Prices

October 17, 2024

HR futures: Support fails as market slows ahead of election

Written by David Feldstein

After a relatively stable and boring September, CME hot-rolled coil (HRC) futures have been on the move lower thus far in October. Since Sept. 30, the November and December futures have declined $63 and $65, respectively, with the curve’s contango steepening.

CME hot-rolled coil futures curve $/st

The November future traded down to a new low of $720 on Aug. 16 before rebounding to $780 only six trading sessions later. The November future traded back down once again testing the $720 low on Sept. 4 and 5 before rebounding one more time, ultimately trading to as high as $799 on Sept. 25. On Oct. 9, the November future tested the $720 low for the third time. It printed as low as $714, but then settled that day at $725, back above what was looking to be a decent support level. However, the $720 level failed to hold with the November future, having settled below $720 in each of the past four trading sessions. At 5:14 am CT on Thursday, it fell to a new intraday low, trading one lot at $666 before trading back up to settle the day up $7 at $702.

November CME HRC future $/st

Similarly, the December future had found support around the $730 level, but like the November future, the support level failed. The December future has settled below $730 the past three sessions, trading as low as $690 late last night before moving back to about unchanged, settling at $710.

December CME HRC future $/st

The fizzle heard round the world. One reason for this morning’s early aggressive selling was a much anticipated announcement out of China’s government with hopes it would provide concrete details with respect to their latest round of economic stimulus measures. As you can see in iron ore’s response below, the actual stimulus was ‘underwhelming.’ For now, you can cross a global Chinese stimulus led commodity rally off the bullish factors list.

Rolling 2nd month SGX iron ore future $/mt

Back on the home front, perhaps the HRC market is not as bad as the futures make it seem. The initial determination in the CORE trade case is scheduled for Monday. There was a massive increase in imports of tandem products in the first half of 2024, but imports of HRC remained flat as exhibited by the three-month moving average in green. Moreover, it seems a reliable assumption that 2025’s flat rolled imports will be down notably on a year-over-year (y/y) basis due to weak market sentiment, relatively unattractive spreads for months, and uncertainty related to the CORE trade case. If that assumption proves correct, then those swing tons should move back into the hands of the domestic mills.

Imports – HRC sheets

We are less than three weeks away from the 2024 presidential and congressional election and how the market has slowed. How much of the slowdown is due to members of the supply chain sitting on their hands waiting to know the outcome of the election?

Consider how much energy surrounds each and every Federal Open Market Committee (FOMC) meeting. Financial markets slow down a week or a few days ahead of the meeting. On the day of the announcement, the financial market news channels are packed with commentary and expectations of what the Fed will do. Then at 1 pm CT, the FOMC announces their decision with Mike McKee of Bloomberg or Steve Liesman at CNBC revealing the news. Financial markets react violently and then calm ahead of the 1:30 press conference. Every word of Fed Chair Jerome Powell’s comments are scrutinized as the markets swing in response to each answer. Finally, Powell wraps up the Q&A while the markets continue to react into the close as financial pundits comment on the day’s events well into the evening. All of this over whether the Fed moved interest rates by 25 basis points or 50 basis points, and what they might do at the next meeting 30 to 60 days out.

Now put the magnitude of a Fed decision in the context of what is going to happen over the next four years as determined by the winner of the US presidential race, and to a lesser extent control of congress. Regardless of who wins, there will be massive winners and losers as a result. For instance, if the Republicans win, the oil and gas industry will benefit. However, if the Democrats win, solar and wind will undoubtedly be favored. Those are easy examples, but the list of industry winners and losers depending on the outcome runs deep. Thus, it is no surprise that the steel industry and economic decision-making writ large slows down weeks before the election just like financial markets slow hours before the FOMC decision.

Furthermore, irrespective of the winner, simply knowing the outcome of the election and pushing the uncertainty aside triggers a wave of business planning and decision making. Thus, how much of the current malaise in the steel industry is due to the uncertainty surrounding the election? More importantly, how will the market react three weeks from now once that uncertainty is resolved? Will it unleash pent-up demand?

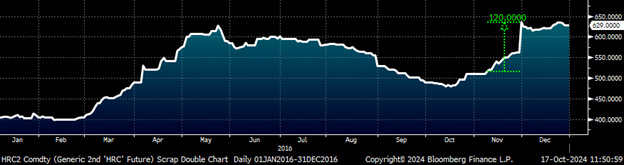

The steel price saw a pop following the past two elections in 2016 and 2020. On Nov. 8 of 2016 (election day), the rolling 2nd month Midwest HRC future settled at $515, before shooting up $120 to $635 on Nov. 30.

Rolling 2nd month CME HRC future $/st – 2016

On Nov. 3, 2020 the rolling 2nd month future settled at $698. While it was Democrat Joe Biden that won this time, steel prices still jumped $143 to settle at $841 on Nov. 30.

Rolling 2nd month CME HRC future $/st – 2020

Look folks, I was born into a middle class family. Now we can debate which candidate is better for the steel industry, perhaps whether one of the candidates could be the greatest president of all time for the steel industry. Regardless of who is better for steel and regardless of who wins, we do know that human beings do not like uncertainty, that businesses do not like uncertainty. We do know that a tremendous amount of uncertainty about the next four years will be lifted on Nov. 5.

Disclaimer: The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Mr. Feldstein should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.