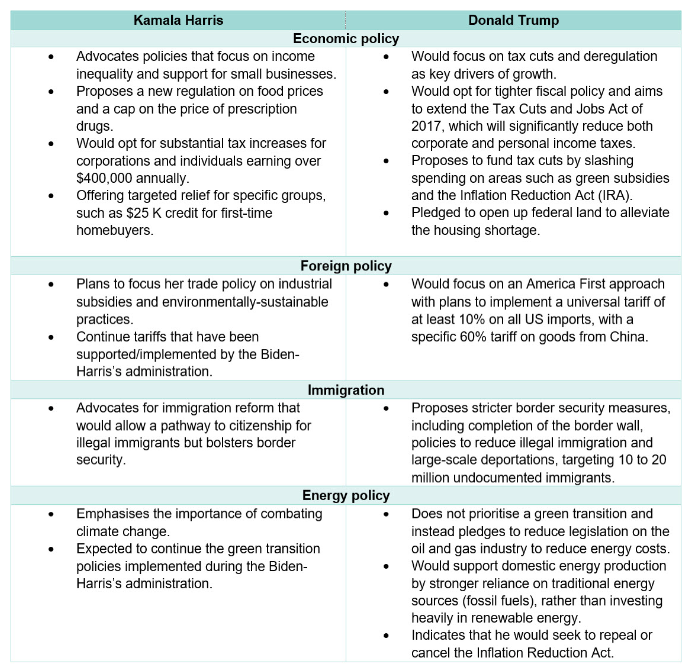

Analysis

October 25, 2024

CRU: What will the US elections mean for economic policy?

Written by Alex Tuckett & Veronika Akhmadieva

SMU is pleased to share this Insight piece from CRU economists. You can visit the CRU website to learn about its global commodities research and analysis services.

US 2024 presidential candidates Donald Trump and Kamala Harris offer contrasting visions for the future. Trump proposed universal tariffs and a strict stance on immigration, which would be highly inflationary. Harris’s preference for higher taxes and more regulation could create economic growth headwinds of their own. Both candidates proposed policies that would be supportive of the construction sector, and while Trump’s preference for lower taxes and deregulation can be supportive in the short term, Harris’s plans around green transition might better position the US economy over the medium to long term. This Insight explores the possible economic effects of each candidate’s agenda.

We discuss the climate policy implications of the election in a separate Insight, “Harris or Trump: What does it mean for US climate policies?“

Competing visions for America’s economic future

Below, we summarize Trump and Harris’s agendas, which are likely to have direct implications for the commodity markets.

The economic impact of Trump’s 2024 proposals

Trump’s proposed policies are likely to be highly inflationary. However, lower taxes and deregulation can support growth in the short run.

Trump’s proposal for mass deportations could substantially shrink the workforce, challenging businesses’ ability to meet current demand levels. Research from the Peterson Institute for International Economics suggests that deportation of even 7.5 million undocumented workers – less than Trump’s proposal – would drive inflation higher and reduce GDP. Combined with large tariff increases, a reduced labor force could reinvigorate inflation, making planned interest rate cuts less probable.

Trump’s proposed universal tariff aims to protect American companies from foreign competition by making US-produced goods more affordable relative to imports, while also increasing government revenue. However, a recent Goldman Sachs report underscores the inflationary risks tied to Trump’s tariff plan, estimating that a one percentage point increase in tariff rates could raise core inflation by 0.1 percentage points. Similarly, a study from the US International Trade Commission found that Trump’s 2018 tariffs on Chinese goods led to a 0.2% rise in domestic prices. While businesses previously absorbed many of these costs, the broader tariffs now proposed could place a heavier burden on consumers.

