Mexico

February 20, 2025

HR Futures: Meaningful rally grips market

Written by Daniel Doderer

Another eventful week in the physical and financial steel markets is coming to a close. Most importantly, this week provided complete clarity that, after months of waiting for a catalyst, we are now definitively in the early stages of a meaningful rally. The 3rd month future (currently the April contract) rose more than 8% for the second consecutive week, reaching $947 as of the Thursday, Feb. 20, settle.

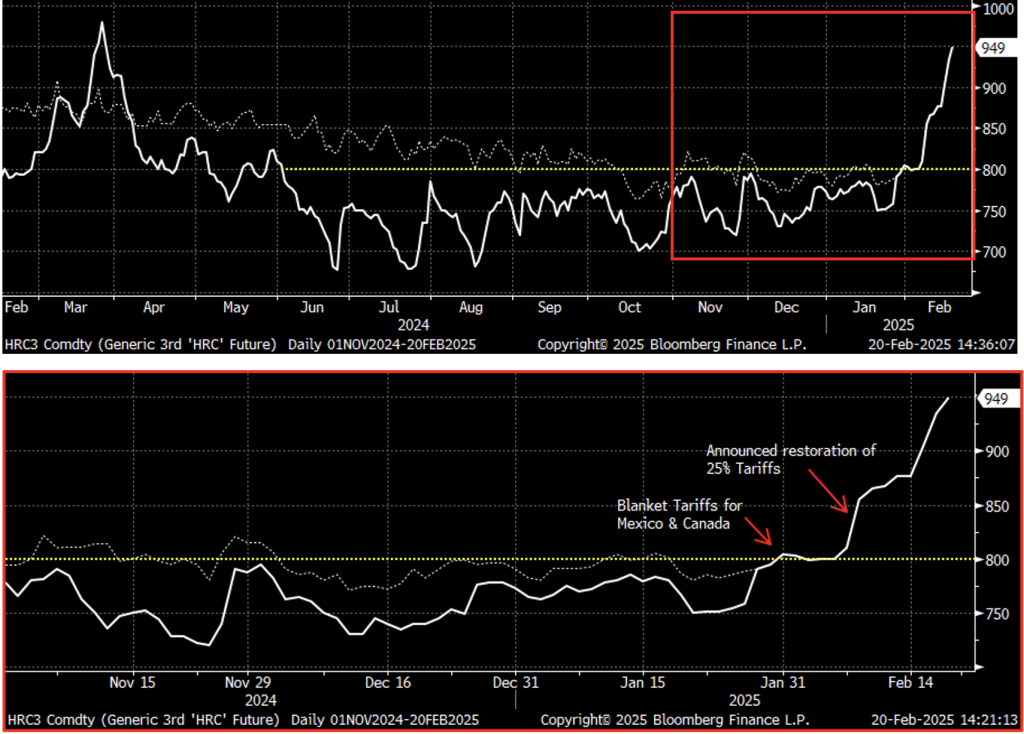

The first chart below offers additional context, highlighting how unusually long the market remained in contango. For months, near-term contracts (3rd Month, solid white) consistently struggled to push above $800 (yellow) since early June of last year, while later-dated futures (April ’25, dotted white) held higher prices for 44 weeks. For clarity, these two converged on Jan. 29, when April ’25 became the 3rd month contract. The second chart zooms in to illustrate the dynamics since Nov. 1.

Rolling 3rd month future (white, solid), April ’25 future (white, dotted), and front of curve resistance (yellow, dotted)

While every reader here is likely up to speed on recent events, we’ve annotated the chart above with the two most notable to show how the market has been reacting to trade policy.

First, after frequently attempting and failing to push above $800, the announced tariff action on all goods from Mexico & Canada at 25%, and an additional 10% on all goods from China stabilized pricing at that resistance level (although the former action was delayed by 30 days).

Almost immediately following this, domestic mills sent out a flurry of announcements in an attempt to firm up the floor, followed by the Nucor consumer spot price (CSP) steadily grinding higher from $750 at the end of January (now $820, as of Feb. 17).

