Final Thoughts

March 2, 2025

Final Thoughts

Written by David Schollaert

Trade policy and rapid run-up in steel prices have taken center stage lately. But scrap remains its own pandora’s box.

Input costs have been driven higher by tighter supplies and restricted flows after a tough winter. Could rising demand from mills fuel an extended rally into Q2?

Already, shredder feed has been strained as shredders try to fill backlogs. And shredded prices could jump by $50 per gross ton (gt) this month, some suggest.

It’s a similar story with prime grades. Industrial generation is down, and hot-rolled coil production is picking up.

SMU Scrap Survey says

We highlighted results from SMU’s inaugural Ferrous Scrap Survey last month. Results from our second survey also provide some valuable insights.

The monthly scrap survey covers everything from pricing and demand to logistics and expectations for the months ahead. We’ve also created Scrap Buyers’ Sentiment Indices – both current and future – to maintain some parallels with SMU’s long-running steel survey.

It’s free to participate in our scrap survey. And remember, if you’re a Premium member, you will have access to the results. (Editor’s note: If you’d like to upgrade from Executive to Premium, please contact SMU Senior Account Executive Luis Corona at luis.corona@crugroup.com.)

Below is a sneak peek at the scrap survey results we will release on Monday afternoon.

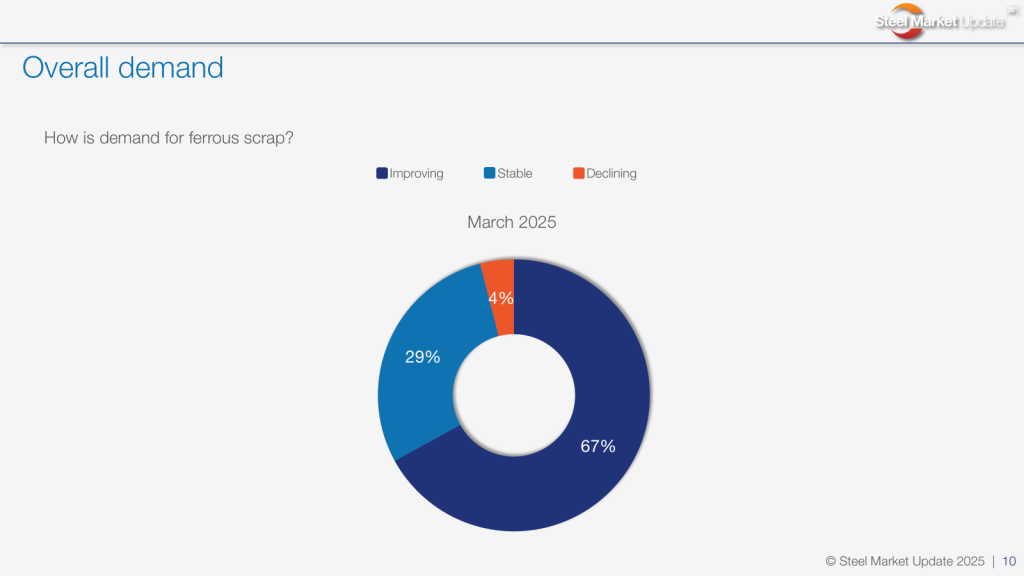

How is demand for ferrous scrap?

We saw a big jump compared to February’s survey. More than two-thirds of respondents see scrap demand improving – up from 41% last month. Just 4% report declining scrap demand vs. 14% in February.

Here’s what some of our respondents are saying:

“Greed Economics 101 as scrap follows steel price increases. Further, if there were no tariffs, they probably still would increase primarily because of seasonal winter conditions.”

“Very tight market, and not a lot available or being generated.”

“Tariffs will affect short-term demand.”

“Not enough prime scrap is being generated by the auto industry and its suppliers.”

