Analysis

August 30, 2024

CRU Insight: Decarbonization will reshape global steel trade flow

Written by Juliana Guarana & Yusu Mao

CRU’s Steel Long Term Market Outlook presents a comprehensive analysis of global steel trade flows until 2050. Decarbonization will play a significant role in redefining trade patterns by shifting regional competitiveness and increasing steel demand needs.

In part one of this CRU Insight series, we illustrate how decarbonization intensifies trade regionalization and alters the competitive landscape. In part two, we will look at decarbonization-led demand and trade growth, focusing on matured economies.

Protectionism will increase as decarbonization efforts arise

Although global steel demand is expected to rise, CRU’s Steel Long Term Market Outlook projects that steel trade volumes will decline in the long term across the globe and steel supplies will become increasingly regionalized.

One of the key drivers for this regionalization will be protectionism, which has been rising in recent years and is expected to increase further due to decarbonization efforts in different regions. A proliferation of different new policies and Emissions Trading Schemes (ETS) similar to the European Carbon Border Adjustment Mechanism (CBAM) will potentially be implemented globally to avoid carbon leakage, or in other words, the transfer of production from a jurisdiction with high emission constraints to a jurisdiction with fewer constraints.

Numerous governments globally have already started to work on domestic carbon pricing and trading schemes to create a level playing field and protect domestic producers, such as the UK, Serbia, Turkey, Australia and China.

The emergence of new carbon pricing schemes will eventually lead to the establishment of carbon clubs among like-minded countries, in which members would adhere to agreed environmental standards – for example maximum emission intensities – in return for recognizing each other’s domestic policy regimes.

These emerging ETS will reconfigure international trade flows and, most importantly, lead to structural changes in steel costs and prices.

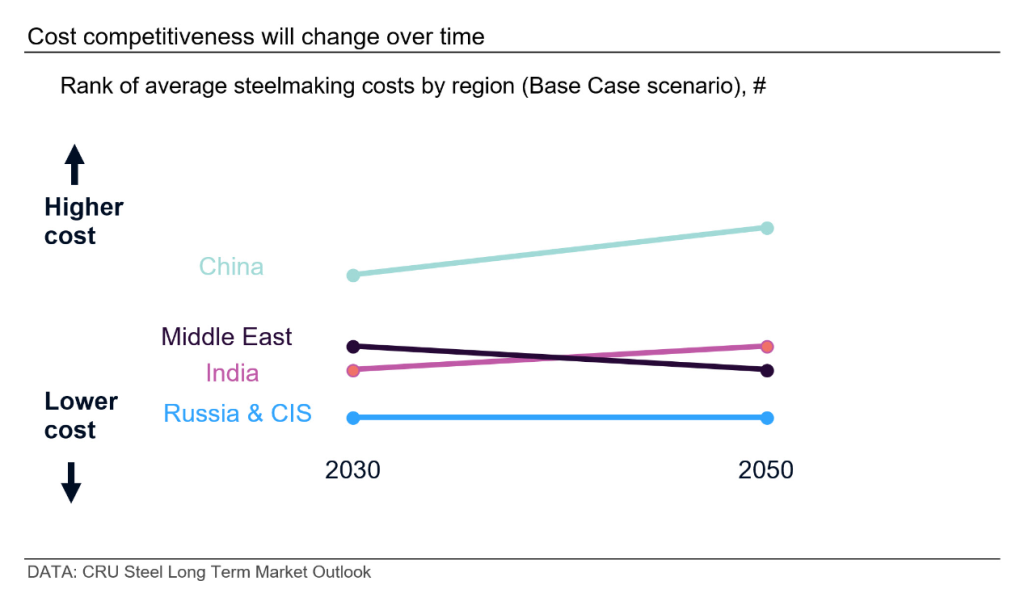

Different decarbonization paths will shift the steelmaking cost landscape

Different regions are moving on different paths towards net zero and the decarbonization of the steel industry, depending on decarbonization targets and the level of policy responses, as well as the local economic and steel demand profiles. Resource availability – such as raw materials and energy, the age of existing assets, and technology readiness – will also influence the diffusion of new steelmaking technologies and the decarbonization time scale globally.

In our Steel Long Term Market Outlook analyses, regional cost competitiveness changes between 2030 and 2050 based on projections of new steelmaking technologies deployment, which are aligned with regional progress toward decarbonization. Overall, regions that have stringent decarbonization targets and powerful market tools to ensure targets will be met will face higher production costs due to the substantial investments required to adopt abatement technologies.

In parallel, lower-cost suppliers facing less pressure to invest heavily in decarbonization (either because of a low level of policy ambition or strong cost competitiveness of low-emission steel production) will increase their share in global exports, especially Russia and CIS, India, and the Middle East. Russia and CIS will remain the most cost-competitive regions and are expected to ramp up exports after a recovery phase from the Ukraine war. India will also be positioned at the lower end of the cost curve, given the fast pace of capacity expansion in the country.

In our alternative case scenario, in which we assume decarbonization will accelerate even further than in the base case scenario, Indian exports are expected to decrease due to the high-emission profile of the country’s supply. In this scenario, China and the Middle East are expected to be better positioned than India as low-emission steel suppliers by 2040.

