Market Data

November 8, 2024

SMU Survey: Steel Buyers' Sentiment Indices less optimistic this week

Written by Brett Linton

SMU’s Steel Buyers’ Sentiment Indices continue to show that steel buyers are optimistic about the success of their businesses, though that confidence has eased compared to earlier in the year.

Previously at a four-year low, our Current Steel Buyers’ Sentiment Index saw a slight uptick this week, while Future Buyers’ Sentiment tumbled to a three-month low.

Every other week, SMU surveys hundreds of steel buyers about their companies’ chances of success in today’s market and business expectations for the next three to six months. Responses are used to calculate our Current Steel Buyers’ Sentiment Index and Future Sentiment Index, measures we have tracked since SMU’s founding in 2008.

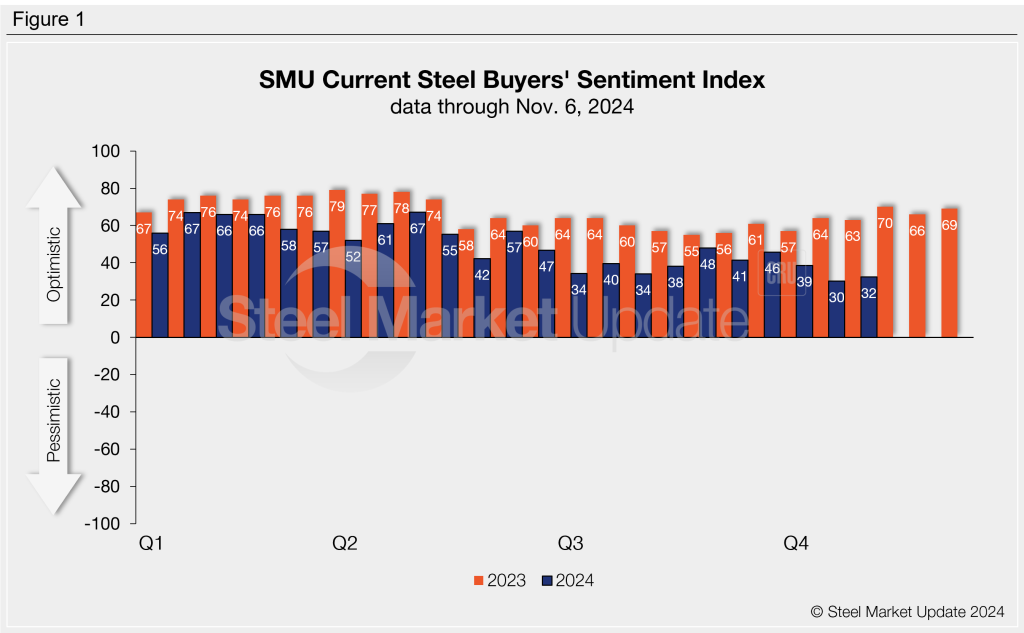

Current Sentiment

This week, SMU’s Current Buyers’ Sentiment Index rose two points to +32 (Figure 1). Just two weeks ago, Sentiment had dropped to the lowest point since May 2020, surpassing the +34 low recorded in July of this year. This time last year Current Sentiment was significantly stronger, standing at +63.

Across the first 11 months of 2024, Current Sentiment has averaged +49. This is considerably lower than the same time period of 2023 when the average was +67.

Future Sentiment

SMU’s Future Buyers’ Sentiment Index saw a sharp 15-point decline this week, settling at +56 (Figure 2). This is the largest survey-to-survey decline witnessed in two and a half years. In late October Future Sentiment had climbed to +71, the second-highest reading seen this year. Recall that in early August, Future Sentiment fell to a one-year low of +55, quickly recovering to a nine-month high of +72 just two weeks later.

Since the beginning of this year, Future Sentiment has averaged +65. This is down two points from the same period last year. This time one year ago Future Sentiment stood at +66.

What SMU survey respondents had to say:

“I expect early 2025 demand to be soft.”

“Expect market conditions to improve once the election dust settles.”

“We remain conservative but well informed.”

“I feel jobs will be opened up and money will start to flow in for more work.”

“Only fair as costs are increasing in 2025.”

“Hard to know about future economic activity and the trade environment.”

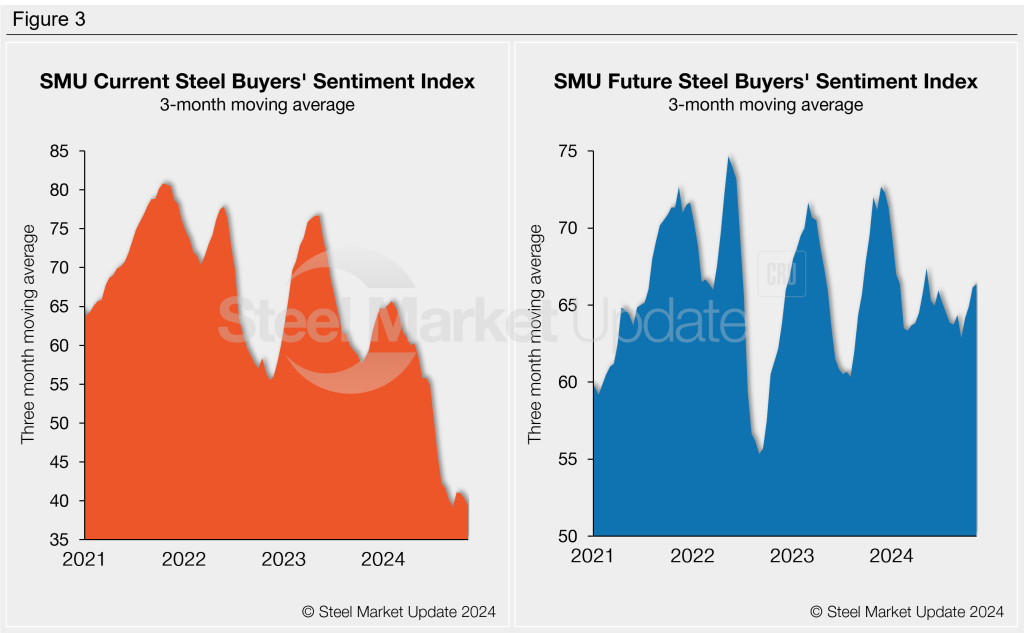

Moving averages

When analyzed as a three-month moving average, Steel Buyers Sentiment moved in differing directions this week (Figure 3).

As of Nov. 6, the Current Sentiment 3MMA eased to +39.37, just above the four-year low of +39.20 recorded in mid-September. For most of this year, Current Buyers’ Sentiment has trended downward. Meanwhile the Future Sentiment 3MMA increased to a six-month high of +66.36 this week, a gradual recovery following the one-year low observed in early September.

About the SMU Steel Buyers’ Sentiment Index

The SMU Steel Buyers Sentiment Index measures the attitude of buyers and sellers of flat-rolled steel products in North America. It is a proprietary product developed by Steel Market Update for the North American steel industry. Tracking steel buyers’ sentiment is helpful in predicting their future behavior. A link to our methodology is here. If you would like to participate in our survey, please contact us at info@steelmarketupdate.com.