Market Data

February 20, 2025

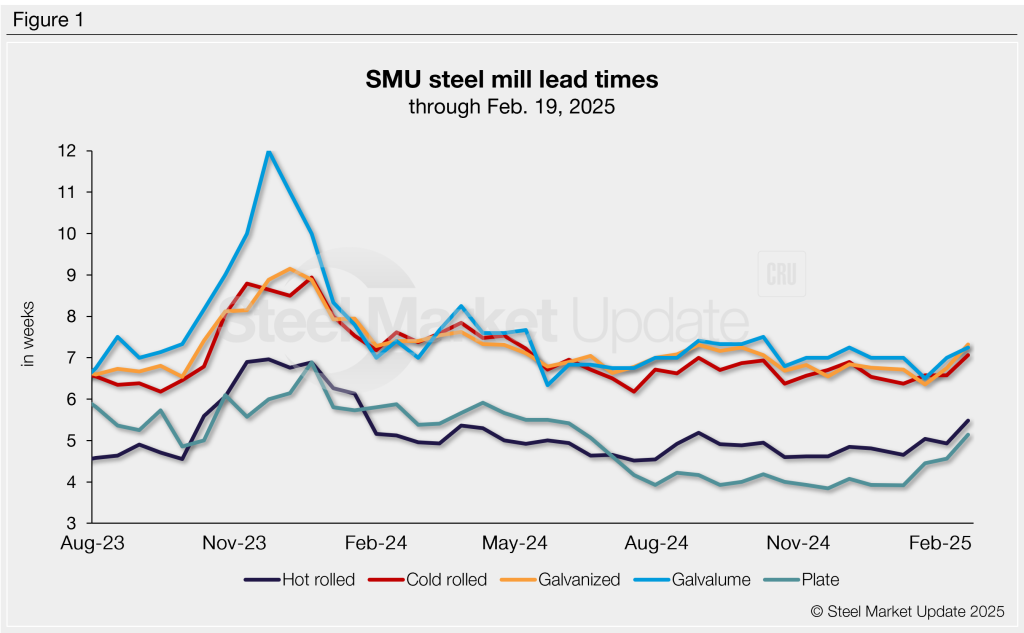

SMU Survey: Mill lead times stretch to 10-month highs

Written by David Schollaert

Buyers responding to our latest market survey reported that steel mill lead times were stretching out this week for sheet and plate products tracked by SMU. The results weren’t much of a surprise. Production times have begun moving out following a wave of frenzied buying in response to stricter Section 232 announced by the Trump administration last week.

Lead times for sheet and plate have, as a result, pulled away from the lows they’d been at since mid-2024.

Lead times for hot-rolled, cold-rolled, coated, and plate products are all at 10-month highs, with an average increase of ~10% over the past two weeks.

Table 1 below summarizes current lead times and recent trends.

Compared to our Feb. 5 market check, all lead time ranges have shifted this week:

Hot rolled: Our range widened from 3-7 weeks to 4-8 weeks.

Cold rolled, galvanized, and Galvalume: The shortest lead time in each range increased from 5 weeks to 6 weeks.

Plate: The shortest lead time in our range is still 3 weeks; however, the longest lead times jumped from 6 weeks to 8 weeks.

Crystal ball says…

Just over half of the respondents we surveyed this week (54%) foresee longer lead times two months from now, a fall from 62% two weeks ago. Most of the others (45%) expect production times to hold steady, up from 36% previously. A small remainder continues to believe lead times could contract further. (The full results of our survey are available here for our Premium members).

Here are some of the comments we collected this week:

“Lead times have been so short for so long, I understand lead times are increasing now for maybe a month or so, but in 2 months I think demand will have leveled off.”

“I feel they will flatten out, but they will be longer than they currently are.”

“It will follow demand and higher steel prices.”

“Follows the recovering market with a slight lag.”

“Construction season – unless the infrastructure bill is rattled, nonres still needs a shot in the arm, and interest rates might get sticky.”

“Very unpredictable due to the impact of steel tariffs.”

“Business is slowly waking up.”

“This is a key one. If we see “real” demand pick up, this rally could get scary.”

“Supply is down due to fewer imports and demand improving.”

“I think they extend in the near term and then settle down.”

“Mills controlling order intake right now and holding buyers to minimums on contracts.”

“Low inventory and increased demand are factors in moving plate lead times out.”

“Domestic mills certainly have capacity… I don’t see lead times extending too much.”

Trends

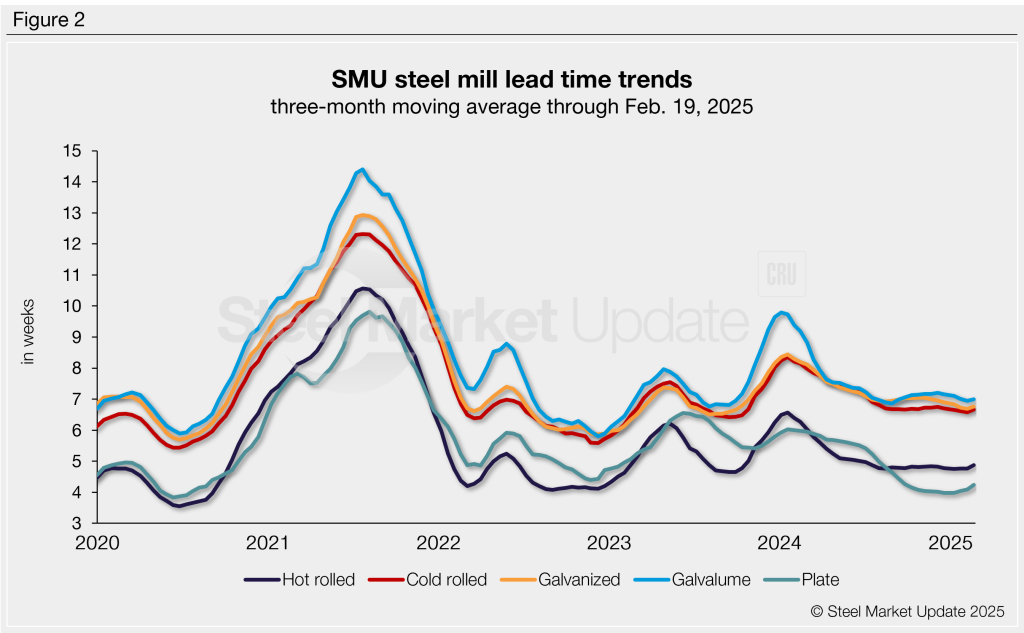

To smooth out the variability in our biweekly data and highlight trends, lead times can be calculated on a three-month moving average (3MMA) basis. This week, lead times for sheet and plate products moved higher on a 3MMA basis, rising ~2% on average. Overall, lead times had been trending lower since last March before flattening out over the past few months. They have since begun moving ahead of near one-year lows (Figure 2).

The hot rolled 3MMA is now at 4.88 weeks, cold rolled at 6.66 weeks, galvanized at 6.76 weeks, Galvalume at 7 weeks, and plate at 4.23 weeks.

Note: These lead times are based on the average from manufacturers and steel service centers participating in this week’s SMU market trends analysis survey. SMU measures lead times as the time it takes from when an order is placed with the mill to when it is processed and ready for shipping, not including delivery time to the buyer. Our lead times do not predict what any individual may get from any specific mill supplier. Look to your mill rep for actual lead times. To see an interactive history of our steel mill lead times data, visit our website. If you’d like to participate in our survey, contact us at info@steelmarketupdate.com.