Logistics

December 4, 2024

Reibus: November flatbed rates cool after October bump

Written by Robert Martin

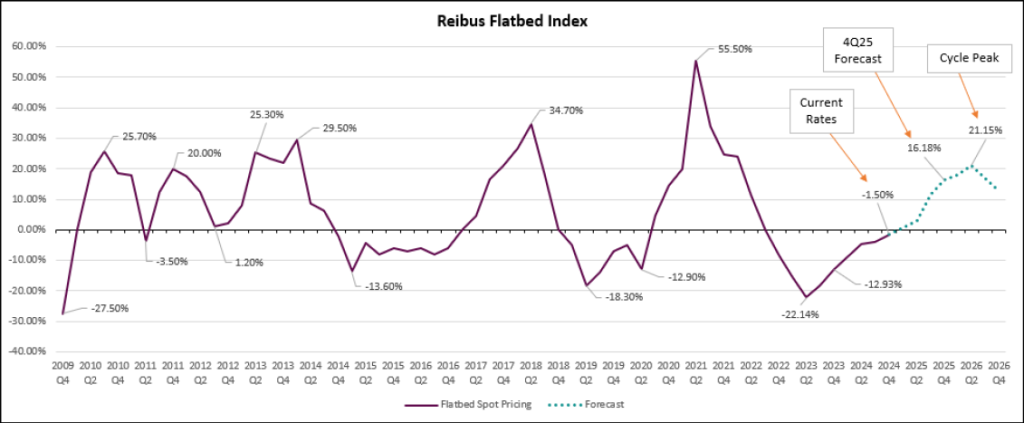

After closing the third quarter -3.84% on a year-over-year (y/y) basis, it appears the fourth quarter Flatbed Index will land right around -1% y/y.

After a slight bump in rates in October, November cooled off, dropping flatbed rates by 2.5% month over month (m/m), effectively returning to where they stood in September.

As noted in our last column, it is likely the higher October rates were merely the after-effects of hurricanes Helene and Milton and the short-lived East Coast port labor strikes we saw from Oct. 1-3. As historical seasonal trends would tell us, absent a black swan event, flatbed rates seeing upward pressure in the colder months of the year is a rarity, so it is likely we’ll have to wait until 1Q’25 to see any real movement.

Overall, flatbed market conditions remain relatively calm. Load-to-truck ratios have fallen from their recent Q3’24 highs with only a few markets still showing tightness. The Pacific Northwest has tightened due to seasonal demand for shipping Christmas trees and winter weather, while certain pockets in the South remain tight. While progress has been slow, the Flatbed Index continues to grind along and, so far, continues to trend toward inflationary in around Q1’24. With the short-lived East Coast port labor strike having much more bark than bite, we now turn toward the Jan. 15 deadline to reach a long-term agreement. The October strike could turn out to be a preview of the main event.

As we move into what appears to be an inflationary market in 2025, we expect the delta between spot and contract shipments to shrink and reverse course, with spot rates overtaking contract rates and moving markedly higher as we’ve seen during the past 20+ years of market cycles.

As spot rates begin to exceed contract, we should expect tender rejections to increase and revert, not to 2021 levels, but something resembling the 2018 inflationary market. We should continue to see what used to be shorter-term quarterly and 6-month bids increasingly move toward 12-month and even longer-term commitments as procurement teams attempt to lock up capacity. It will then become a question of whether carriers will honor those commitments and to what extent. These things tend to balance out, and shippers who re-bid their networks prior to contract periods expiring should expect the same in return.

The macroeconomic data has continued to show tepid results in Q4’24 with overall consumption pointing higher but industrial production pointing lower. These are lagging data points and there continues to be optimism surrounding Q1’25 and 2025 as whole.

It remains to be seen what impact the new administration’s potential tariffs will have on the economy. Tariffs make imports less competitive and are intended to boost domestic production, which should result in a boon for domestic manufacturing. Historically, higher tariffs on Chinese imports have been linked to increased US manufacturing output. Therefore, the anticipated tariffs could revitalize a stagnant manufacturing sector, thus boosting the demand for shipping services domestically.

Editor’s note: The views, thoughts, and opinions expressed in the content above belong solely to the author and do not necessarily reflect the opinions and beliefs of Steel Market Update or its parent company, CRU Group.