Sheet

May 24, 2024

SMU Steel Demand Index falls to a 12-month low

Written by David Schollaert

Steel Market Update’s Steel Demand Index fell five points to a 12-month low and has moved further into contraction territory, according to our latest survey data.

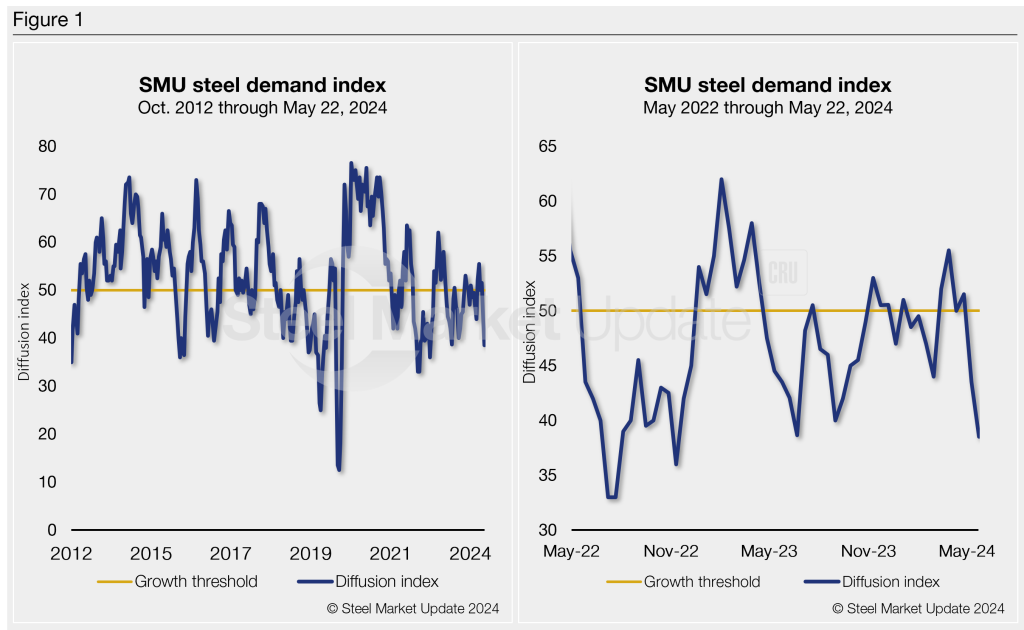

SMU’s Steel Demand Index now stands at 39, down five points from a reading of 44 at the end of April. The decline brought the index to its lowest measure since mid-June 2023.

The reading – down 17 points from a recent high of 56 in March – may indicate that demand is down even as we move past Q2 outages, while prices and lead times are still trending lower.

Methodology

The index, which compares lead times and demand, is a diffusion index derived from the market surveys we conduct every two weeks. This index has historically preceded lead times, which is notable given that lead times are often seen as a leading indicator of steel price moves.

An index score above 50 indicates rising demand and a score below 50 suggests declining demand. Detailed side by side in Figure 1 are both the historical views and the latest Steel Demand Index trend.

State of play

Repeated declines have swung the index to contraction after a brief stint of growth came from early Q2 buying and mill price hikes. The short-lived boost has given way to a bearish undertone with prices and lead time ticking down.

The trend is accentuated by sheet buyers continuing to find mills willing to talk price, and SMU’s Current Buyers’ Sentiment dropping to its lowest mark since August 2020.

Lead times continue to hover around five weeks on average, while hot-rolled (HR) coil slipped to $760 per short ton (st) FOB mill, east of the Rockies. That’s down $35/st week on week and down $85/st from a recent peak of $845/st in early April, according to SMU’s latest check of the market on Tuesday, May 21.

It’s not all bad news. Despite the lower reading, 70% of survey respondents still report stable or improving demand. However, 30% are reporting declining demand, a five-percentage point increase from earlier in the month.

But recall the only time the index has moved into growth territory since late-April 2023 has been for short-lived bumps when the market responded to mill price hikes in last June, late September, November, and mid-March.

Besides short-lived rallies, SMU’s Steel Demand Index has trended downwards and into contraction territory for significant clips over the past year.

