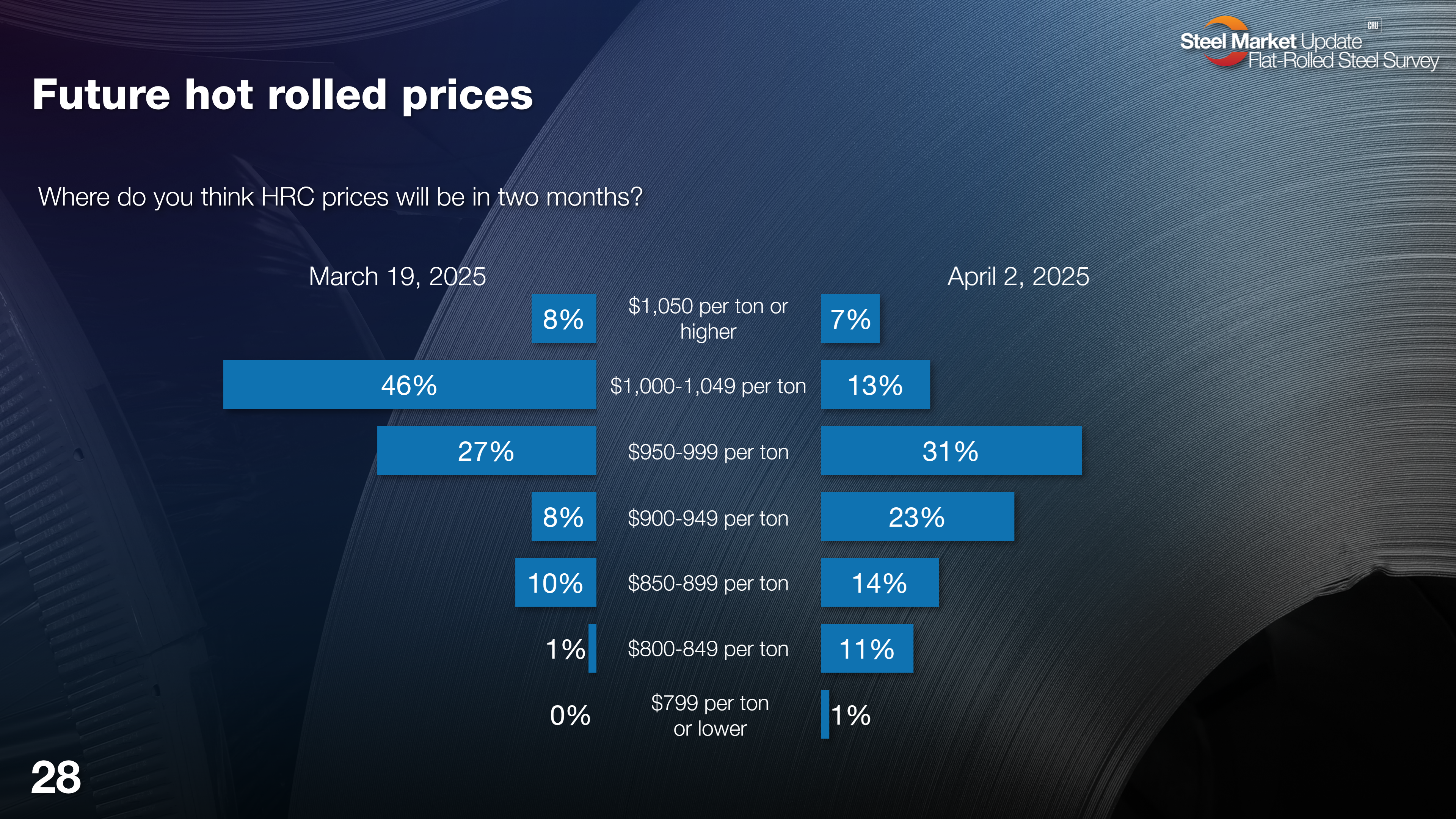

Not surprisingly, the view of where prices will be in two months from now has shifted as well. Just a couple of weeks ago, close to half of you saw prices at or slightly above $1,000 per short ton (st). That has shifted. Now just about 20% of you still think that could happen.

