AMU

February 13, 2025

Wittbecker on Aluminum: Canada’s options to combat US tariffs

Written by Greg Wittbecker

Canada remains at risk from several import duties on its exports of aluminum to the US.

On March 4, it may face a 10% duty under the heading of criterial mineral imports after being threatened with a 25% tariff against it and Mexico. There is a view that aluminum will get the same treatment as the announced 10% tariff on Canadian crude.

On March 12, a 25% duty goes into effect under the revised Section 232 executive order. Canada will lose its exemption under Section 232.

The problem is that the situation in Washington is so fluid that no one really knows what to expect.

Thus far, the physical and financial markets are discounting the probability of these tariffs being enacted. The Chicago Mercantile Exchange (CME) Midwest Futures contract is valuing premiums between $0.37-$0.3850 per pounds into June.

There is still a dogged belief that there’s a deal to be done with Trump, and this won’t happen. They might be right, but we would be surprised if the commercial people at Alcoa, Rio Tinto and Alouette in Canada are not running the numbers on different alternatives.

Gordon Sullivan wrote a classic business book in 1996 called “Hope Is Not A Method,” and we doubt the three Canadian producers are simply hoping for a better outcome. They will be planning alternative export markets if the Midwest premium does not fully weigh the effect of the duties.

Europe is the natural outlet

Canada will look to the Rotterdam duty paid ingot market for its alternative to the US. There are compelling reasons why this makes sense.

One reason is Canada has a free trade agreement with the EU27, the Comprehensive Economic and Trade Agreement (CETA). This gives Canada duty free entry to the EU. That means Canadian metal is sold at the Rotterdam duty paid premium market, which trades at about $50/metric ton premium to duty unpaid metal.

Another is that Canadian metal is low carbon (2 tons of CO2/ton production), which commands a slight premium in the EU of $10-$20/metric ton.

Additionally, Canada’s transit time to Europe is better than its competitors in India, the Middle East and Asia. What buyers don’t like a shorter supply chain that can be more reactive to their changes in demand?

The market has expressed skepticism about how fast and in what volumes Canada could divert to Europe. We have no doubt that all the companies have sold forward already for 2025 into the US. The incumbent suppliers to Europe are also likely to have decent backlogs of sales for 2025. So, it may be hard for the Canadians to free up units for Europe and to displace the incumbents. However, we wanted to look at the most recently available trade statistics for the EU27 to see the potential for Canada.

EU27 trade flows and opportunities for Canada

The latest full year of data available is 2023 for imports under HTS (Harmonized Trade Schedule) 7601, which is primary aluminum. The EU27 imported a total of 6.3 million metric tons in 2023.

This is a summary of the major origins:

| Metric Tons 2023 | Comments | |

| Norway | 1,374,522 | Duty Free into EU |

| Iceland | 758,452 | Duty Free into EU |

| United Arab Emirates | 667,950 | |

| India | 589,906 | |

| Russia | 512,153 | |

| Mozambique | 453,306 | Duty Free into EU |

| Bahrain | 346,831 | |

| South Africa | 173,301 | |

| Malaysia | 151,859 | |

| Canada | 132,914 | Duty Free into EU |

| Egypt | 117,162 | Duty Free into EU |

| Kazakhstan | 108,294 | |

| Saudi Arabia | 72,884 | |

| Türkiye | 62,520 | |

| Oman | 60,658 | |

| Australia | 52,271 | |

| Qatar | 41,779 | |

| Ghana | 34,916 | Duty Free into EU |

| Cameroon | 31,943 | Duty Free into EU |

| New Zealand | 25,889 | |

| Brazil | 25,701 | |

| Venezuela | 22,013 | |

| Indonesia | 14,105 | |

| Argentina | 13,411 |

Amongst these major origins, 2.3 million metrics comes duty free countries excluding Canada. This metal supply is inelastic due to its value as duty paid metal. The rest of the origins are duty unpaid, representing 2.9 million tons. This pool of metal represents the competing supply against Canada.

