Analysis

February 9, 2025

Final Thoughts

Written by Ethan Bernard

There’s no doubt that the ferrous scrap market is dynamic and of great importance to our subscribers. That’s why at SMU we have made the decision to add a scrap survey to complement our current steel survey. And we’ll also be expanding our scrap coverage to help keep you up to date on all the twists and turns in the market.

With over two-thirds of US steel production coming from EAFs, intel about scrap has never been more crucial. Add in things like a potential tariff on Canada, whose scrap flows influence the US market, and one on Mexico for good measure, and things really get interesting.

So our survey covers things like pricing for the various grades SMU covers, demand, logistics, outlooks, and so much more. We’ve created Scrap Buyers’ Sentiment Indices, both current and future, to keep continuity with what you’ve come to expect from SMU.

I could go on talking about it, but even better, I’d like to show you some of the results from our first-ever SMU Scrap Survey. It will be published once a month. The goal: To give you some key intel just ahead of the monthly scrap settle.

It’s free to participate, and, remember, if you’re a Premium member, you will have access to the results. Judging from our first survey, there will definitely be plenty of good bits to digest. (And if you’d like to upgrade from Executive to Premium, please contact SMU Senior Account Executive Luis Corona at luis.corona@crugroup.com.)

So without further ado, we’ll let the survey results speak for themselves.

