Market Data

January 22, 2025

Architecture firm billings fell in December on market uncertainty

Written by Brett Linton

Architecture firms reported a sharp reduction in billings in December, according to the latest Architecture Billings Index (ABI) released by the American Institute of Architects (AIA) and Deltek.

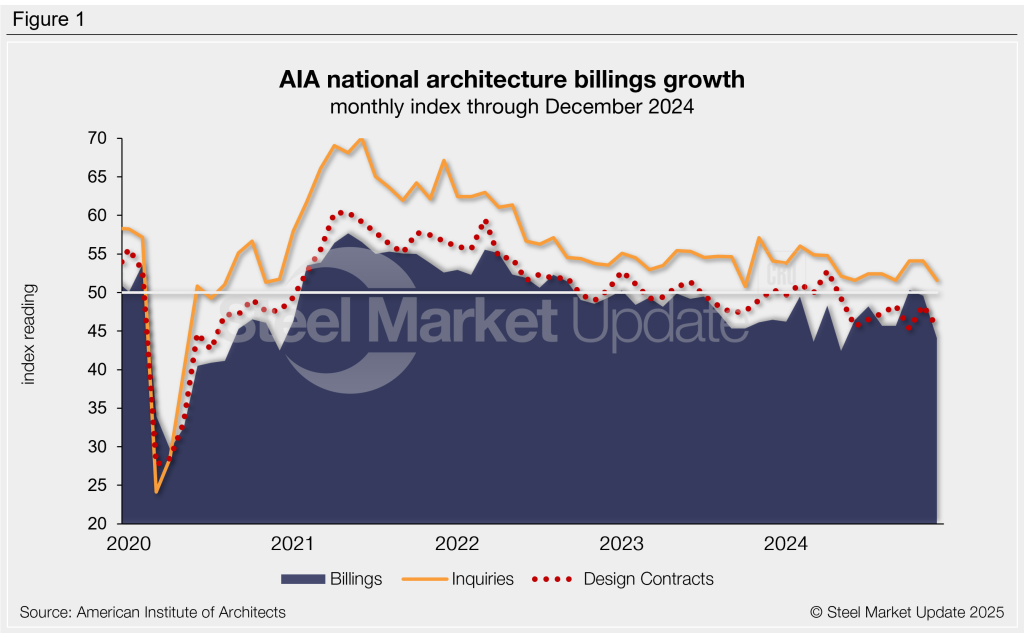

The December ABI fell 5.5 points month over month (m/m) to 44.1, shifting from one of the highest readings in two years to one of the lowest (Figure 1). The Index has declined each of the past two months, and has indicated declining business conditions for all but two months since October 2022.

The AIA/Deltek release attributed this deterioration to a continued period of future uncertainty that has been challenging for many firms, noting that clients remain hesitant to commit to new projects.

“While there were signs that the design cycle was bottoming out in the fourth quarter, the December reading indicated a step back,” said AIA chief economist Kermit Baker. He also commented that, “There remains considerable uncertainty as to the feasibility of many planned construction projects, so the wait-and-see period is extending into 2025.”

The ABI is a leading indicator for near-term nonresidential construction activity and projects business conditions approximately 9-12 months down the road (the typical lead time between architecture billings and construction spending). An index score above 50 indicates an increase in architecture billings, while a reading below 50 indicates a decrease.

Participant comments this month included:

- “We have not received any inquiries for new work in months.” – Southern institutional firm

- “Still flat, but expectations seem to be for some improvement in 2025.” – Western multi-family residential firm

- “Philadelphia, and the East Coast in general, do not get the same wild economic swings, since they are anchored by many large institutions.” – Northeastern institutional firm

- “We work nationally, and had very healthy inquiries in December, which is usually a slow month. Hoping that converts into new projects in the first quarter.” – Midwestern commercial/industrial firm

Sub-index trends

The new project inquiries index fell to a three-month low in December but remained in optimistic territory. It was one of the lowest measures seen in over a year, tied with September and June 2024 at 51.6.

Following November’s uptick, the design contracts index slipped in December to 45.5, marking the eighth consecutive month of declining conditions.

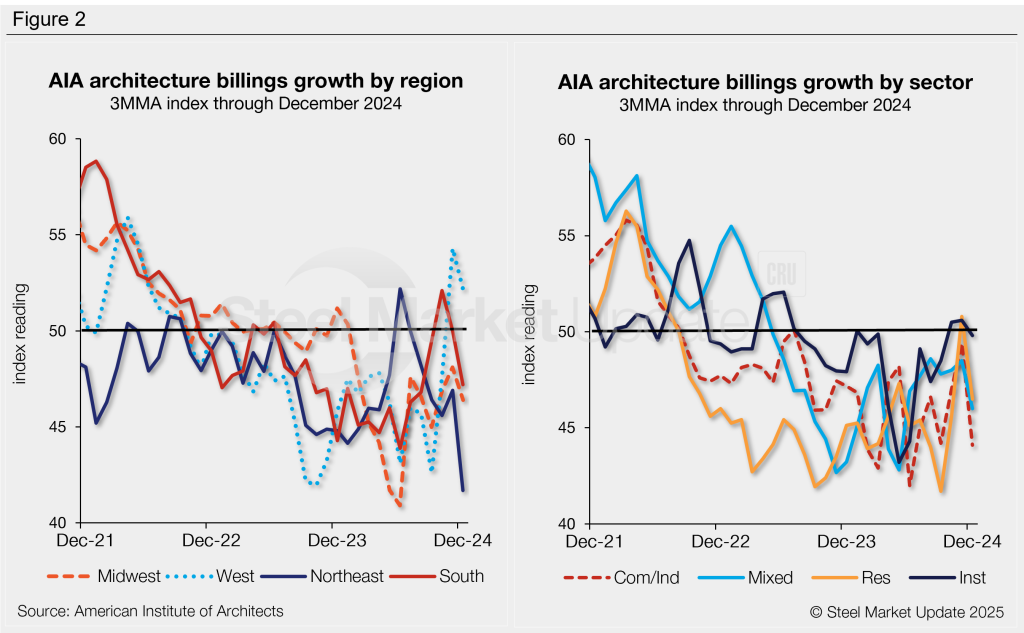

Each of the regional indices declined from November to December, with only the Western regional index above the 50 threshold (Figure 2, left). The Southern, Midwestern, and Northeastern indices continued to signal declines in billings.

All four of the sub-sector indices saw a decrease in billings in December (Figure 2, right). The institutional, residential, mixed practice, and commercial/industrial sectors all remain in contraction, a trend that has persisted for over a year now.

An interactive history of the December Architecture Billings Index is available here on our website.