Even so, there was very little movement in the futures, until Monday, Feb. 10, when it was announced that the Trump administration would re-establish the 25% tariff on all steel imports, in effect on March 12, removing the previous established quotas.

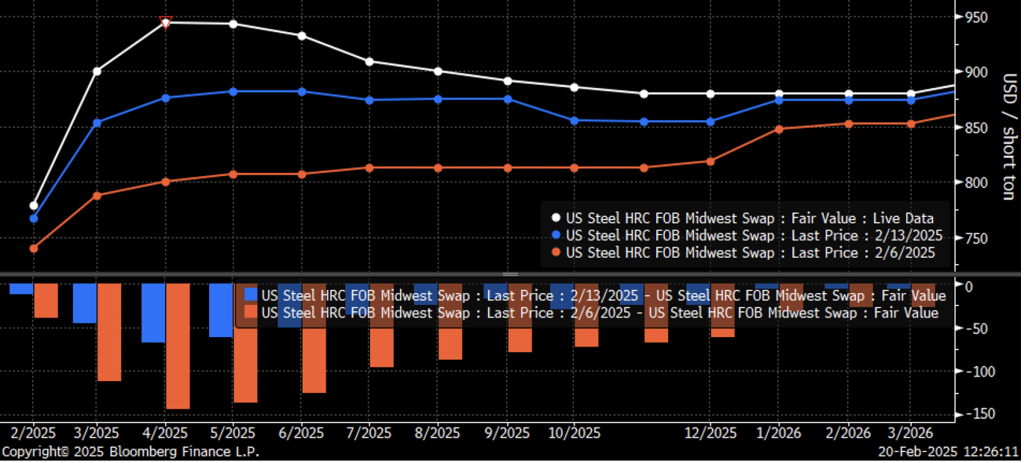

Interestingly, near the end of last week, the chart below shows that the market was still in contango (blue). Since then, the 44-week contango cycle has officially ended, shifting into backwardation (white).

While the shape of the curve does not predict when the physical market will peak, in this case, it highlights the premium for steel in the coming months as supply chains adjust and global prices respond to new market realities.

At this stage, we believe this move has established a floor at $830, given current global pricing dynamics, though some deterioration remains possible if global prices follow a pattern similar to 2018.

However, as we’ve seen in recent weeks, much can change. Attempting to predict with confidence where and when this rally will peak—or when the floor will be tested—would be futile. This is especially true as overall steel demand is expected to improve throughout most of 2025 after 18 months of inertia.

CME Midwest HRC futures curve (2/20 in white, 1wk in blue, 2wks in orange)

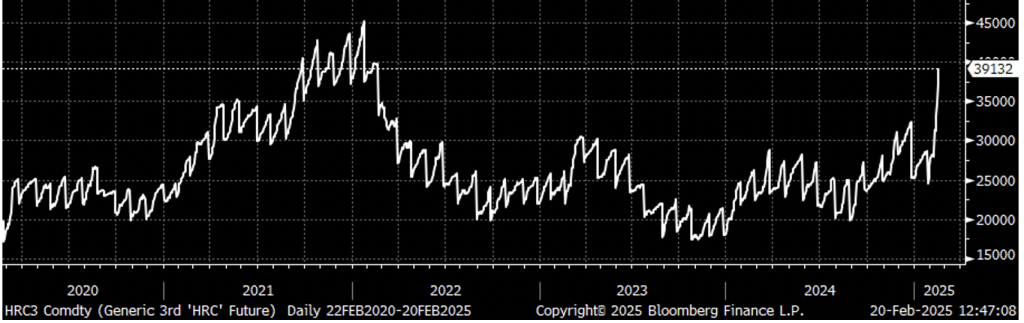

Finally, a notable and encouraging sign for the market’s health is the recent surge in liquidity, which has pushed open interest (below) to levels rivaling previous highs from late 2021 and early 2022.

Currently, participant statistics are only available through Feb. 11, and as of that date, they did not indicate a significant influx of new commercial participants on either the long or short side. However, we anticipate that updated data will show increases in both.

Aggregate open interest CME Midwest HRC futures

Disclaimer: The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Flack Global Metals or Flack Capital Markets should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.