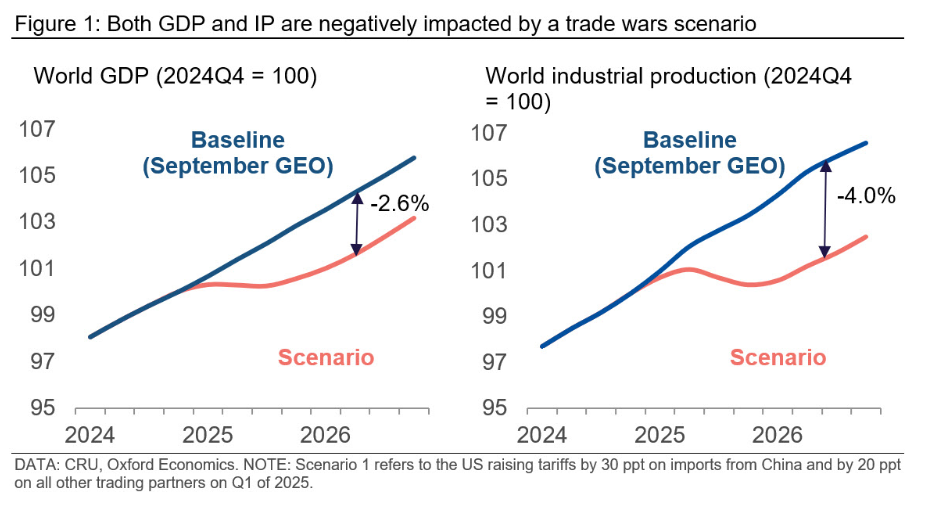

The universal tariff proposal is also likely to provoke retaliatory measures from other nations as they seek to protect their own economies. Such responses could intensify global economic strains, as seen with China’s actions during Trump’s first term. Our scenario analysis suggests that a multilateral trade war could reduce global GDP by approximately 2.5% and decrease industrial production by 4% (Figure 1).

Such a sweeping tariff could lead to a stronger US dollar if trading partners respond with more lenient monetary policies to offset weaker exports. A stronger dollar could, in turn, diminish some of the intended price increases on imports, reduce US export competitiveness, and put downward pressure on commodity prices.

However, Trump’s plan to extend the 2017 Tax Cuts and Jobs Act would maintain the corporate tax rate at 21% (down from the previous 35%) and continue to lower personal income tax rates. This continuation would spur US investment, raise wages, and increase disposable income.

The economic impact of Harris’s 2024 proposals

Kamala Harris’s agenda might translate into economic growth headwinds in the short run but lead to more sustainable growth in the medium to long term.

While Harris’s proposed policies are expected to be less inflationary than Trump’s proposals, some of them can still contribute to upward price pressures. The increase in disposable income for many Americans could spur demand and push prices higher. However, Goldman Sachs contends that these inflationary impacts would likely be tempered by Harris’s other policy measures.

To increase government revenue, Harris proposes raising corporate and individual tax rates, particularly targeting high-income earners. Her plan includes raising the federal corporate tax rate from 21% to 28% and increasing the federal income tax rate for individuals earning over $400 K from 37% to 39.6%. Higher corporate taxes and increased capital gains taxes may reduce investment in capital markets and elevate corporate costs.

Harris is also likely to advocate for more stringent regulations on corporations, which could further increase operating costs, slow performance, and decrease profit margins. Goldman Sachs analysts estimate that these measures would reduce S&P 500 earnings by approximately 5%, with additional tax burdens potentially leading to further economic headwinds.

To support small businesses and families, Harris proposes a series of tax breaks, including up to $50,000 in relief for small businesses, an expansion of the child tax credit to $6,000 for the first year, and a $25,000 tax credit for first-time homebuyers.

Kamala Harris’s trade policy is expected to align closely with the Biden administration’s approach, focusing on multilateral cooperation and fair trade while encouraging domestic production through tax incentives. Her agenda will support a transition to green energy, building on the foundations of the Inflation Reduction Act (IRA). Since its implementation under Biden, the IRA has driven over $250 billion in investments into US energy projects and has contributed to the creation of over 100,000 jobs in the energy sector. However, it is also the most expensive energy policy in US history, raising concerns about long-term fiscal impacts.

