Market Data

December 19, 2024

SMU Survey: Mill lead times contract slightly, remain short

Written by Brett Linton

Buyers participating in our latest market survey reported a slight contraction in mill lead times for both sheet and plate steel products, a reversal from the slight upticks seen in early December.

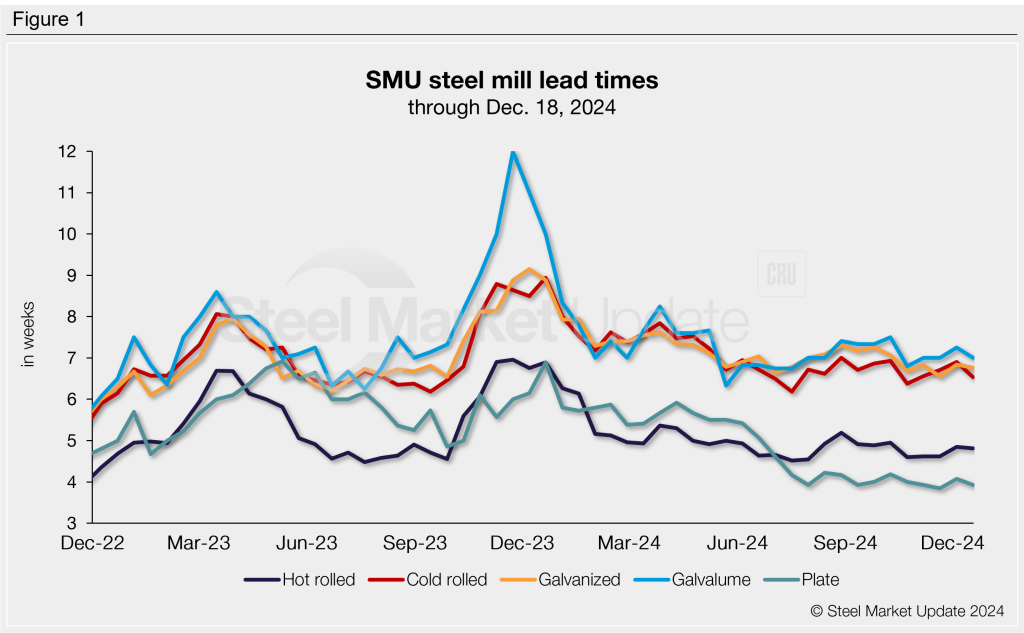

Production times this week are not far above the lows seen in July and November. Sheet product production times have been historically low since May, and plate production times have followed suit since July.

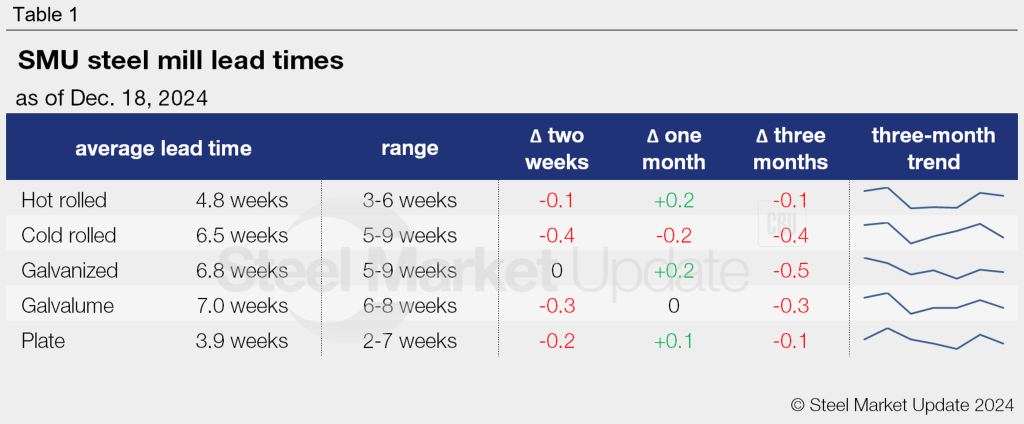

Average lead times for hot-rolled steel are holding in the upper four-week range. Tandem product production times are hovering around six to seven weeks. Plate lead times average just under four weeks.

Table 1 below summarizes current lead times and recent trends.

