Community Events

March 22, 2023

HRC, Prime Scrap Price Spread Widens Further in March

The spread between hot-rolled coil (HRC) and prime scrap prices has widened significantly in March as both products saw large price gains, according to Steel Market Update data.

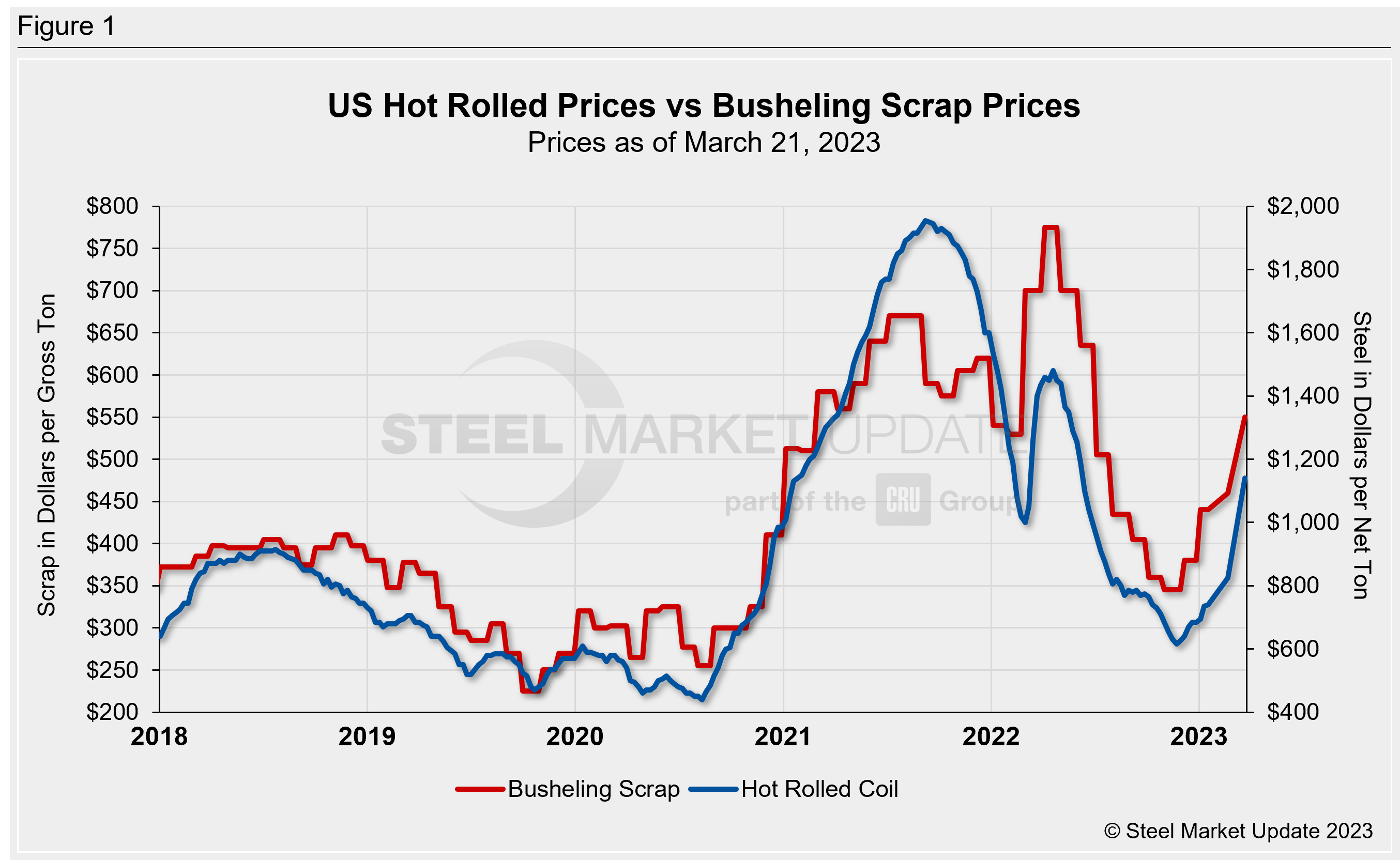

With a flurry of recent price increases, our hot-rolled coil price average jumped $25 per ton week over week to $1,140 per ton ($57 per cwt) as of March 21.

March scrap prices settled late last week, with busheling prices rising $90 per gross ton to $550 per ton from February. Figure 1 shows price histories for each product.

