CRU

July 3, 2024

CRU: Longs pricing trends diverge in North, South America

Written by Alexandra Anderson

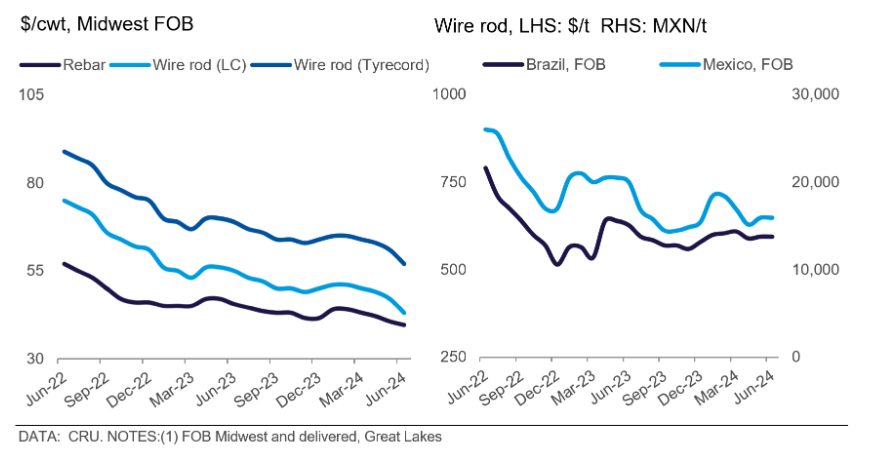

Most longs prices in the US were unchanged this month, except for rebar, which declined by $1.50/cwt ($30/short ton) m/m. While end-use demand is stable, inventories are well-stocked, keeping purchases limited. Domestic availability is sufficient to meet current demand, hindering the appetite for imported material. Meanwhile, prices for scrap remained under pressure in June, with expectations of further decreases in July amid continued weak demand.

Wire rod prices were flat m/m at $43/cwt ($860/st), although prices varied widely depending on volume. Domestic lead times are low, and supply easily meets current demand. Consequently, import licenses fell off in June as buyers are unwilling to wait for material when domestic prices are under pressure and delivery times are short. According to the US Department of Commerce, June import licenses indicated wire rod imports are down roughly 60% m/m from May.

Prices for rebar fell to $38/cwt ($760/st) as demand remained sluggish in June, while merchant bar and structurals were unchanged. Lower scrap prices in June exacerbated the downward pressure and, as with wire rod, supply is readily available, and purchases are in small volumes on an as-needed basis. Rebar imports also fell m/m as buyers can cover their needs from domestic suppliers. June import licenses for rebar were down 50% from May preliminary census data, according to the US Department of Commerce.

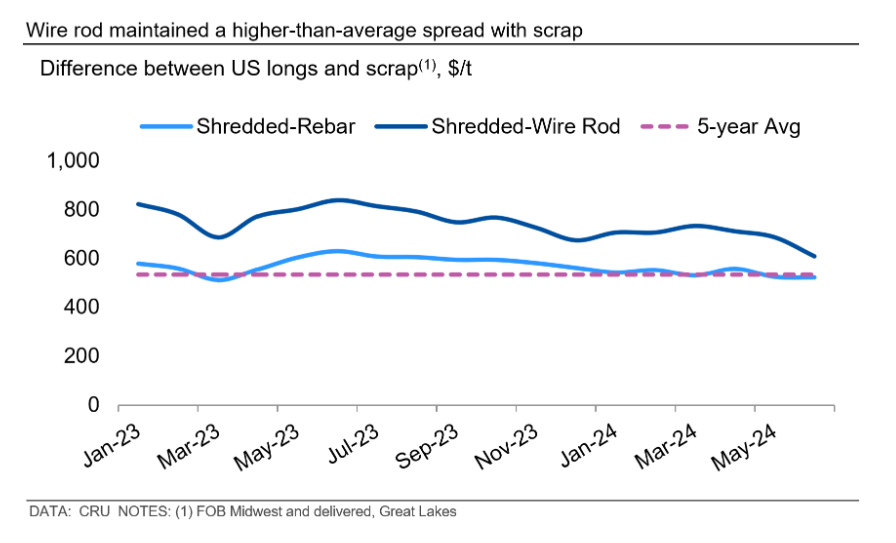

Despite continued decreases in scrap, spreads with long products have remained wide. The June spread with shredded scrap was $608/metric ton and $521/mt for wire rod and rebar, respectively, compared to the historical spread of ~$530/mt between longs and scrap. The US scrap price downtrend continued due to persistent soft demand, although flows into scrap yards slowed in some regions. Mills reportedly had ample inventories, and buy programs were reduced, particularly with scheduled maintenance outages for some buyers. Ultimately, June prices for prime grades fell $20-40/l.ton m/m, depending on the region, while secondary grades were generally down $10-20/l.ton.

The market continues to wait for any tangible impacts from federal infrastructure spending, although some projects have started to break ground. Despite high interest rates, construction spending is still marching forward, with total spending up 8.8% y/y (not seas. adj.), according to the US Census Bureau. Most of that growth has been in the manufacturing and public safety sectors, while commercial project spending has declined 10% y/y.

Brazilian mills announced price increases for all products, including longs, with an increase of 5% in domestic prices starting this month. The main reason behind the increase is the devaluation of the domestic currency against the USD in the last two months, currently around 8.8% lower than what it was in May, as domestic demand continues to be weak while supply remains stable. The new quota system imposed by the government from June only includes wire rods of long products. Domestic production decreased by 5% m/m in May while net imports increased, keeping apparent demand stable.

This article was first published by CRU. To learn more about CRU’s services, visit www.crugroup.com.