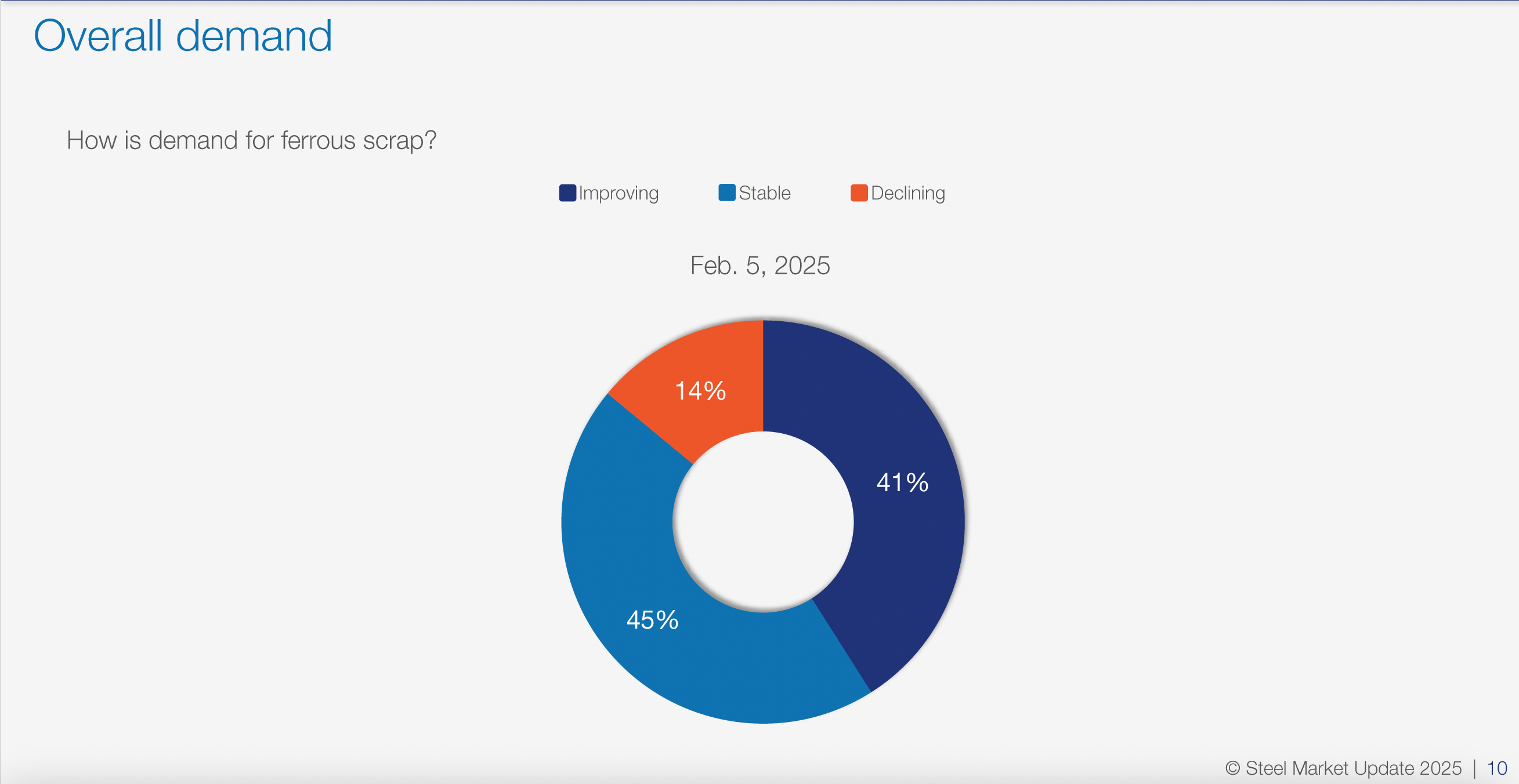

How is demand for ferrous scrap?

Regarding current demand, 41% responded that demand is improving, 45% thought it was stable, and 14% said it was declining.

What our respondents are saying:

“Seeing limited increased demand from Southeast Asia and US domestic.”

“Pricing is flat.”

“Not much scrap is moving in western Canada. Everyone needs more tons.”

“Mills are restocking from low year-end inventory levels.”

“Demand seems to be stable, but supply is certainly down.”

“I think a restocking period that was hoped for in January stalled because of weather.”

“Seems like everyone is cautiously optimistic.”

“Global markets have struggled with China buying less, but domestic demand is improving on a volume basis.”