Overall, however, the analysis suggests that Harris’s economic policies could result in a modest GDP growth boost between 2025–2026, with a limited effect on inflation. Nevertheless, the precise impact of her policies remains uncertain, as the magnitude of these effects can vary.

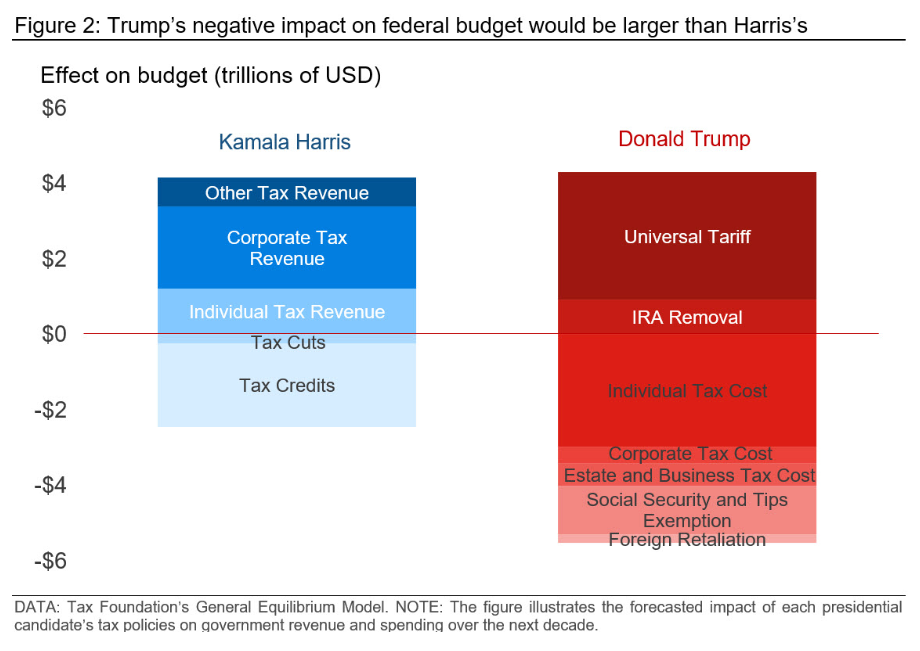

How would Trump and Harris shape the nation’s budget?

In 2023, the US recorded a fiscal deficit of 8% of GDP; similar figures are expected for this year. This level of deficit is unusually high, particularly given the current state of full employment. Both the International Monetary Fund (IMF) and key government officials in Washington have voiced serious concerns about the rapidly growing deficit, urging policymakers to take swift action.

As the 2024 election approaches, the fiscal impact of the candidates’ economic proposals has become a central issue. Trump and Harris offer distinct approaches, each with significant implications for the national budget. According to projections from the Tax Foundation, a Trump presidency could lead to a net worsening of the federal deficit over the next decade. Harris’s policies would also have substantial effects on the budget due to her proposed tax increases and spending initiatives. The effects of each candidate’s policies are outlined below (Figure 2).

It is important to emphasize that if the Senate and House of Representatives end up being split between Democrats and Republicans, pushing through further fiscal stimulus could be a challenge, raising the risk of a recession in 2025.

In conclusion, the two candidates’ policies present very distinct potential economic implications. Trump’s tax cuts and supply-side policies might spur high inflation growth, increasing the likelihood of interest rates getting pushed higher. Harris’s proposed policies, including higher taxes and more regulation, could lead to slower economic growth, mild inflation pressures, and a modest decline in interest rates in the short term. However, her focus on green initiatives and infrastructure spending could boost growth in the coming years. At this point, the presidential race remains too close to call, with uncertainty around the outcome of the election weighing on growth in Q4.

With additional contribution from Maria Garcia, economist.