Market Data

July 20, 2023

Mills More Willing to Negotiate Lower Sheet Prices: SMU Survey

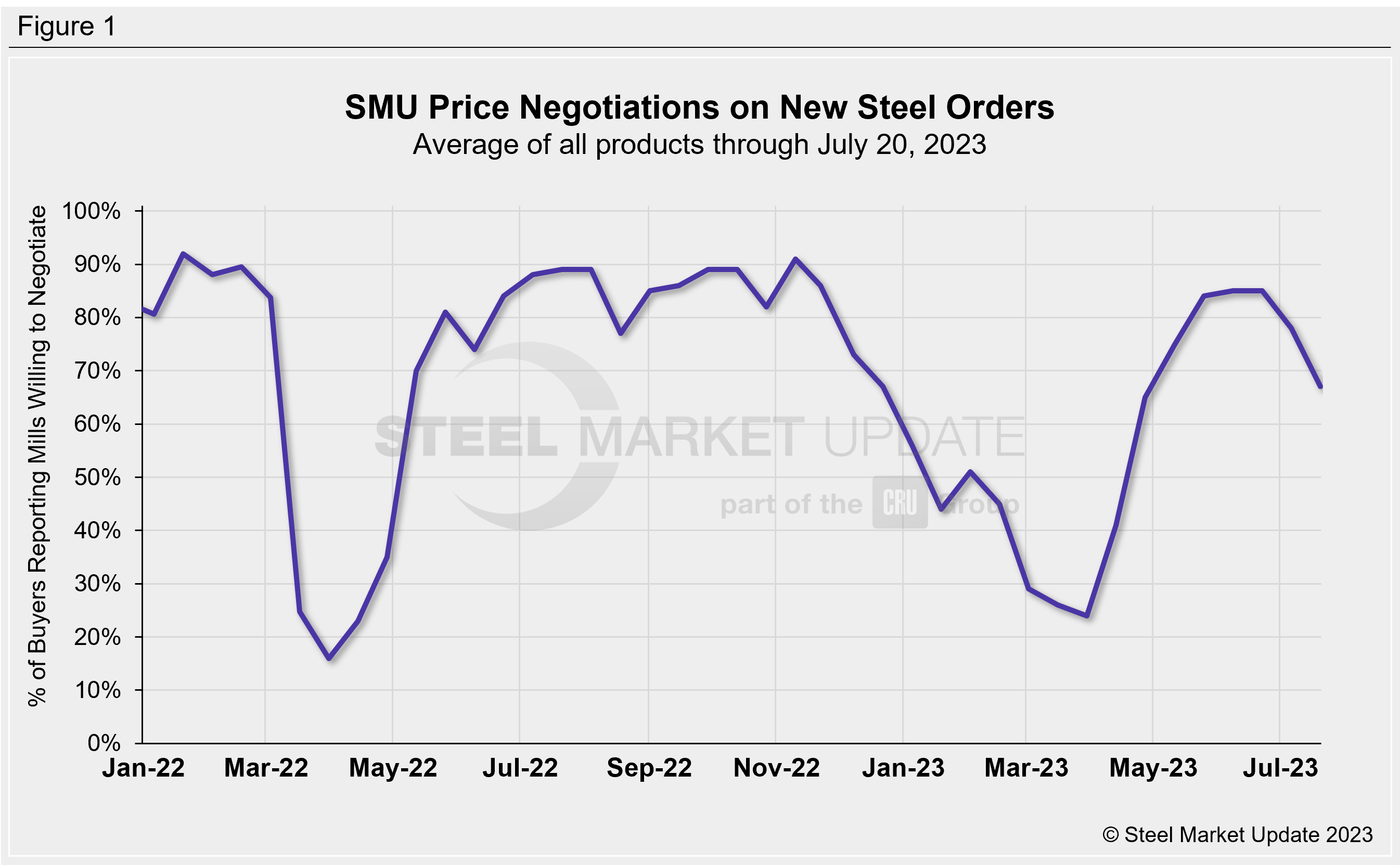

Steel buyers report that mills are willing to negotiate lower spot prices for the sheet products SMU surveys. It’s a different story in plate, where buyers find mills less willing to negotiate lower, according to SMU’s most recent survey data.

The percentage of respondents saying steel mills were willing to talk price on plate stood at 29% this week, off from 63% two weeks ago. Galvanized, in contrast, increased six percentage points to 90% in the same comparison.

Every two weeks, SMU asks steel buyers whether domestic mills are willing to negotiate lower spot pricing on new orders. This week, (Figure 1) 67% of participants surveyed by SMU reported mills were willing to talk price on new orders, down nine percentage points from two weeks earlier – largely because of producers being less willing to drop plate prices.