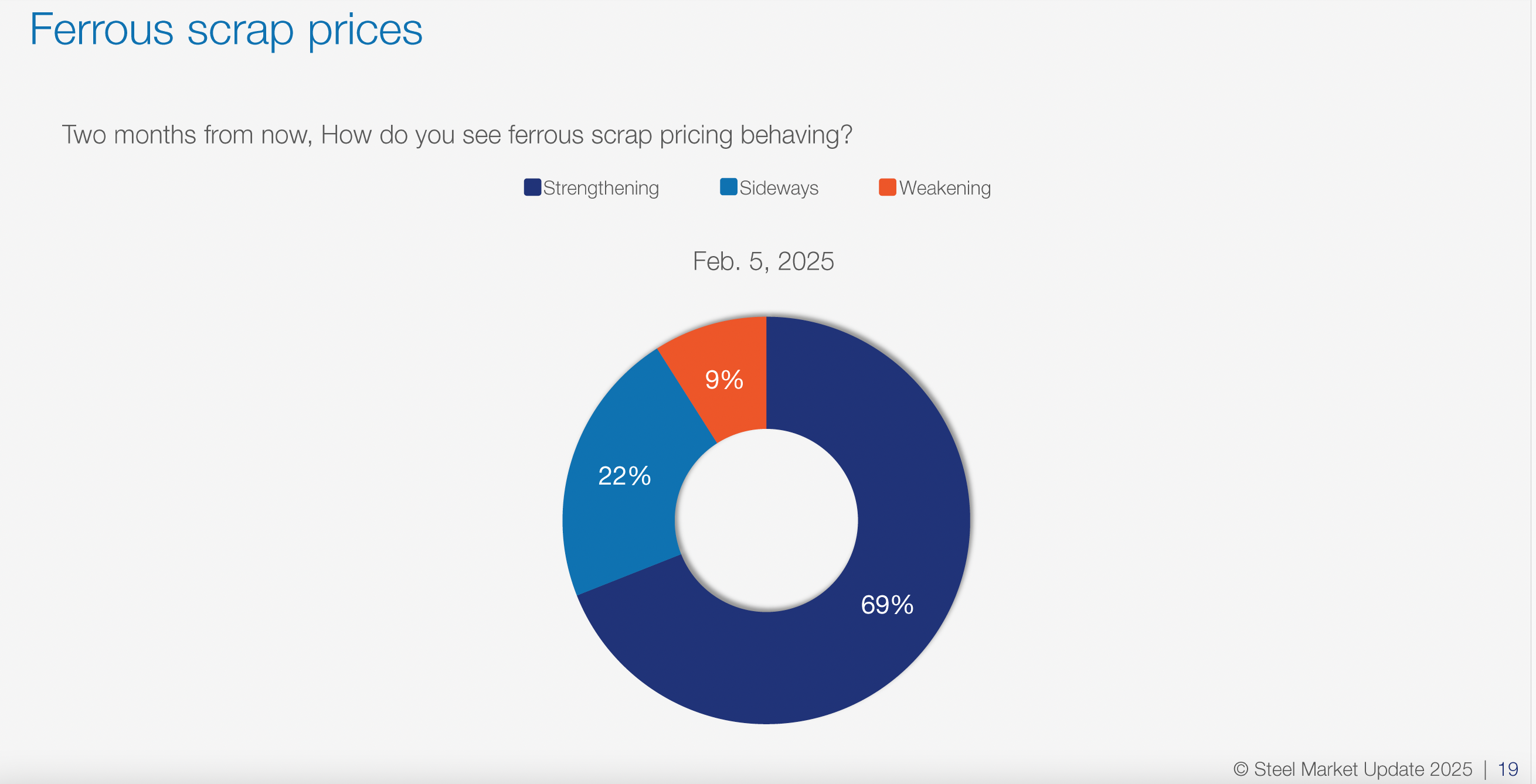

How do you see ferrous scrap pricing behaving over the next 60 days?

Respondents were bullish on scrap’s pricing outlook for the next 60 days, with 69% seeing prices strengthening. However, 22% thought pricing would be sideways, and the remaining 9% anticipated the price environment would be weakening.

What our respondents are saying:

“The current situation on tariffs is unclear. However, mill operating rates will likely strengthen heading into Q2. This will be positive for scrap and steel prices.”

“Unless we have more bad weather, order books not improving yet.”

“Trump is back in office.”

“Oil and gas companies are ramping up for sustained growth.”

“Supply-driven price increases in Jan. and Feb. I think the market in March is sideways to down based on a weak steel industry.”

“What happens in Washington will set the mood for the balance of this year.”

“Demand will increase throughout Q1. Supply will not keep up.”

“I think by the end of the first quarter, the market will be sideways to down. Mills ran inventory down for year-end and need to replace tons. Shredder feed will start flowing in, more material will be available.”

“Lower inbound flows and steady demand should bode well for scrap pricing.”

“Low melt-shop utilization rate.”