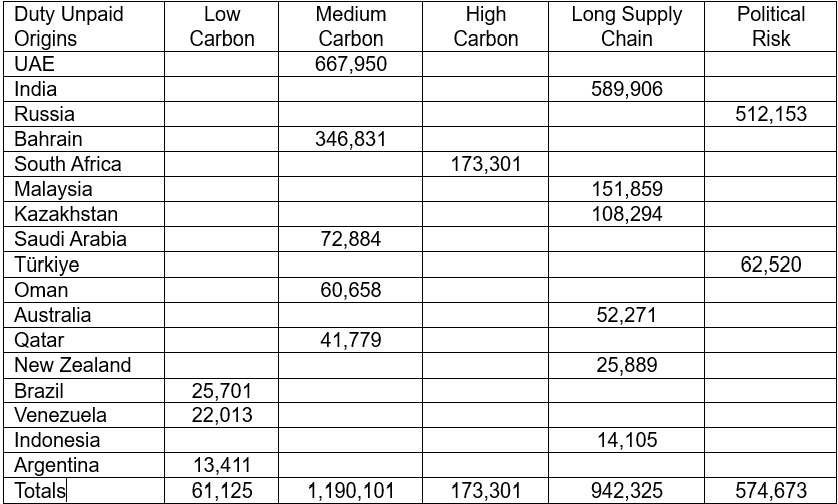

Let’s dig a little deeper:

(in metric tons)

What does this tell us?

One thing it tells us is Canada does not face substantial low carbon competition from duty unpaid origins. It will face major competition from duty paid production in Iceland and Norway.

Also, the Middle East is a concentrated block of medium carbon (8 tons CO2/ton) production. Their transit time to the EU is hindered by the problems in the Horn of Africa with the Houthi rebels. This has forced Middle East shipments around the Cape of Good Horn adding seven to 14 days.

South African metal is high carbon (16 tons CO2/ton) making it less attractive to European as carbon border taxes loom in 2026.

Additionally, metal originating in India, Oceania and South Asia represents an exceptionally long supply chain.

Also, Russian metal is on the cusp of being banned for import into the EU. The market has been voting with their wallets in 2024, also reducing estimated Russian imports to only 130,000 metric tons. There are questions about the true origins of the metal coming from Türkiye (Turkey in its old Anglicized form). Many believe this is Russian metal being transshipped so it is problematic long-term.

Canada’s best chances to displace suppliers in this pool come from the following:

The long supply chain origins. (942 kmt tons) They will be aided by the fact that India, Kazakhstan, and Australia are also coal-based production meaning they are high carbon.

South African high carbon. (173kmt) The impending carbon border tax make this origin highly vulnerable and suspect to attack from Canada.

Russian metal. (574kmt) will be hard pressed to win back customers in the EU even if the Ukraine war is settled. Memories of Russian gas interruptions are fresh in the minds of the EU and trust will be slow to rebuild.

Medium carbon supply ex the Middle will be the toughest competition. (1,190kmt) The producers are first rate with an excellent product and excellent performance. Notwithstanding the carbon tax that’s coming, the Middle East will remain strong competition, but Canada should peel some business away.

We expect the volumes in long supply chain, South Africa, and Russia to be won by Canada. That’s 1.6 million tons.

Canada goes direct to Mexico

In 2025, Mexican primary aluminum consumption will top 900,000 tons. Canada has been supplying that market already, sharing the market with imports from the Middle East, Russia, and China. One of the likely outcomes of the US-Mexico trade confrontation is that USMCA is going to be restructured. Rules of origin will be tighter and US/Canadian origin metal will be the winners. Of course, Canada and Mexico first need to make peace with the Trump Administration on tariffs… but eventually, you have to expect ties amongst the three nations will be stronger.

In the short-run, Canada will look at going direct to Mexico to bypass US markets. This would take the form of seaborne shipments from the St. Lawrence into Mexico’s eastern port of Veracruz.

An obvious question in the short run is how secure is that 900,000 demand, given pending US import tariffs on Mexico. The US and Mexico traded $840 billion in 2024. The auto sector is huge, so are white goods and building products for aluminum. Demand could suffer. However, the two economies are so intertwined that one has to believe that the Trump administration will make some deal to keep trade going.

Canada may be counting on this and developing capabilities to go direct now and bypass the US until the tariff battles are settled.

One thing is clear, Canadian producers are not sitting on their hands hoping this tariff problem goes away. They will act to create alternative markets to minimize the damage from whatever tariffs are eventually settled upon.

Editor’s note

This is an opinion column. The views in this article do not necessarily reflect those of SMU. We welcome you to share your thoughts as well at info@steelmarketupdate.com.