CRU

August 7, 2024

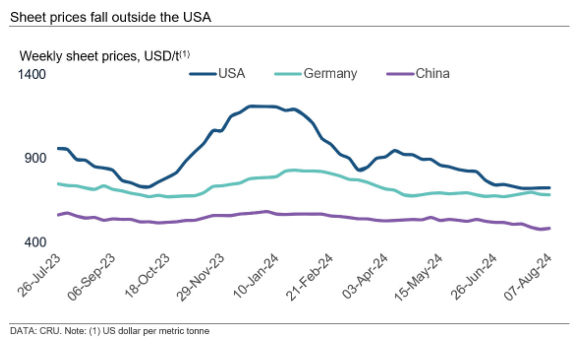

CRU: US prices find a bottom as other markets fall

Written by Ryan McKinley

The US sheet market appears to have reached a bottom following consistent weekly declines since April. However, other markets remain weak due to limited demand. Trading in Europe has been slow due to summer holidays. While European mills are also undergoing maintenance outages, these have not been enough to offset ongoing price falls, with weak demand still outweighing supply. Softer demand can also be seen in China, where the country’s PMI held in contraction for another month. Attempts to increase offers in other parts of Asia were met with resistance, and buyers in India continue to hold sufficient inventory levels as construction activity remains low due to heavy rainfall.

USA

HR coil prices were little changed for a third week in a row, with our first assessment in August coming in $1 per short ton (st) above last week at $659/st. CR coil prices rose by $9/st to $927/st, while HDG coil base prices declined by $8/st to $859/st

The general consensus among market participants this week was that prices have now reached a bottom, and the market is poised to turn higher. However, the magnitude of a price increase will be limited by lackluster demand, and buyers said they are in no rush to jump into the market to beat said increase. On top of this, doubt that demand will recover meaningfully this year, potential macroeconomic headwinds, and uncertainty regarding other geopolitical developments have made some buyers take a more cautious stance toward purchasing activity.

However, we have also seen some large-volume, low-priced deals take place recently, which may help extend mill lead times soon. Increases in publicly announced price levels from mills appear to be gaining some traction, which helps support this notion. In some cases, sellers said that upcoming maintenance outages may be enough to tighten for yet more price increase announcements to be realized.

Europe

European sheet prices were mostly down last week amid seasonally slow trading activity, especially in Italy, where all sheet products have decreased by between €6–14/metric ton (mt) w/w. German and Italian HR coil were assessed at €626/mt and €616/mt, respectively, down by €10/mt and €14/mt.

Buying activity has been weak, both for real demand and for restocking. While some of this downturn can be attributed to the usual seasonal impact of summer holidays, underlying real demand remains subdued even when accounting for seasonality.

Market activity in Europe is expected to remain quiet in the short term as steelmakers perform maintenance. Both producers and service centers are expected to extend their maintenance shutdowns to three or four weeks because of slow end-use demand. Lead times for HR coil are currently four weeks in Italy and six weeks in Germany.

HR coil import offers from Turkey declined w/w due to lower offers from Chinese manufacturers, which put downward pressure on prices. Turkish HR coil imports were reported into southern Europe at $565–575/mt FOB (down $5–10/mt w/w). Although Turkish mills are trying to maintain price levels, they are making weekly concessions due to weak demand.

Meanwhile, the European Commission is set to formally launch an anti-dumping investigation into HR coil imports from Egypt, Japan, India, and Vietnam following a request from Eurofer. This investigation could impact more than half of European HR coil imports. The EU’s introduction of a 15% cap on HR coil volumes from individual countries within the “other countries” quota category in June 2024 already reduced this quota by around 30% in Q3’24. If anti-dumping measures are implemented, it could further tighten supply, supporting European prices.

China

Domestic Chinese sheet prices edged down by RMB10-20/mt w/w given weak demand and deteriorating market confidence amid a summer slowdown. The official manufacturing PMI data remained below the 50 mark in July, coming in at 49.4 and indicating that the domestic manufacturing sector has yet to return to growth territory. Demand remains weak seasonally, and a rise in July’s auto inventory index published by China’s Auto Dealers Association placed further worries on sheet demand. However, domestic sheet production remained elevated despite production halts and maintenance by mills. As such, sheet inventories increased w/w.

Asia

Prices of imported sheet products in Asia remain low due to limited buying interest.

Offers for HR coil SAE1006 grade increased by $10/mt to $520/mt CFR Vietnam for October shipment. However, buyers did not accept this increase, and bids were held at $500/mt CFR Vietnam.

For commercial grade HR coil, offers fluctuated in the range of $490-500/mt CFR Vietnam with very thin buying interest.

Last week, Hoa Phat also announced its new offers for October to domestic customers. The new price was $522-525/mt CFR Vietnam for both SAE1006 and SS400 grades, marking a ~$30/mt fall from its last offers.

CRU assessed HR coil at $510/mt CFR Far East, flat w/w. CR coil and HDG coil prices were both down by $10/mt w/w to $610/mt and $630/mt, respectively.

India

Indian sheet prices fell by INR700–1200/mt ($8–14) w/w as buying activity remained subdued due to low-priced import offers exerting downward pressure on the domestic market. Construction activity weakened further as rains intensified across key demand regions, while manufacturing end users bought material only on an as-needed basis because they had enough inventory at hand. Several buyers also awaited fresh price offers from mills for August output, where they expect some reduction.

For downstream products, drawing grade CR coil commanded a price premium of INR1200–1500/mt ($14–18) over base grade CR coil as suppliers cited better demand for drawing grade material. Meanwhile, Indian sheet export offer prices stayed unchanged amid weak overseas buying interest.

This article was first published by CRU. To learn more about CRU’s services, visit www.crugroup.com.