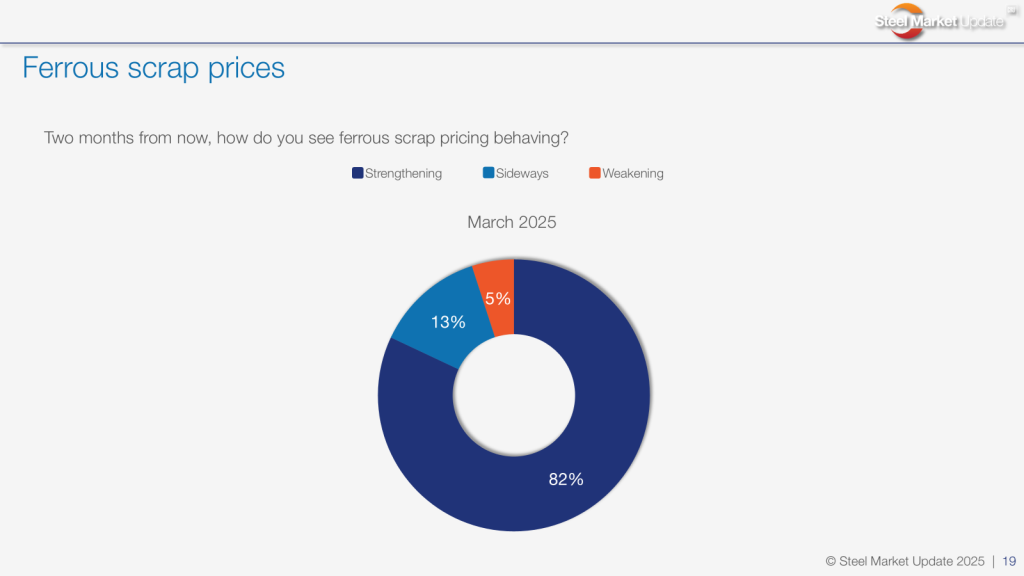

How do you see ferrous scrap pricing trending over the next 60 days?

Respondents were more bullish this month on the outlook for scrap prices than they were last month. More than 80% see prices strengthening over the next two months. Another 13% think prices will be sideways. And the remaining 5% expect the price environment to weaken come May.

Here is what some of our respondents are saying:

“Scrap prices were severely depressed in 2024, and it looks like the market has turned.”

“The spring melt is making scrap more available in the North, and scrap substitutes are becoming lower cost in comparison. That will help weaken demand for scrap products. Over the summer, we should see scrap prices come back down.”

“Demand is stable and inbound flows are lower.”

“Up in March, sideways in April.”

“If exports weaken substantially, the market will correct.”

“Sideways to up. Weather depending.”

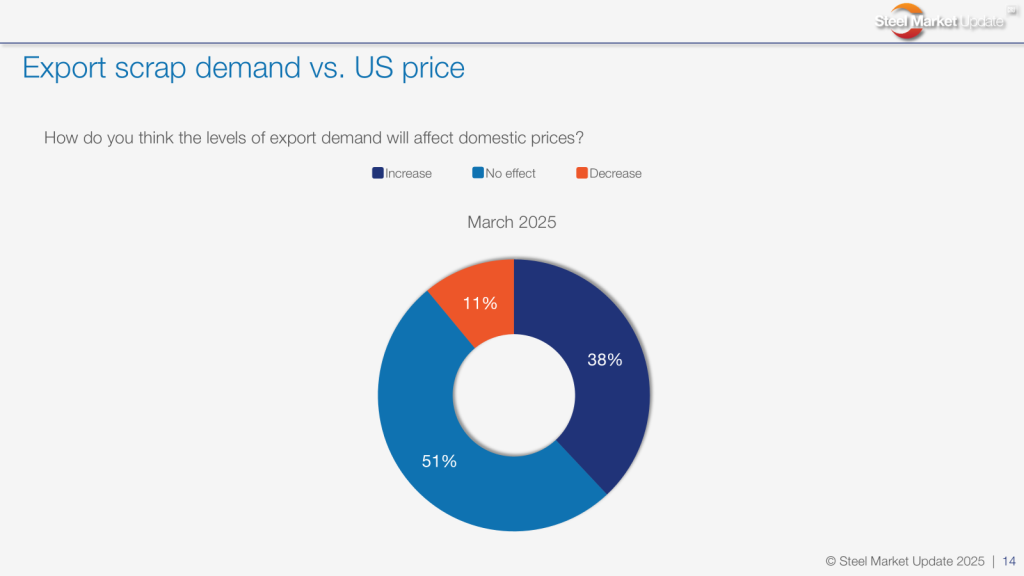

How do you think the levels of export demand will affect domestic prices?