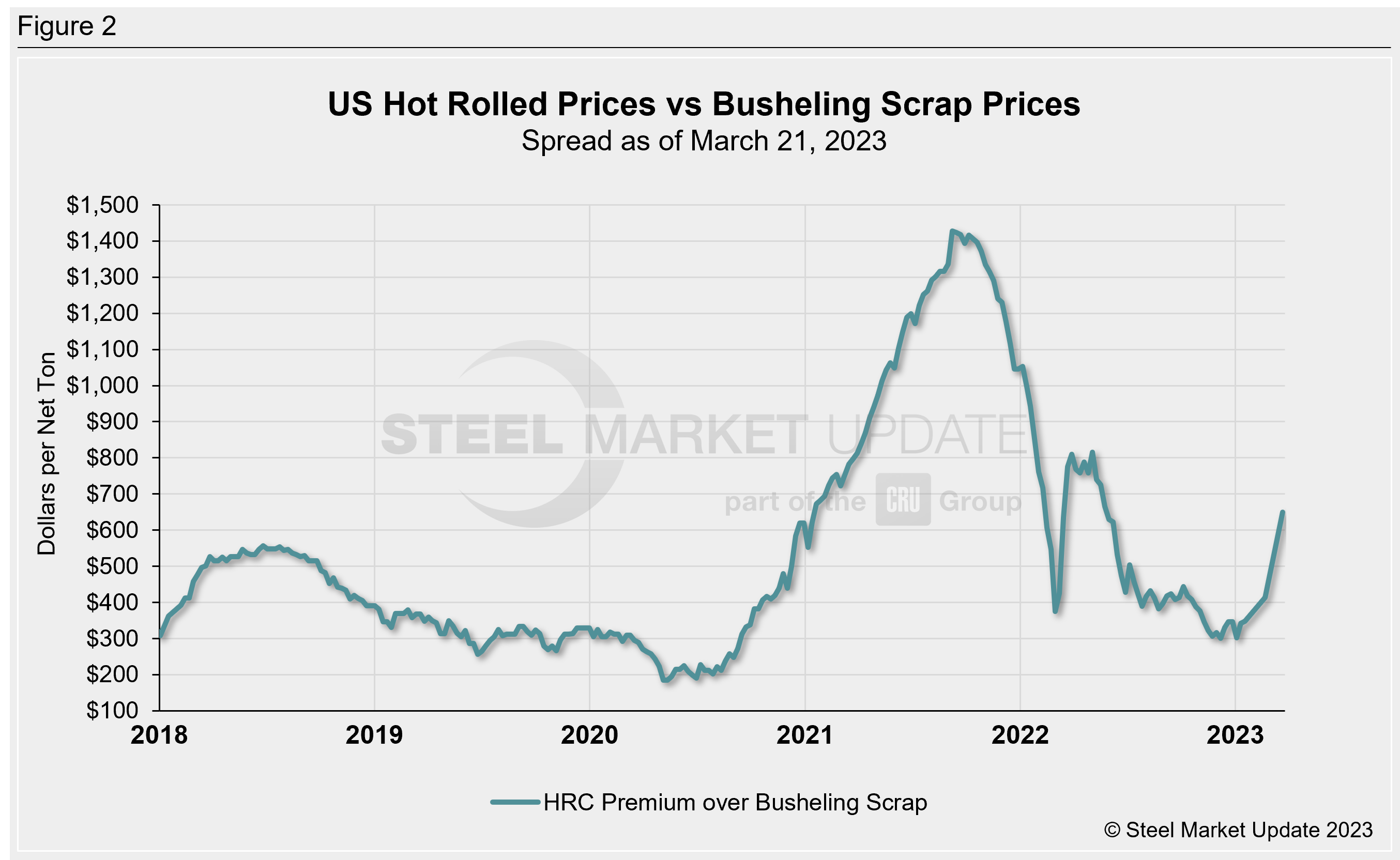

After converting scrap prices to dollars per net ton for an equal comparison, the differential between HRC and busheling scrap prices is $649 per net ton through March 21, up $235 from $414 last month (Figure 2). This represents the widest spread since late-May 2022.

PSA: Did you know our Interactive Pricing Tool has the capability to show steel and scrap prices in dollars per net ton, dollars per metric ton, and dollars per gross ton?

