CRU

December 15, 2023

CRU: Ore-based metallics prices follow scrap price upswing

Written by Brett Reed

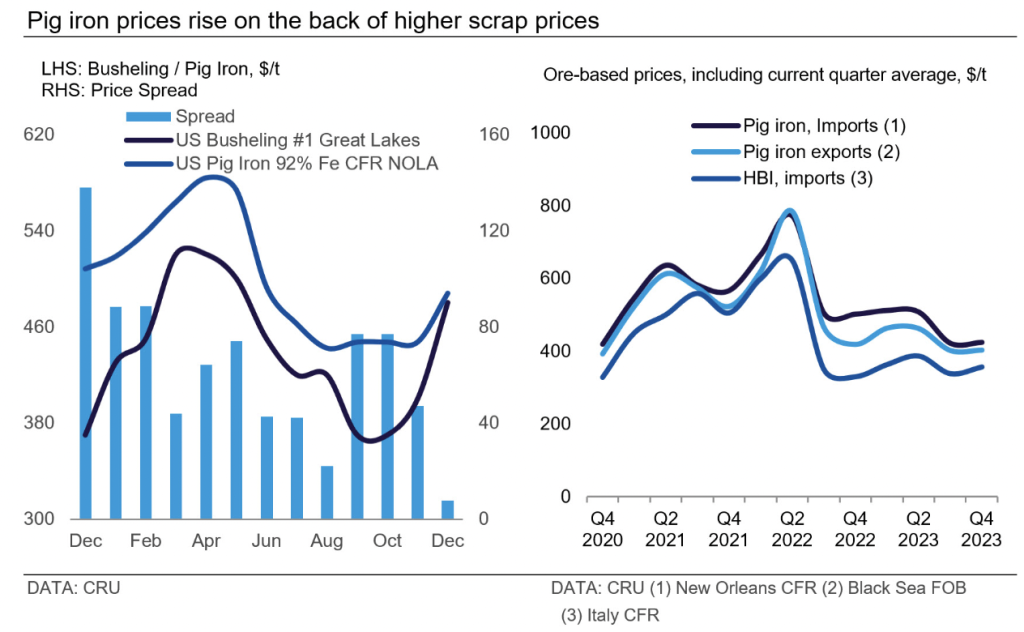

Pig iron prices rose month over month (MoM) for all major regions, driven by rising scrap prices. Supply has tightened in Brazil, extending lead times for US buyers. Additionally, higher domestic consumption in the CIS has restricted availability in Western Europe.

In the CIS, pig iron prices increased $48 per metric ton (t) MoM to $385/t FOB Black Sea. Higher domestic consumption and soft external demand has limited export volumes of Ukrainian material. While risks remain associated with shipping Ukrainian material, there is a potential to use temporary sea corridors. Similarly, Russian exports of merchant pig iron continued to decline in November on softened external demand, resulting in reduced output as demand is primarily driven by domestic consumption.

In Europe, pig iron prices increased $45/t MoM to $425/t CFR Italy on tighter supply. According to market contacts, volumes of Russian material have heavily declined due to elevated demand from Russian buyers and limited supply within the region.

Brazilian pig iron prices increased $30/t MoM in the North and South to $463/t and $435/t FOB, respectively. Despite mills decreasing consumption at the end of this year, export lead times extended.

In the US, pig iron prices increased $40/t MoM to $480/t CFR NOLA on the back of higher scrap prices and tightened supply from Brazil. Market participants note that Brazilian producers are sold out through February shipment, while Ukrainian producers are sold out through January shipment. While US mills have sufficient pig iron inventories at hand, mills are expected to utilize less pig iron in finished steel production due to extended lead times.

Market participants report that buyers are looking to secure Ukrainian material in light of tightened supply in Brazil. However, there remains logistical risks associated with securing Ukrainian material. Though pig iron prices have converged with prime, market participants do not expect it to last, anticipating further price increases into 2024.

This article was first published by CRU. Learn more about CRU’s services at www.crugroup.com.