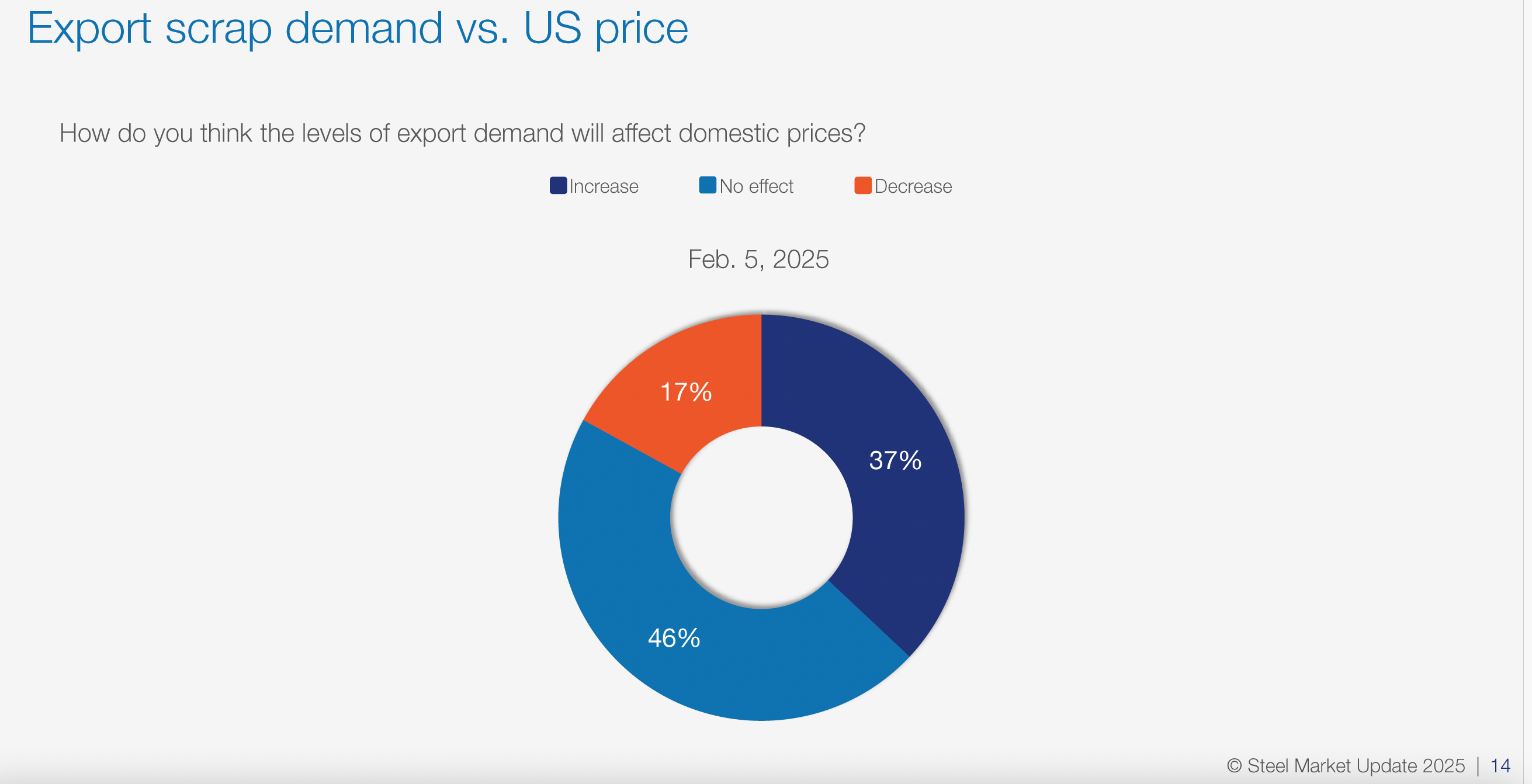

How do you think the levels of export demand will affect domestic prices?

On the question of export demand influencing US prices, 37% thought it would end up increasing domestic tags; 46% anticipated no effect; and 17% saw the opposite, with prices decreasing.

What our respondents are saying:

“Threat of tariffs.”

“Taking cut grades out of the supply chain.”

“Lower exports usually drops pricing.”

“Exasperate supply tightness.”

“Zero.”

“Won’t be much.”

“Mild increases recently.”

“Automakers are struggling with high inventories and lower demand, so this could help limit the upside.”

“Export has been a non-event for months in a row. Could be negative impact on price as winter months come to an end, unless domestic demand or export pricing picks up.”

