Analysis

February 20, 2025

Final Thoughts

Written by Michael Cowden

Some of you have told me that the current market feels about as crazy as early 2021 when demand snapped back after the initial outbreak of the Covid-19 pandemic.

Others have said it might be more like late February/early March 2022, when Russia launched a full-scale invasion of Ukraine – and, in the process, caused a panic over pig iron availability.

For the time being, I’ll set aside questions about whether what we’re seeing now is the beginning of a period of sustainably higher prices (Covid snapback) or another of the price spikes (Russia invasion) the US market is notorious for.

It feels a lot like 2021-22

Instead, as a therapist might say, I just want to acknowledge the validity your feelings. There are data points that indicate some clear parallels between now and the ’21 and ’22 market frenzies.

Look at mill negotiation rates from our latest survey results. (We’ll release full results to our premium members Friday afternoon.) Only 21% of survey respondents said that mills were willing to negotiate lower hot-rolled (HR) coil lower prices. That’s down from nearly 90% in early January.

By the way, is it just me, or does early January feel like another galaxy now? The simple times before President Trump’s inauguration and before POTUS announced that Section 232 was coming while flying to the Super Bowl on Air Force One.

In any event, the last time we saw negotiation rates this low was in March 2022, in the immediate aftermath of Russia’s full-scale invasion of Ukraine. The ensuing all-out war called into question what, at the time, accounted for two-thirds of the US pig iron supply (roughly one-third each from Brazil, Ukraine, and Russia.)

The pig-iron panic caused HR prices to spike from $825/st in mid-February 2022, just before the war, to $1,160/st by mid-April, according to SMU’s interactive price tool. (After that, prices fell back to earth.) Are we about to see something similar?

The whispered price hike

Another notable aspect of this post-Trump tariff round of price hikes is that many have not been written down. Is it because the market is moving too fast? Because no one wants to be blamed for inflation? Because no one needs a reminder of which way prices are going?

I’ll leave the answer to that to you. But seeing US steelmakers pushing prices higher from one day to the next? That feels a lot like early 2021.

Case in point: Nucor said it was seeking at least $820/st for HR on Monday. U.S. Steel quietly announced that it wanted at least $850/st. And NLMK USA wants at least $900/st. SMU has heard that certain mills have not yet opened April but could be at around that level when they do.

HR prices have not been at or above $900/st since mid-February 2024, a little over a year ago. Cold rolled and coated prices have not been at or above $1,100/st since April 2024, according to SMU’s interactive pricing tool. Meanwhile, lead times are stretching out to 10-month highs.

And that’s just on the sheet side. When it comes to plate, we’ve seen SSAB Americas announcing increases totaling at least $240/st in less than a month.

Here’s another bit of data that stands out.