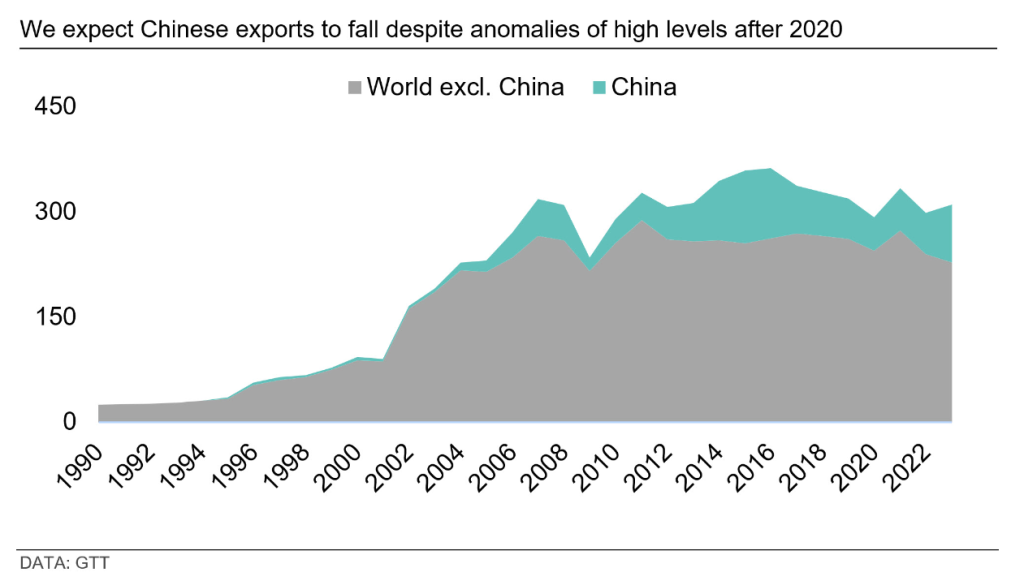

Chinese steel exports will fall alongside capacity constraints

We expect Chinese steel exports will decline significantly in the long term as the country transitions from an investment-led growth model to a higher value- and services-led growth one.

Over the last five years, the Chinese government initiated production control to reduce emissions from the steel industry, and in line with the country’s decarbonization targets, we believe this trend will continue in the medium-to-long term. We expect that the output reduction in China will outweigh the expected reduction in the country’s domestic demand, leading to lower exports. This is also in line with the country’s strategy to focus on quality growth, meaning more higher-value-added manufacturing exports.

Additionally, steelmaking costs will move structurally higher in China from 2035 onwards due to the deployment of new technologies. For China, exports account for only a small share of total steel production. Hence, external carbon-related trade barriers such as CBAM are not enough to empower the industry’s transition. Policy will be the main driver, while the timeline of it remains a key uncertainty.

China’s share of global steel exports will fall in the long term, but the country will still be a major steel exporter, particularly in the APAC region. Accelerating economic development in Southeast Asia will support significant steel demand growth in the region, with China remaining its marginal supplier.

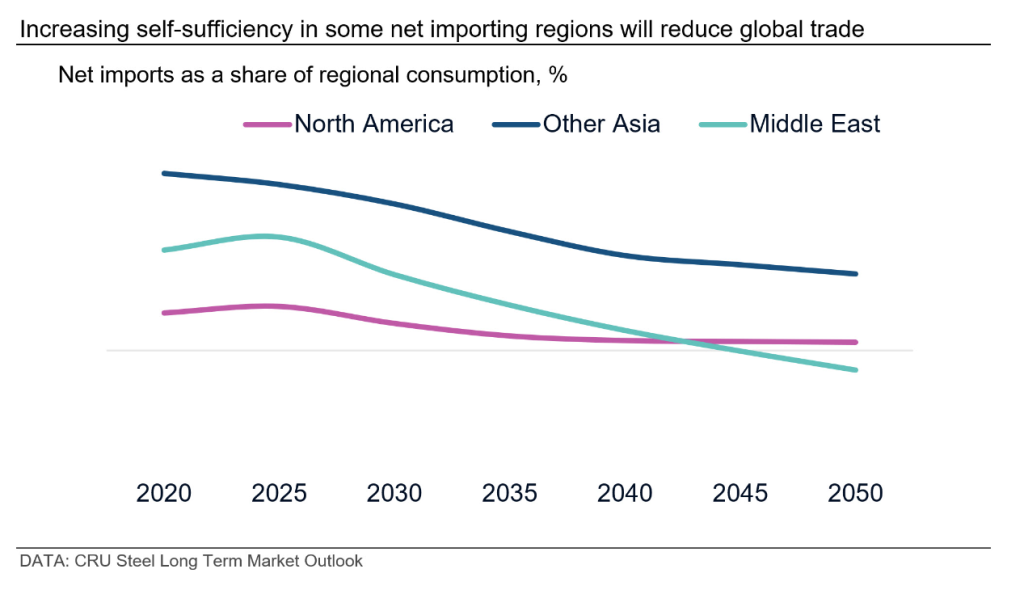

The Middle East will become a low-emission steel net exporter after 2040

CRU’s Steel Long Term Market Outlook projects that steel supply will become increasingly regionalized, with many regions achieving a higher level of self-sufficiency and domestic suppliers taking a larger share in demand growth. North America, the Middle East, and Southeast Asia are regions that are already investing in new capacity to meet future demand growth. Production growth is expected to outpace that of demand in some of these regions, reducing import demand.

The Middle East will change from a steel net importer to a net exporter after 2040, and part of the change in its net trade balance is via increasing low-emission steel to developed markets. The region is expected to focus on expanding domestic low-emission steel production by taking advantage of its abundant and low-cost natural gas supply. We expect local producers will also invest in green-hydrogen DRI-EAF steel production, which we believe will be one of the key steel decarbonization technologies in the future. Future global demand for low-emission steel is expected to increase and we expect Middle Eastern producers to capture a share of this market.

This Insight article was first published by CRU. To learn more about CRU’s services, visit www.crugroup.com.