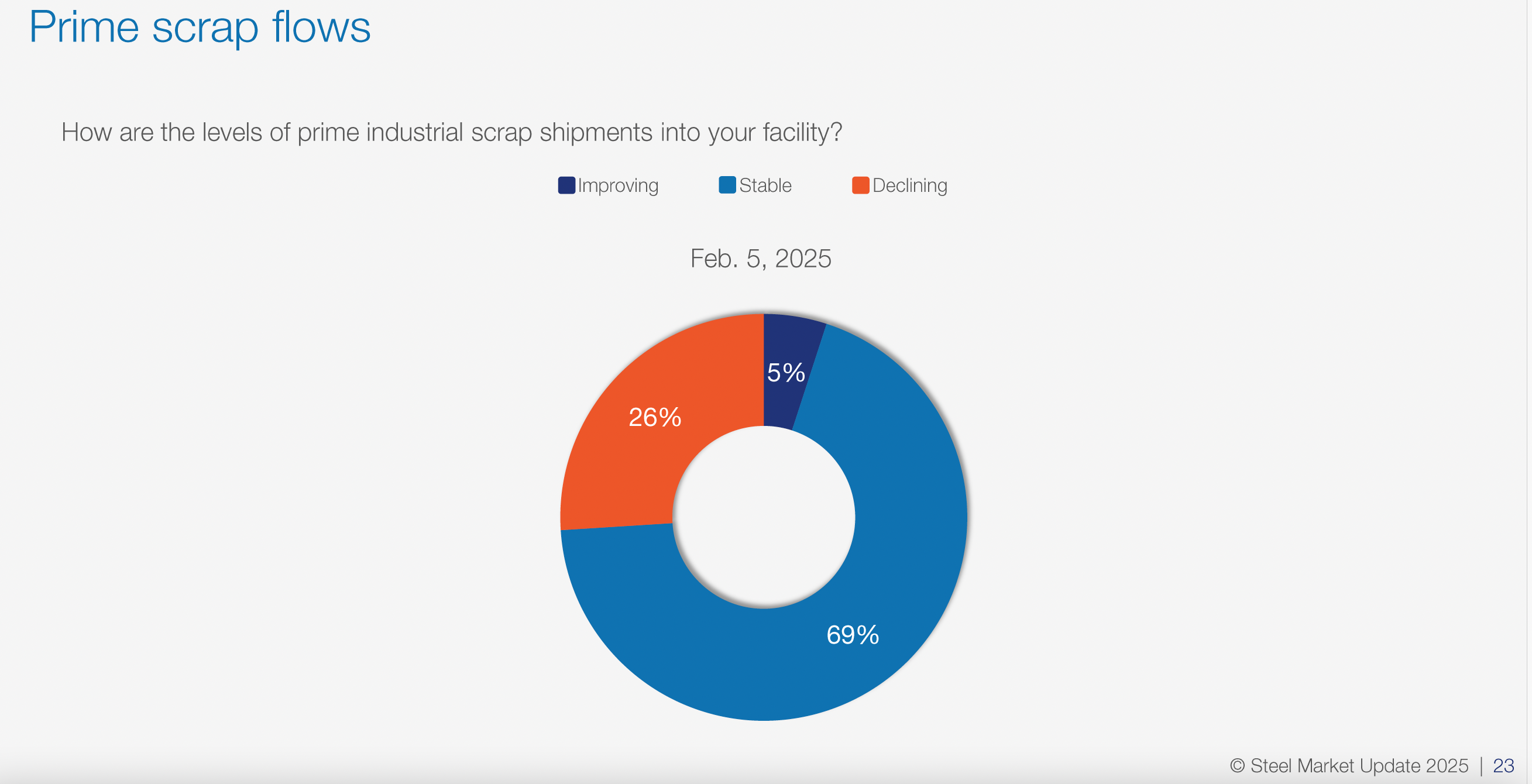

How are the levels of prime industrial scrap shipments into your facility?

For prime levels, 5% saw them improving, 69% thought they were stable, and 26% said they were declining.

What our respondents are saying:

“OEM available tonnage should increase this month and next.”

“Normal during winter months.”

“Don’t see much prime.”

“Slow manufacturing levels reducing generation of prime scrap.”

“Stable but down overall.”

“Manufacturing weak.”

Just the beginning…

Well, there you have it. Just a quick peek at some of our scrap survey data. We had a lot of respondents in this first one, and we’re sure things will ramp up even more as we get rolling in the months ahead.

So, stay tuned for more SMU scrap coverage, especially with the February settle happening as this article is published. Additionally, we’ll be keeping tabs on all things Trump for any tariff updates.

And, finally, we can’t wait for you to participate in our second survey for next month! If you’d like to participate, reach out to us at info@steelmarketupdate.com. It can be filled out in just a few minutes, we promise!