Market Data

March 20, 2025

SMU Survey: Mills hold firm on price, little negotiation room for buyers

Written by Brett Linton

The majority of the steel buyers responding to our latest market survey continue to report that domestic mills remain firm on pricing, showing little willingness to talk price on new spot orders this week.

Following President Trump’s tariff actions and rising mill prices, negotiation rates plummeted in mid-February and reached a near-two-year low by early March. This week, negotiation rates have marginally increased but remain on the low side.

Every two weeks, SMU surveys thousands of steel buyers asking if domestic mills are willing to negotiate price on new orders. As shown in Figure 1, just 32% of respondents this week said that mills were negotiable. While this rate is 18 percentage points higher than our early-March survey, it remains below most of the rates observed over the past two years. Recall that until January, buyers had previously held the bargaining power for nearly a year.

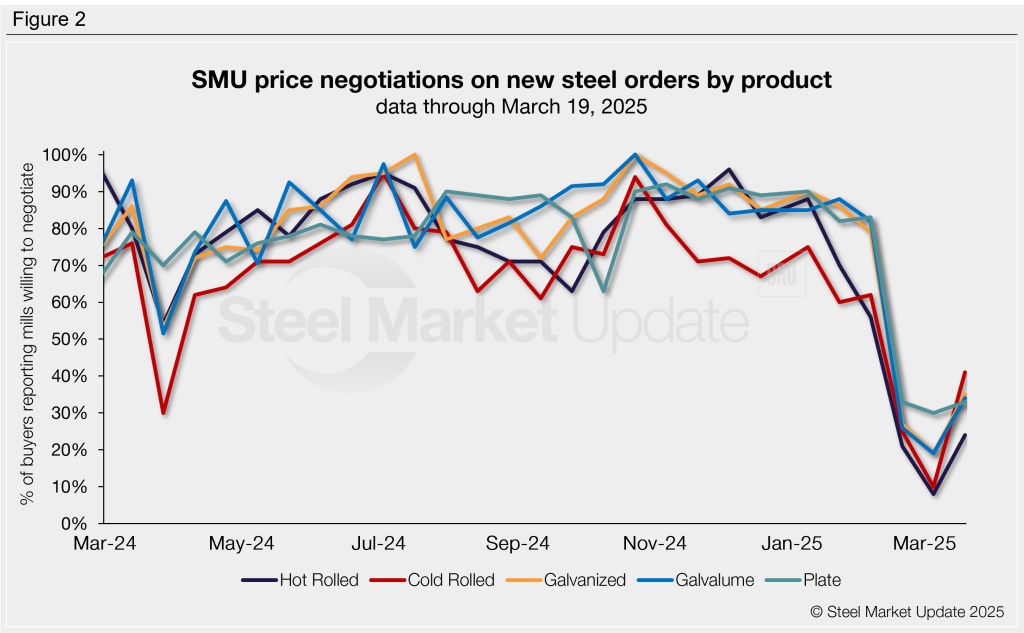

Negotiation rates by product

The lowest negotiation rates this week were on hot-rolled products. Just two weeks ago, negotiation rates for all sheet and plate products we track dropped to their lowest levels in over a year (Figure 2). Rates this week are as follows:

- Hot rolled at 24%, a 16-percentage point increase from the three-and-a-half-year low recorded on March 5.

- Cold rolled at 41%, recovering 31 percentage points from a one-year low.

- Galvanized at 35%, rising 16 percentage points from a three-year low.

- Galvalume at 34%, up 15 percentage points from a one-year low.

- Plate at 33%, a modest three percentage point rise from a near-two-year low.

Steel buyer remarks:

“Mill wouldn’t extend spot at the time but will offer/ work with us in the future. Very tight on [plate] supply.”

“Not on galvanized, lots of talk about how full the mill is with still relatively short lead times.”

“Depends on who you are and how much you are buying.”

“Negotiable [on hot rolled], they need volume.”

Note: SMU surveys active steel buyers every other week to gauge their steel suppliers’ willingness to negotiate new order prices. The results reflect current steel demand and changing spot pricing trends. Visit our website to see an interactive history of our steel mill negotiations data.