The wisdom of the crowd says hot band will be roughly where it is now – SMU’s average domestic HR price was $915/st as of April 1, down $30/st vs. the previous week – or lower come June.

And what some had to say:

“Peak in late April/early May and then drop off a bit through May. Larger drop in June.”

“This is the goal I feel the mills want.”

“Similar pattern to 2018.”

“Tariff resolved and demand returns to an unpanicked state.”

“Mills will push it until the market will not support.”

“Lack of demand.”

“We are anticipating a bit more of a run. We are also expecting a pretty epic collapse heading into the summer months too.”

“Mills grabbing all they can.”

“Unsettled trade wars.”

“Plenty of supply weak demand.”

“Demand fundamentals are still weak, or weaker than before.”

Steel buyers agree… mostly

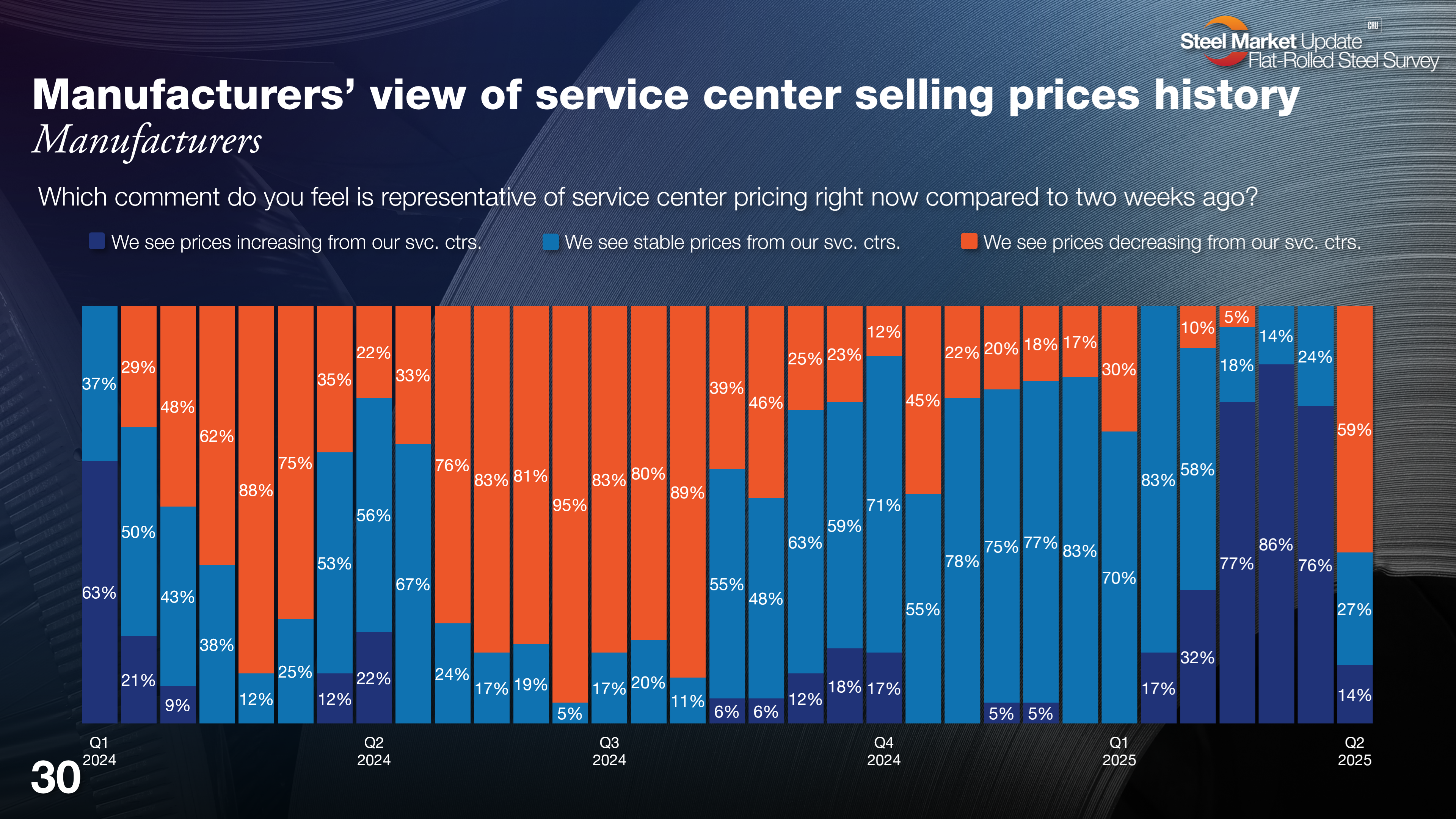

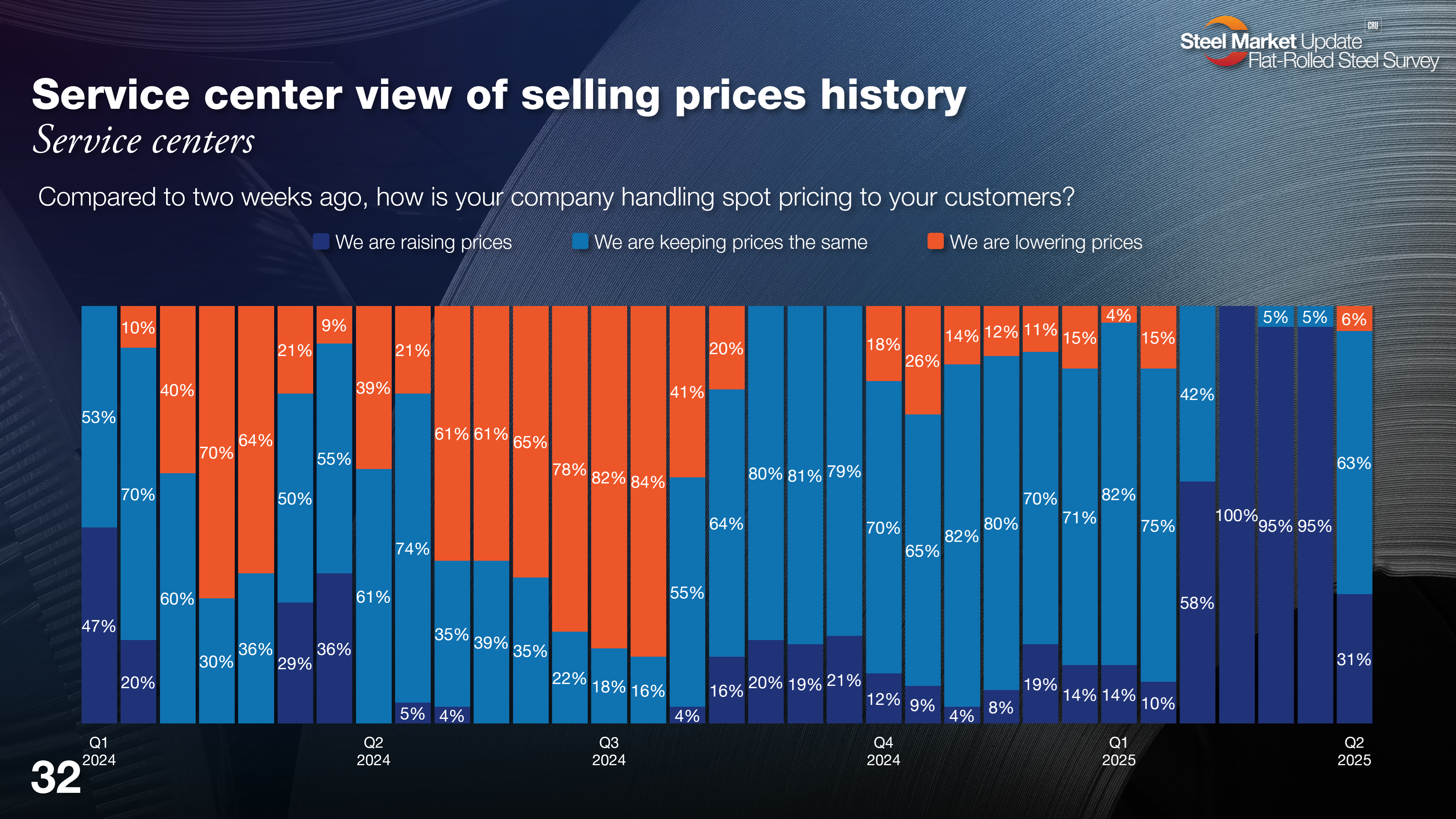

Service centers and manufacturers alike (next two charts) are reporting a significant pivot in pricing. I don’t think we’ve seen a reversal quite like this over just a couple of weeks (each bar is two weeks).

In early/mid Q1, mills began pushing prices higher, supported by tariffs. Once buyers covered near-term needs, concerns shifted to uncertainty around some of those same tariffs. Buying tailed off, and so did prices.

A few comments:

“Pricing is still headed up at a pretty good pace from SSCs. However, they seem willing to negotiate if you balk at the price.”

“We have raised prices once in the last two weeks.”

“Competitors need to stop selling on a cost + model and start to look at replacement costs or they will get stuck restocking at a much higher level.”

“So many increases so fast have caused panic buying, and I think mills are in a comfortable spot now to let things plateau.”