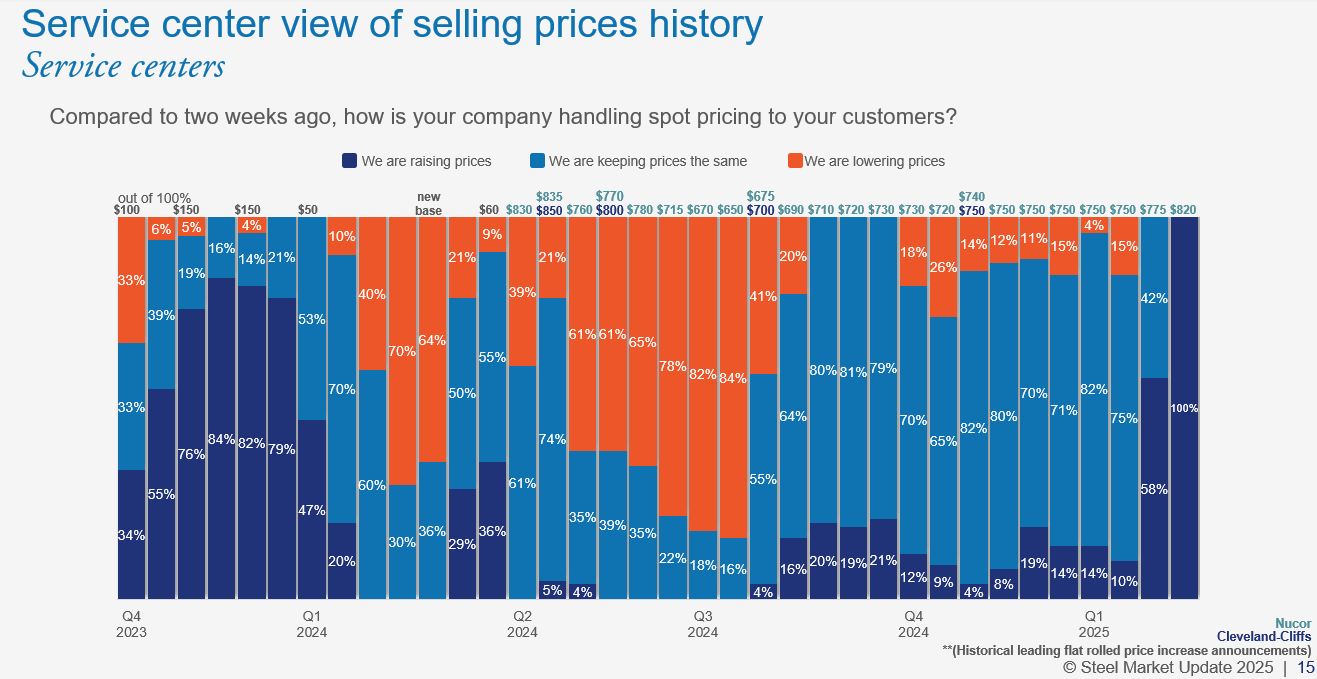

As of right now – and I stress that this is preliminary data – 100% of service centers responding to our survey told us that they were raising prices to their customers. Compare that to 58% two weeks ago and 10% the week of Trump’s inauguration.

Maybe that 100% figure will come down a little by the time we release the final results on Friday afternoon. Even if it dropped to, say, 90%, the last time we saw a figure that high was following Russia’s invasion of Ukraine and, before that, in the first half of 2021.

But is it really a repeat?

That said, there are a couple of data points that definitely don’t reflect the realities we saw in 2021 and early 2020. Here is one:

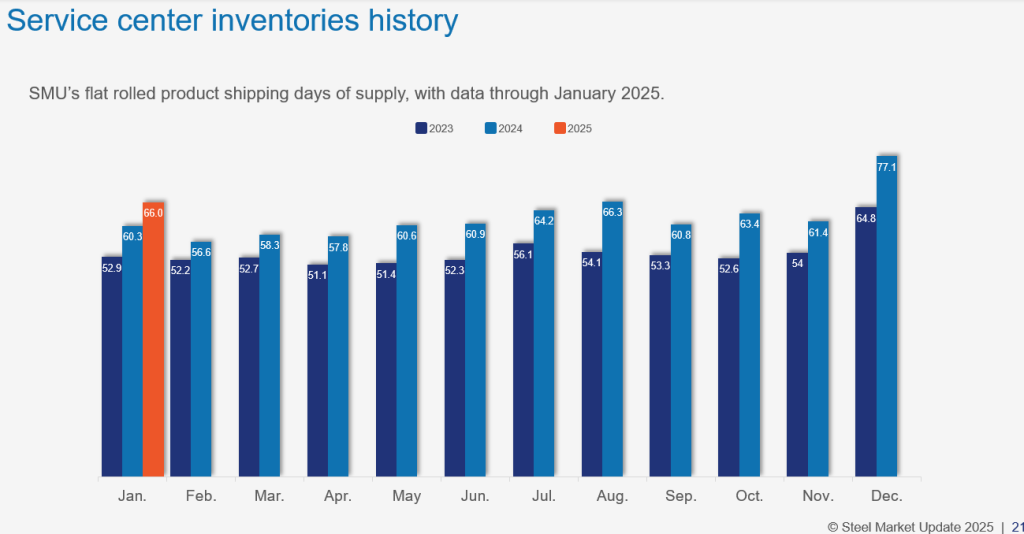

Yes, sheet inventories declined in January from elevated levels in December. That said, and as you can see in the chart below, we’re still well above where we’ve been in recent years.

And if you check out our full data series (available to premium subscribers), you’ll see that that 66 days’ supply is the highest January we’ve recorded since we launched our own service center inventory data in January 2019. Where were things in January 2021 as prices prepared for a liftoff the likes of which we haven’t seen since? Only 40 days of supply.

I guess my point is this: The upside risk to prices was clearly higher than the downside risk in the back half of 2024. Some mills were losing money. They could not afford to go any lower. Is the reverse true now – is the downside risk more than the upside risk?

In other words, should steel buyers continue to panic? Or should they step back, take a deep breath, and consider what the market might look like once we get to late spring/early summer? Are we going to see prices rise throughout the first half of the year, as we did in 2021? Or will we see prices moderate once the initial shock of tariffs passes?

Consider an upgrade

I’ve mentioned some data that’s available only to “premium” SMU subscribers. If you’re an “executive” subscriber who’d like to have access to that, please reach out to SMU Senior Account Manager Luis Corona (luis.corona@crugroup.com) to learn more about upgrading to a premium subscription.

Thank you for your continued interest in Steel Market Update.