Figure 1 tracks lead times for each product over the past two years. Compared to our market check two weeks earlier, the lead time ranges changed this week for two of our five products. The longest galvanized lead time we considered increased from eight to nine weeks, and the top end of our plate range rose from six to seven weeks.

Survey results

Nearly half of the respondents we surveyed this week expect lead times to remain stable two months from now (49%). Almost as many foresee production times extending (48%), and the remaining few believe lead times could contract further. This has been the general trend for the past two months.

We also asked buyers to rate the current state of mill production times. Over half of respondents (58%) say lead times are shorter than usual, while the remaining 42% feel they are within typical levels. Not a single respondent voted that lead times today are longer than usual.

Here’s what respondents are saying:

“Lead times will remain relatively short.”

“Still short and will get back to average as buyers get back to replenishing stock.”

“Based on a small increase in demand, lead times will increase slightly.”

“I think they’ll extend in the next month and then settle down.”

“Longer lead times, I think we’ll see optimism in the first half of next year. Hopefully it will continue.”

“Lead times will extend, large projects will be filling available capacities.”

“They will contract as more capacity will be coming online and we expect demand to remain soft. Obviously imports/tariffs is the huge question mark.”

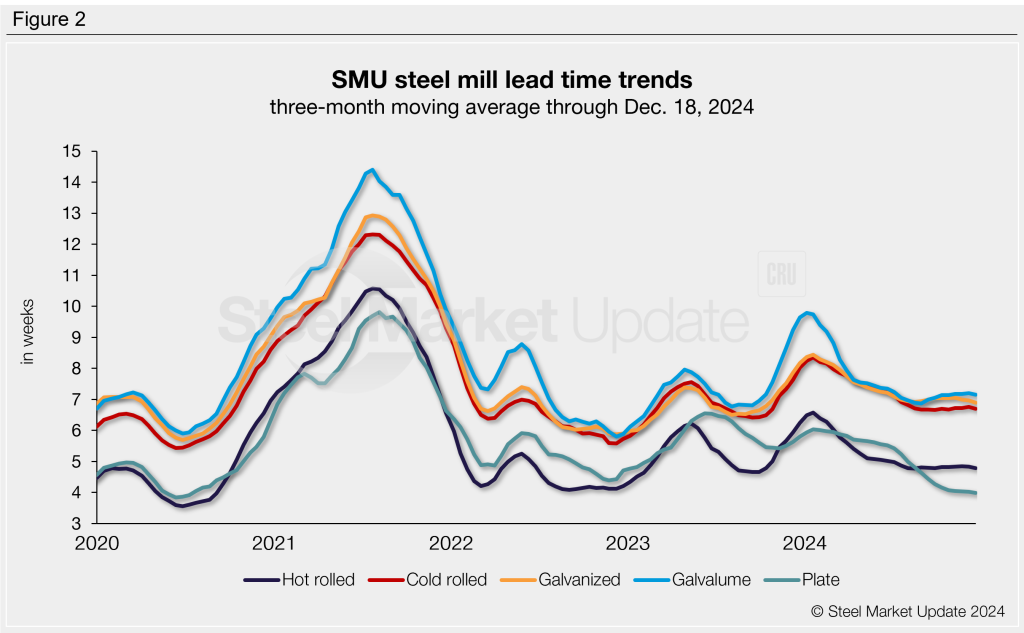

3MMA lead times

To smooth out variability in our biweekly data and better highlight trends, we can calculate lead times on a three-month moving average (3MMA) basis. As of Dec. 18, 3MMA lead times on both sheet and plate edged slightly lower. Overall, 3MMA lead times have been shrinking since the start of the year, leveling out in recent months near one-year lows.

The hot rolled 3MMA is now at 4.78 weeks, cold rolled at 6.70 weeks, galvanized at 6.89 weeks, Galvalume at 7.15 weeks, and plate at 3.99 weeks.

Figure 2 highlights lead time movements since the start of 2020.

Note: These lead times are based on the average from manufacturers and steel service centers participating in this week’s SMU market trends analysis survey. SMU measures lead times as the time it takes from when an order is placed with the mill to when it is processed and ready for shipping, not including delivery time to the buyer. Our lead times do not predict what any individual may get from any specific mill supplier. Look to your mill rep for actual lead times. To see an interactive history of our steel mill lead times data, visit our website. If you’d like to participate in our survey, contact us at info@steelmarketupdate.com.