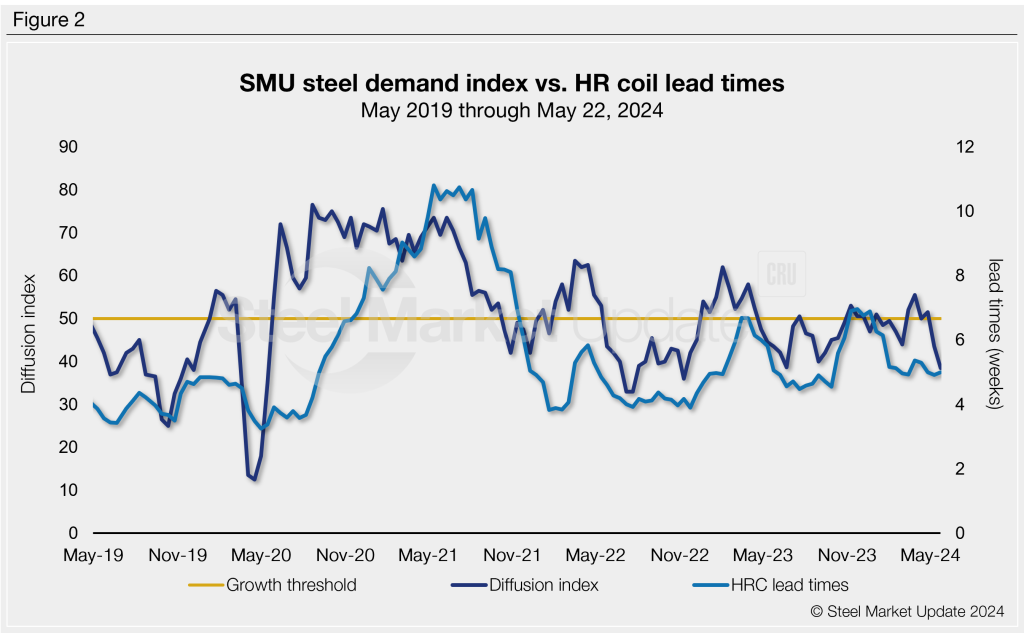

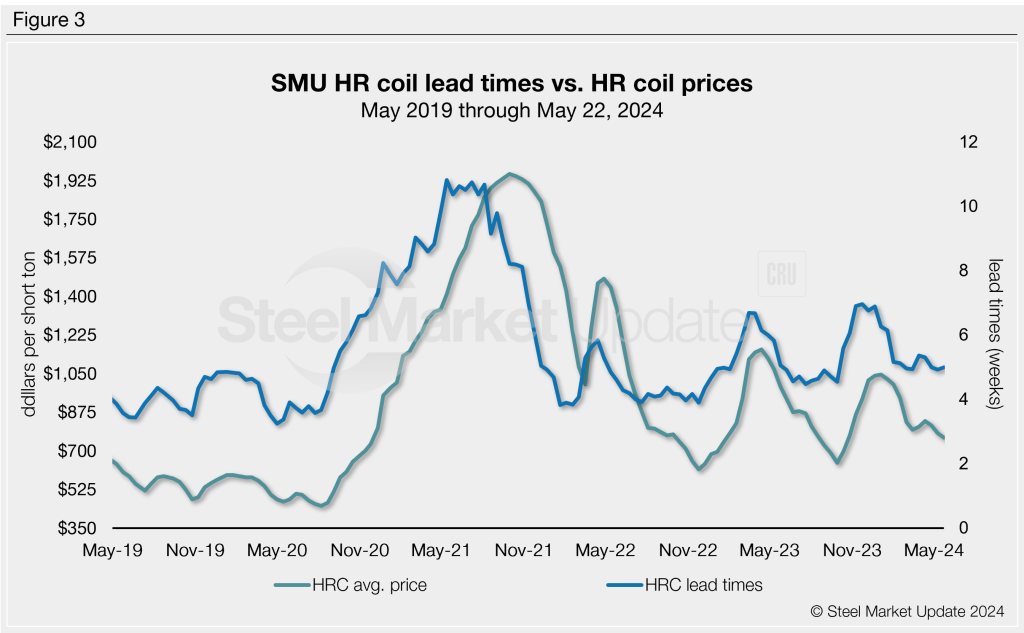

It’s important to note that SMU’s demand diffusion index has, for nearly a decade, preceded moves in steel mill lead times (Figure 2), and SMU’s lead times have also been a leading indicator for flat-rolled steel prices, particularly HRC (Figure 3).

What some SMU survey respondents had to say

“Demand is steady but somewhat down.”

“Summer seems to have started early, still waiting for infrastructure money to trickle down, and uncertainty with the election.”

“Seeing things very soft.”

“Declining transactionally due to pricing pressure.”

“Beginning to decline.”

“High interest rates are slowing our demand.”

“Declining due to falling prices, it’s killing the plate market.”

“Still good on OEM side; slightly offset by spot buyers being cautious and buying small amounts.”

“Near-term spot buying is dead and expect June to be a tough month on contracts with buyers knowing July will be cheaper.”

Note: Demand, lead times, and prices are based on the average data from manufacturers and steel service centers that participate in SMU’s market trends analysis surveys. Our demand and lead times do not predict prices but are leading indicators of overall market dynamics and potential pricing dynamics. Look to your mill rep for actual lead times and prices.