Prices

December 10, 2024

HR futures: Volatility, tariffs, and global shifts - What's next for prices in 2025?

Written by Joshua Toney

Import arbitrations expressed via futures may become enticing as coil price spreads expand. The spread market in CME US hot-rolled coil (HRC) is currently navigating a period of volatility. Prices have fluctuated post-election, leaving traders uncertain about the market’s direction. A Trump trade structure formed pre-election, with Jan. ’25 peaking at $790 per short ton (st) in early November before dropping to $730/st by month-end. The Dec. ’24/Jan. ’25 spread decomposed from a high of -$50/st to -$27/st by the end of November, and the spread stood at -$38/st as of Dec. 4. These sharp shifts highlight the market’s lack of clear direction, making it challenging for participants to find consistent opportunities.

Dec. 4 – CME HRC Dec. ’24/Jan. ’25 Spread

Source: Bloomberg

Physical market participants are cautious and reluctant to increase inventory levels amidst uncertainty. While cash-and-carry trades remain viable due to the structure of CME HRC’s curve, the premium for forward sales is not sufficient to justify holding inventory. This is evident through the lack of deferred trading along the curve. For example, the Dec. ’24/Dec. ’25 price spread stood at -$105/st as of Dec. 4.

Taking current Nucor consumer spot price (CSP) offer levels at $750/st against underlying indices for Midwest HRC of $671/st, we have an approximate $122/st spread for spot against December 2025 as of Dec. 4. This hesitation is contributing to a broader sense of uncertainty in the market.

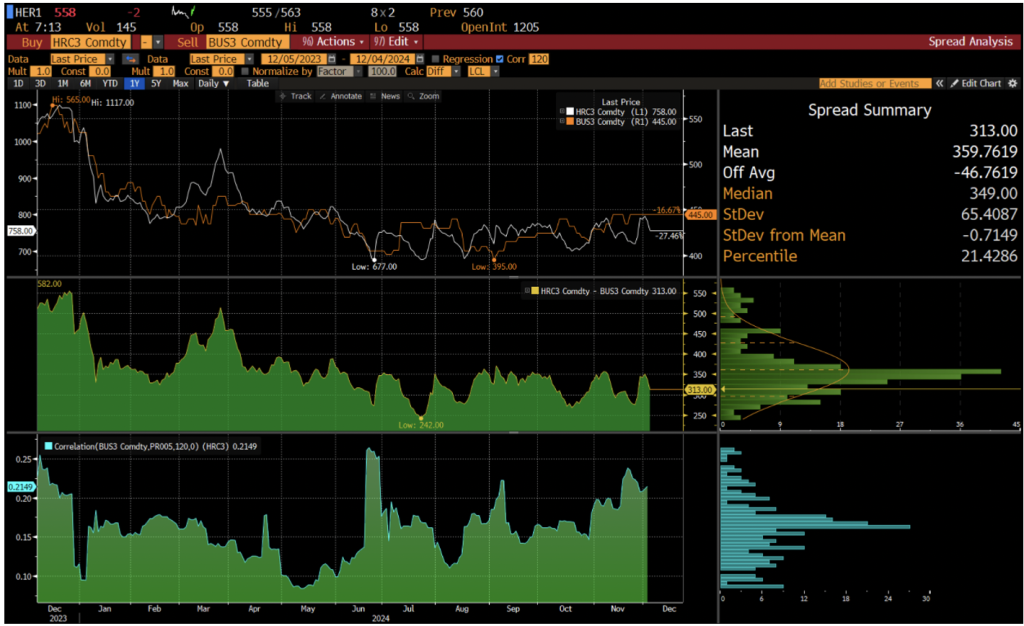

CME busheling futures

Absent from HRC’s price action, CME BUS futures have been relatively rangebound, with buying pressure materializing on screen for 2025 expiries. The CME HRC vs. CME BUS spread has found stability at $350 per gross ton for the rolling month three expiry. As of Dec. 4 is Feb. ’25, this is just shy of the one-year mean of $360/gt.

The launch of the CME Chicago Busheling (BUS) contract on Dec. 16 adds another layer of complexity. Declining participation in 2024 on the existing Midwest BUS contract is leading traders to anticipate a resurgence of BUS trading with the launch of the Chicago contract running in parallel for 2025. Expect to see enhanced liquidity and price discovery with the advent of this new contract.

Dec. 4 CME HRC /CME BUS Rolling M3 Spread (Feb. ’25)

Source Bloomberg

Despite these challenges, there is optimism that tariffs and protectionist measures may provide a turning point. Expectations for 2025 suggest tariffs could play a key role in stabilizing or even boosting US HRC prices. Although Chinese production remains aggressive and experienced a 4% contraction in November 2024 steel PMI, new tariffs on steel imports to the US could create a more favorable environment for US mills. This could enable them to raise prices further. We would expect the scrap price side of the electric-arc furnace (EAF) equation to improve if mills are able to capitalize on strength from implied tariff structures.

Additionally, the widening price spreads between US HRC and international markets could offer arbitrage opportunities. Futures markets in the global HRC sector could become more attractive as spreads expand. This could provide traders with avenues to capitalize on pricing shifts from Europe, the US, and Asia.

The US HRC market is at a crossroads. Volatility continues to define price action. However, external factors like tariffs, arbitrage opportunities, and shifting scrap dynamics could offer significant upside. As 2025 approaches, all eyes will be on evolving trade policies, scrap supply conditions, and the performance of the new CME BUS contract. While the path forward remains uncertain, the market holds potential for recovery and growth.

Disclaimer: This report was approved and issued by Marex Financial, a company within the Marex group. Marex Financial is incorporated under the laws of England and Wales (company no. 5613061 and VAT registration no. GB 872 8106 13), is authorized and regulated by the Financial Conduct Authority (FCA registration number 442767) and is a member of the London Stock Exchange. Marex Financial’s registered address is at 155 Bishopsgate, London, EC2M 3TQ. Nothing in this report constitutes (i) an offer of services, (ii) an offer to purchase or sell investments or any other product or (iii) investment, tax or legal advice. The report has been approved and issued on the basis of publicly available information, internally developed data and other sources believed to be reliable. It has been prepared for the general information of Marex’s institutional clients, is not directed at retail customers and does not take into account particular investment objectives, risk appetites, financial situations or needs. Recipients should make their own trading decisions based upon their own financial objectives and financial resources. This report is a marketing communication. It is not investment research and has not been prepared in accordance with legal requirements designed to promote investment research independence. The report is not subject to any prohibition on dealing ahead of the dissemination of investment research. Whilst reasonable care has been taken to ensure that facts stated are fair, clear and not misleading, Marex does not warrant or represent (expressly or impliedly) their accuracy or completeness. Any opinions expressed are those of the author of the report as at the date of the report and not necessarily those of Marex and, in any event, may be subject to change without notice. Marex accepts no liability whatsoever for any direct, indirect or consequential loss or damage arising out of the use of all or any of the data or information in this report. This report is not intended to be an offer to buy or sell any securities of any company referred to herein nor any other transaction or investment. This report is not intended for use by any other person than the addressee. If you are not the addressee, please delete it and immediately notify the Group Compliance department at Marex. This report may not be distributed in any jurisdiction where its distribution may be restricted by law. Additional material relating to any security, transaction or investment referred to in the report may be made available on request. No part of this report may be redistributed, copied or reproduced without the prior written consent of Marex. You must not distribute any part of this report to any other person without attaching a copy of this information.