Analysis

October 25, 2024

Drilling activity stable in the US and Canada

Written by Brett Linton

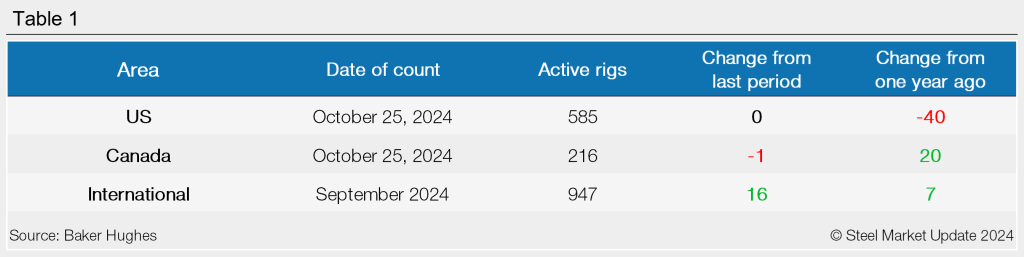

The number of operating drilling rigs in the US held steady last week, while Canadian counts eased by one, according to the latest figures released by Baker Hughes.

US rig activity remains near multi-year lows, hovering within a narrow range over the last five months. Canadian counts have stabilized in recent weeks but remain near some of the highest levels recorded in the past seven months.

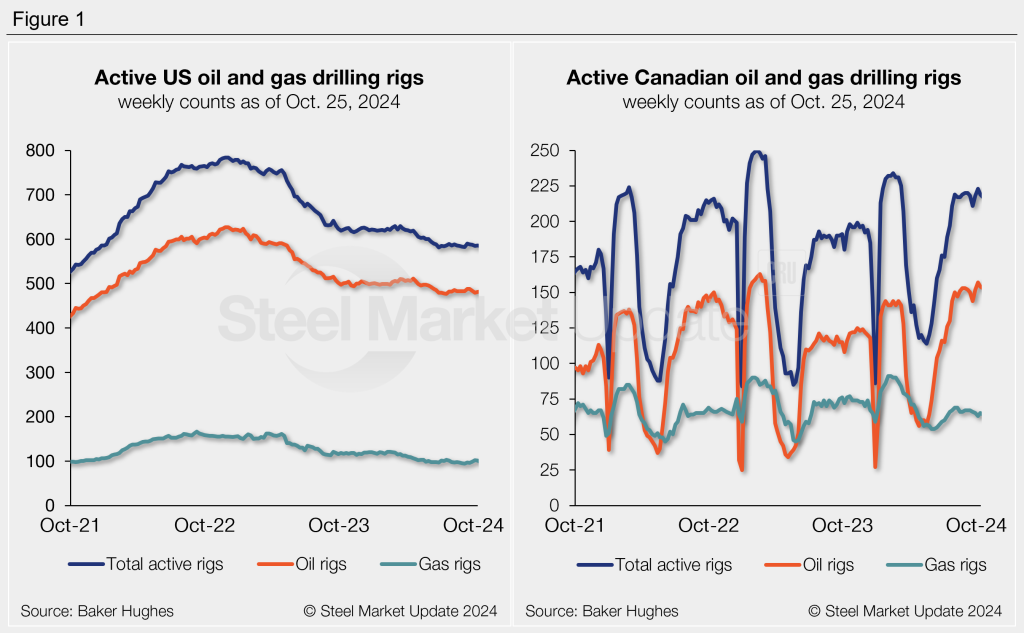

US counts

Through Oct. 25, there were 585 drilling rigs operating in the US, in line with the prior weekly count. The number of oil rigs fell by two week over week (w/w) to 480, gas rigs rose by two to 101, and miscellaneous rigs were unchanged at four.

There were 40 fewer active US rigs last week compared to the same week one year prior, with 24 fewer oil rigs and 16 fewer gas rigs.

Canadian counts

There were 216 active Canadian drilling rigs as of last week, one less than the prior week. Oil rigs fell by three w/w to 150, gas rigs rose by two to 66, and miscellaneous rigs were unchanged at zero.

There are currently 20 more Canadian rigs in operation than levels one year ago, with 28 more oil rigs and eight fewer gas rigs.

International rig count

The international rig count is a monthly figure updated at the beginning of each month. The total number of active rigs for the month of September rose to 947, up 16 from the August count and seven more than levels one year prior.

The Baker Hughes rig count is important to the steel industry because it is a leading indicator of demand for oil country tubular goods (OCTG), a key end market for steel sheet. A rotary rig rotates the drill pipe from the surface to either drill a new well or sidetrack an existing one. For a history of the US and Canadian rig counts, visit the rig count page on our website.