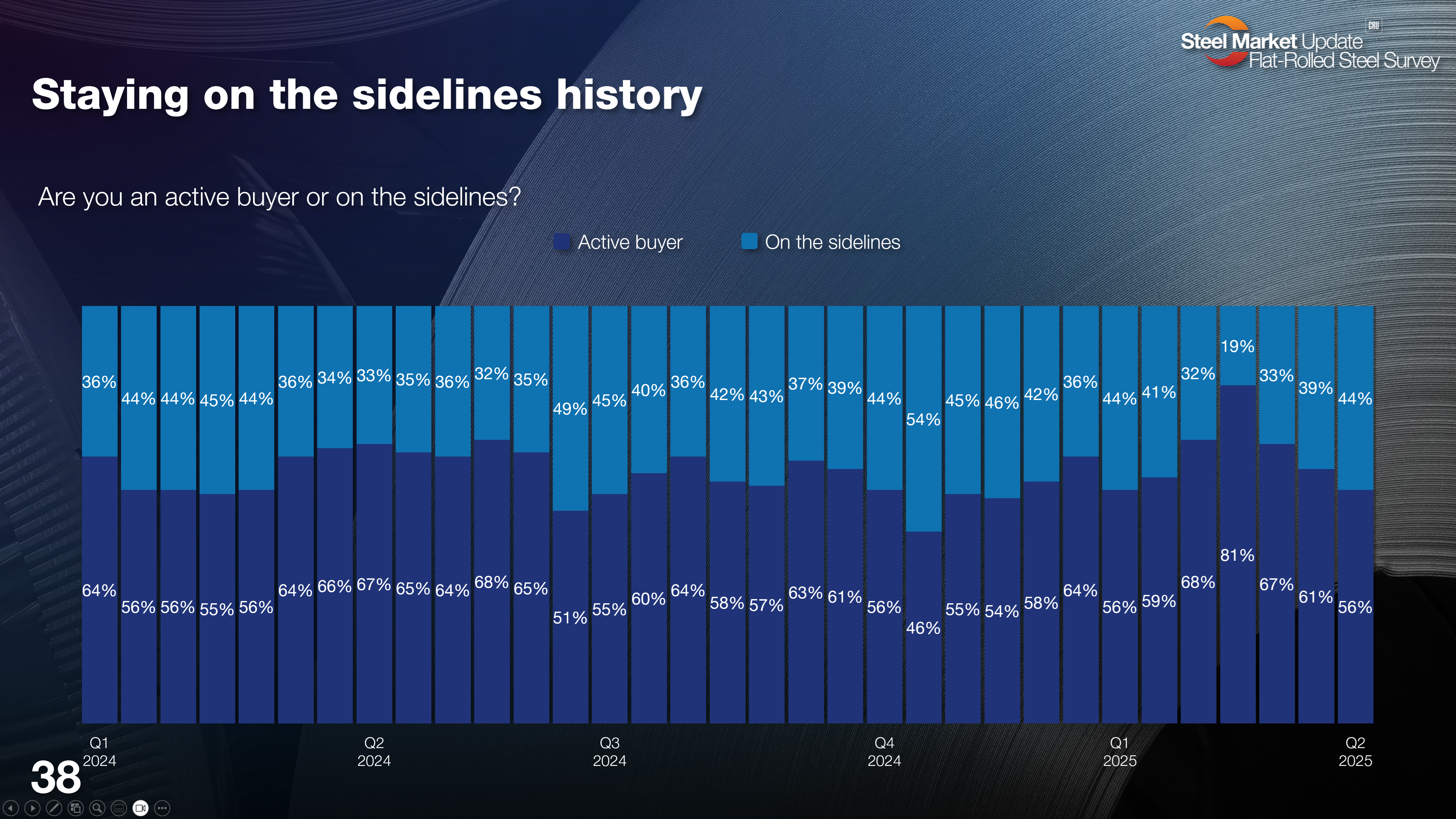

Comfort on the sidelines?

The span of the past seven surveys depicts so well what we’ve seen play out in the market since early Q1. We saw an upswing of buyers came off the sidelines just before swinging back, and many are now just waiting it out.

Here is what some survey respondents had to say:

“Active for back-to-back contracts.”

“We bought heavy before pricing went up. We are only buying to fill small needs that might pop up.”

“Active, but only for what we need according to current lead times.”

“Always buying, but being held close to the minimum with most mills.”

“Maintaining inventory.”

“As needed.”

“Just based on the pricing, we are hand-to-mouth. And if we can use secondary/excess, we most certainly are.”

“We’re only buying what we can secure customer orders for at this moment.”

“After the initial flurry, things have slowed a bit.”

“Only buying per job.”

“Just buying to run at minimal inventory levels.”

“We are not a buyer.”

Imports, even more appealing?

And while reciprocal tariffs on imports were detailed on April 2, they don’t apply to Canada and Mexico, at least not yet. Imports of steel, aluminum, autos, and auto parts are also excluded since they are subject to Section 232 tariffs.

And with US prices high, 25% Section 232 tariffs, and no quotas, imports are more attractive than they had been.

Here is what some survey respondents had to say:

“The spread between domestic and foreign is too big even after paying tariffs.”

“Domestic suppliers continue to raise prices, so it is still cheaper to go offshore rather than buy domestic. The lead times are a little further out, but even with the tariffs, foreign is still cheaper for the most part.”

“Pricing is back to being good on imports. Delivery dates are still lousy, though.”

“New numbers for offshore are attractive, but who knows what will happen with tariffs and/or potential quotas. Still, too much risk involved for our company to source foreign steel.”

“Hit or miss from different countries and varying pricing. The market is still trying to figure out where things will settle.”

Steel 101 Workshop

If you’re new to the industry, have a few new joiners, or just want a refresher on all things steel, don’t miss our next Steel 101 workshop coming up in June.

We will once again converge in Memphis, Tenn., with the date set for June 10-11, 2025. The workshop includes a guided mill tour of Nucor Steel Arkansas. You can get more info and register here.

As always, all of us here at Steel Market Update truly appreciate your business.