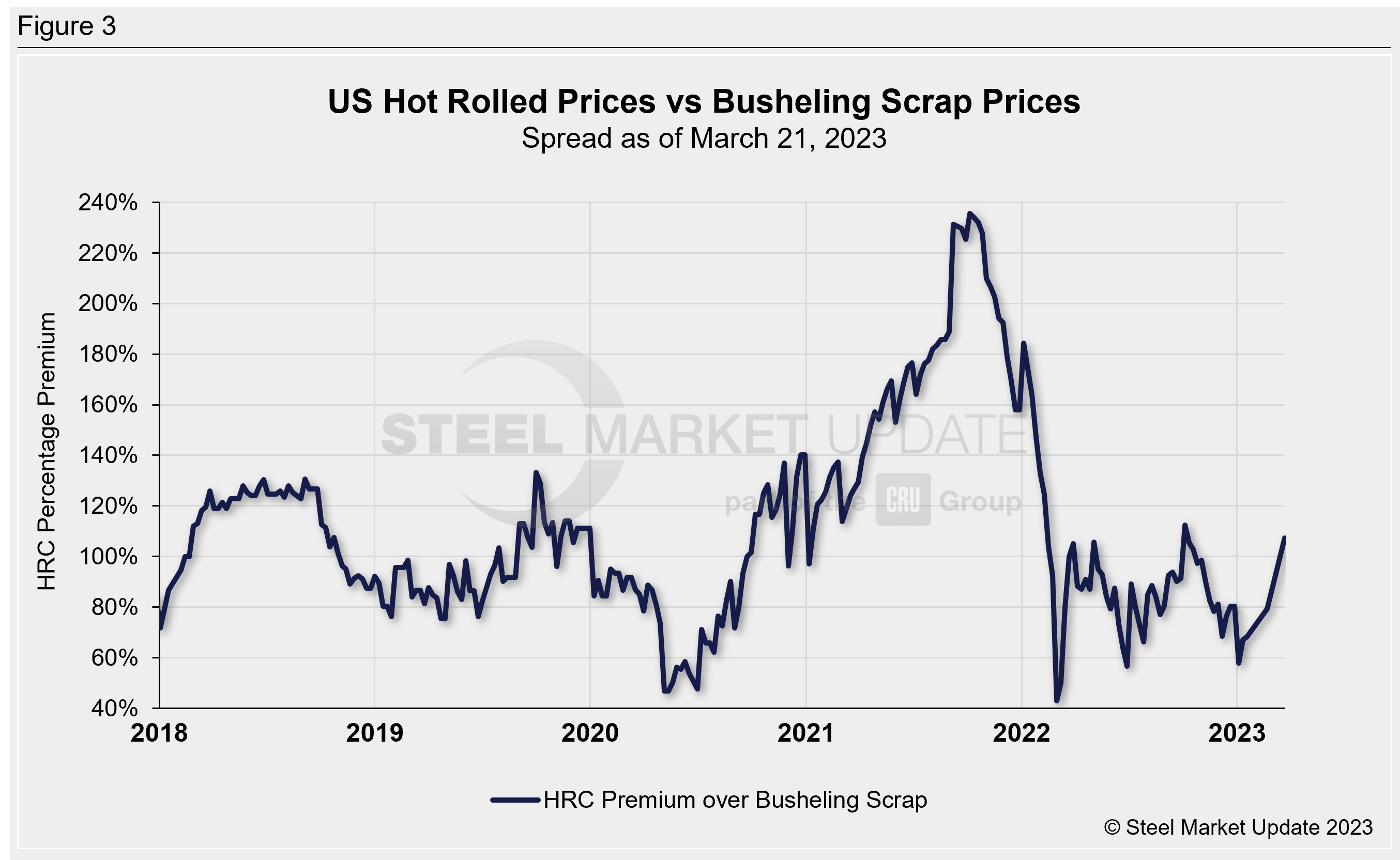

Figure 3 explores this relationship in a different way – we have graphed the spread between HRC and busheling scrap prices as a percentage premium over scrap prices. HRC prices now carry a 107% premium over prime scrap, increasing from 79% a month earlier, and the first time the premium has topped 100% since October of last year.

This comparison was inspired by reader suggestions. If you would like to chime in with topics you want us to explore, reach out to our team at news@steelmarketupdate.com.

By Ethan Bernard, ethan@steelmarketupdate.com