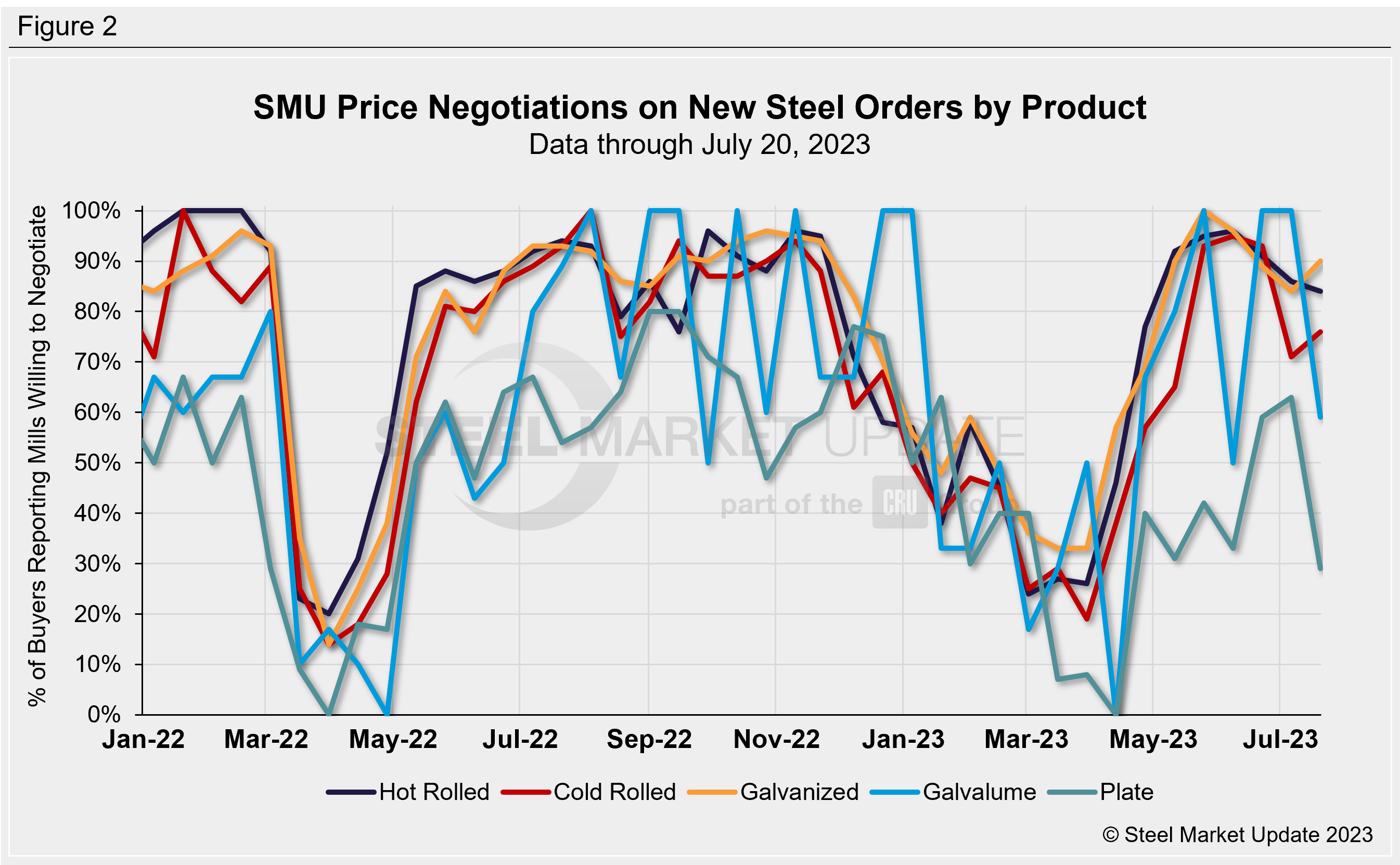

Figure 2 below shows negotiation rates by product. Hot rolled slipped two percentage points to 84% of buyers reporting mills more willing to negotiate price vs. two weeks earlier, while Galvalume dropped 41 percentage points to 59% in the same comparison. Recall that Galvalume can be more volatile because we have fewer survey participants there. Cold rolled has increased since the last market check, rising five percentage points to 76% of respondents saying mills were willing to talk price.

What SMU Survey Respondents Had to Say:

“We will have challenges but will do OK.”

“Cheap imports from Asia are flooding in.”

“Market is tough, but we will continue to make money.”

“Demand is better than the past two months with contract prices decent, and some restocking happening, along with auto doing well.”

“Climate is slightly better for us.”

Note: SMU surveys active steel buyers every other week to gauge the willingness of their steel suppliers to negotiate pricing. The results reflect current steel demand and changing spot pricing trends. SMU provides our members with a number of ways to interact with current and historical data. To see an interactive history of our Steel Mill Negotiations data, visit our website here.

By Ethan Bernard, ethan@steelmarketupdate.com