We asked in the survey how the export market might influence on US prices. Thirty-eight percent of respondents think export demand will increase domestic tags. Fifty-one percent anticipate no impact. And 11% see prices decreasing.

Below is what some of our survey respondents are saying:

“Once tariffs are attached to steel, exports become a non-issue.”

“No effect on US market.”

“There is very little export business at present, and much of what would be exported is now going to be shipped back inland to domestic mills.”

“As a net exporter of scrap, we will need to continue to keep the flow heading out of the country. As our price increases, exports will decrease until the scrap can no longer be held – leading to lower offerings. Global demand is still trailing US demand.”

“The US is the strongest market in the world right now. It’s bullish sentiment caused by tariff policies.”

“If exports weaken substantially, the market will correct.”

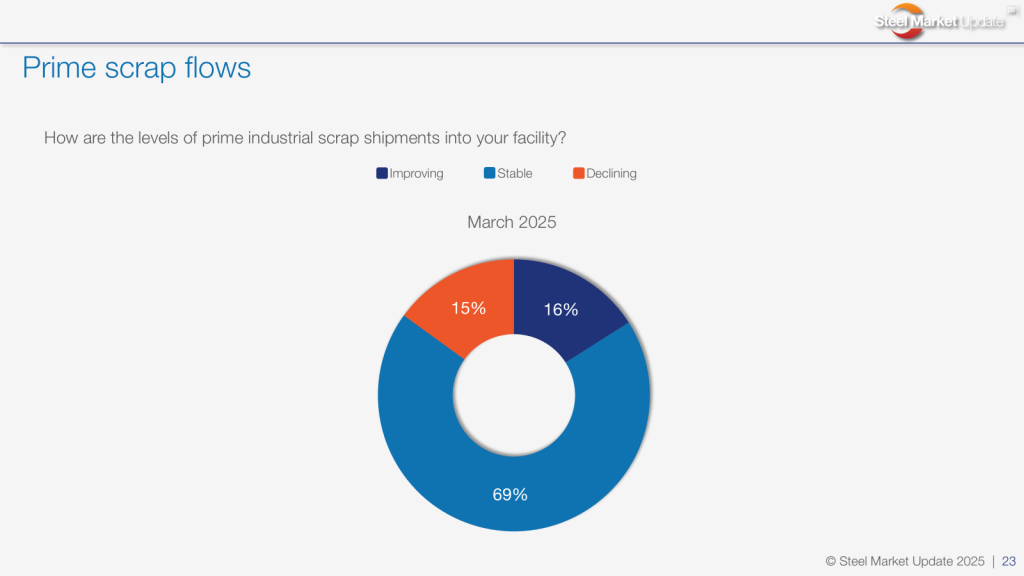

How are the levels of prime industrial scrap shipments into your facility?

Sixteen percent saw them improving in March, up from just 5% in February’s survey. Sixty-nine percent thought flows were stable. Only 15% said flows were declining.

Here is what some of our respondents are saying:

“I am hearing anything from up $20 to up 50 per gt.”

“Sounds like $30 to $40 up, with some expecting as much as $60.”

“Everything we’re seeing and hearing points to a decent-size bump in price for March.”

“Tight supply and increasing demand.”

Much more to come

Well, there you have it. Just a quick peek at some of our latest scrap survey data. We’ve had a great response rate in our first two scrap surveys. And we’re sure that will continue as SMU’s scrap survey becomes more established in the months ahead.

So, stay tuned for more SMU scrap coverage – especially of March’s upcoming settlement.

And, finally, we’d love for you to participate in our future ferrous scrap surveys! If you’d like to participate, reach out to me at david@steelmarketupdate.com to learn more.

Again, we will report full results of our March Ferrous Scrap Survey to our premium subscribers on Monday afternoon.

And, as always, all of us here at Steel Market Update truly appreciate your support.