Prices

March 27, 2025

HR Futures: Correction in market after big rally

Written by Daniel Doderer

Another eventful week in the physical and financial steel markets is coming to a close, but with a markedly different tone than the last update at the end of February.

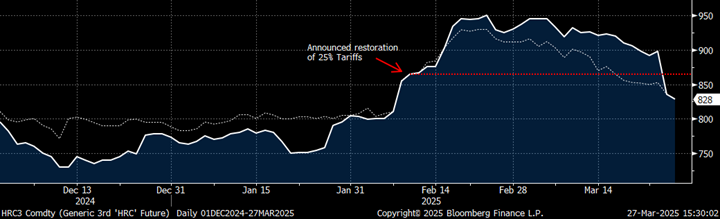

After an incredible rally in futures pricing that saw steel contracts rise sharply, the past two weeks have brought a notable correction. The 3rd Month future (currently the June contract) fell nearly 11% from its peak on Feb. 25, settling at $828 as of the Thursday, March 27, close. While some retracement was expected given the rapid pace of ascent, the swiftness of this decline has caught many market participants off guard.

The first chart below highlights just how sharply the futures have adjusted, with the June contract now trading nearly $40 below where it was on the day that steel and aluminum tariffs were announced (Feb. 11). This correction follows a period in which near-term contracts (3rd Month, solid white) surged above $900, marking a rare instance where futures led the physical market higher.

However, the latest price action suggests a market recalibration to global realities, rather than a full-scale reversal.

Rolling 3rd Month future (white, solid), June ’25 future (white, dotted)

While physical market pricing has also lost some momentum, current spot market indications are currently reported to be higher than all open futures contracts.

Reports suggest that mills maintain price levels above all outstanding futures positions, highlighting a disconnect that could lead to further volatility if arbitrage opportunities emerge. Unlike prior corrections, where sharp futures declines often preceded broader physical market weakness, the current pullback has yet to fully translate into comparatively lower transaction values for spot steel. This raises questions about whether the futures market has overshot to the downside or if physical prices will eventually follow suit.

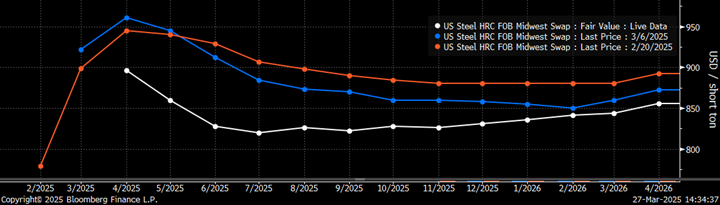

Interestingly, the market technically remains in a state of backwardation with the current settled futures curve in white, reflecting continued expectations of near-term tightness. However, the extent of the curve’s inversion has narrowed along with the sell-off. This reinforces the notion that some of the bullish enthusiasm seen a few weeks ago may have been overdone. Whether this signals the beginning of a prolonged consolidation phase or simply a pause before the next leg higher remains to be seen.

CME Midwest HRC futures curve (March 27 in white, March 6 in blue, Feb. 20 in orange)

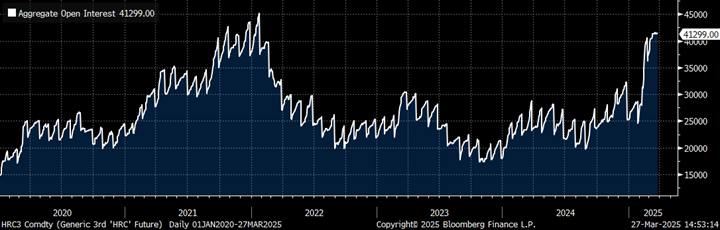

Another unexpected development has been the behavior of open interest in CME Midwest HRC Futures (below). Open interest represents the total number of outstanding futures contracts that have not been closed, liquidated, or delivered. It is an important indicator of market participation and liquidity, as rising open interest typically signals fresh buying or selling, while unchanged levels suggest that existing positions are merely shifting hands or contract months without new commitments.

Aggregate open interest CME Midwest HRC futures

Despite the significant price action, open interest has remained essentially unchanged over the last three weeks. Such a dynamic is unusual in a period of such heightened volatility, where sharp moves typically coincide with either speculative positioning or increased commercial hedging. Taking a step back, liquidity remains elevated, and the lack of fresh positioning in futures could simply echo the wait-and-see approach seen by many in the physical market.

At this stage, the critical question is whether the recent correction represents a necessary cooling-off period or the early stages of a broader downturn.

Given the relative resilience of physical spot prices, a technically tighter supply side (imports and domestic production not yet responding to higher prices), and the absence of major structural souring of demand, one could make a case that futures should be supported at these levels. That said, with markets adjusting to new realities, participants and observers should brace for further volatility and heightened uncertainty in the weeks ahead, while the new administration’s policies are cemented in.

With demand still expected to improve throughout most of 2025 and key global pricing dynamics still in play, the coming weeks will be crucial in determining whether this pullback is noise, or a signal that the fundamentals are not as stable as once thought.

Disclaimer: The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Flack Global Metals or Flack Capital Markets should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.