Analysis

February 7, 2025

US rig counts inch up, Canadian activity falls

Written by Brett Linton

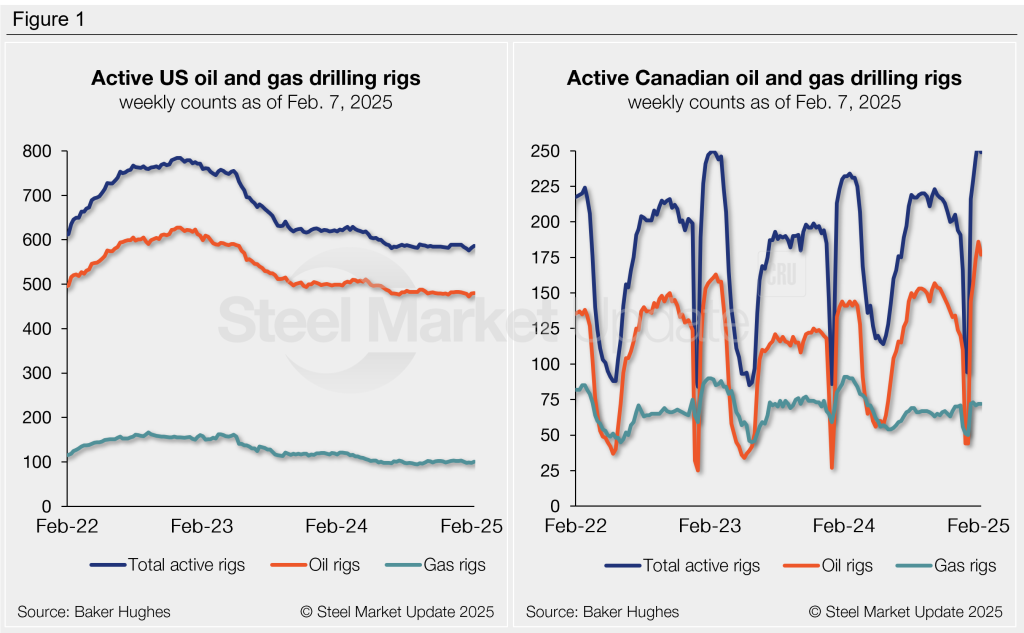

The latest tally of operational oil and gas rigs in the US increased slightly from last week, while Canadian activity declined, according to Baker Hughes.

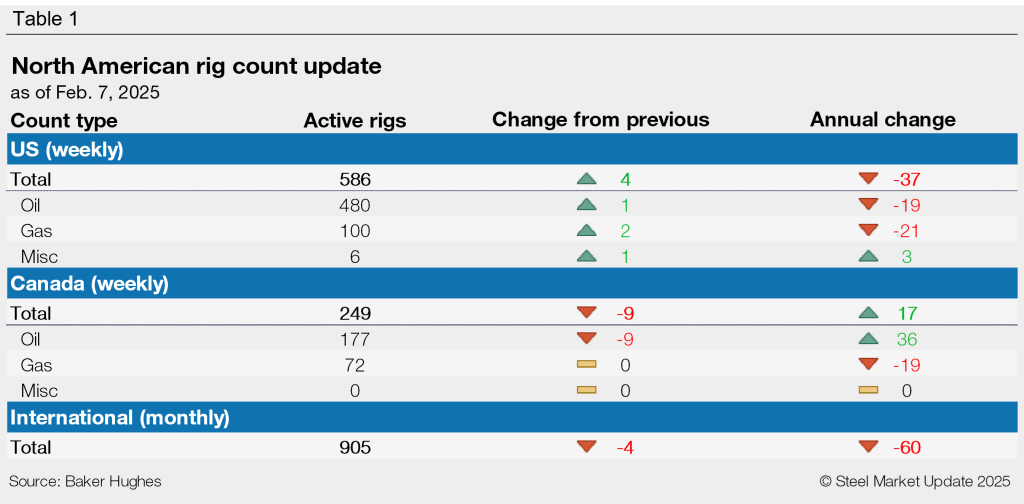

US counts remain marginally above multi-year lows. The drop in Canadian activity comes just one week after reaching a near seven-year high.

The US rig count is 586, up by four from the prior week. It’s worth noting that in late January, US activity fell to the lowest rate recorded since late 2021. US drilling activity has remained at reduced levels since June 2024.

Breaking a four-week streak of consecutive gains, Canadian activity slipped by nine rigs this week to a total of 249. Recall that the previous week’s count of 258 was the highest rate seen since March 2018. Historically, Canadian counts tend to surge through February before declining as warmer weather and thawing ground conditions limit access to roads and drill sites.

The international rig count is a monthly measure that was updated this week, now totaling 905 in January. This is down by four from the December count and 60 fewer than the same month last year.

The Baker Hughes rig count is significant for the steel industry because it is a leading indicator of oil country tubular goods (OCTG) demand, a key end market for steel sheet.

For a history of the US and Canadian rig counts, visit the rig count page on our website.