Market Data

August 19, 2022

SMU Steel Buyers Sentiment Index Slips After Previous Jump

Written by Brett Linton

Steel Market Update’s Steel Buyers Sentiment Index eased from it’s early-August blip, as did our Future Steel Buyers Sentiment Index. The latest Sentiment Index is tied with the early-June reading for the third lowest level recorded this year. Future Sentiment is now at the fourth lowest level of the year. Recall that one month ago, both Sentiment Indices saw double-digit declines, then quickly recovered in early-August.

SMU surveys steel buyers every other week, asking how they view their chances of success in the market today, and also a few months down the road. SMU’s Buyers Sentiment Index registered +60 this week, down six points from two weeks prior, but up 17 points from one month ago (Figure 1). In mid-July, Sentiment declined by 17 points to +43, the lowest level seen since August 2020. Sentiment then recovered 23 points in early August. Our Buyers Sentiment Index peaked at +82 in March of this year.

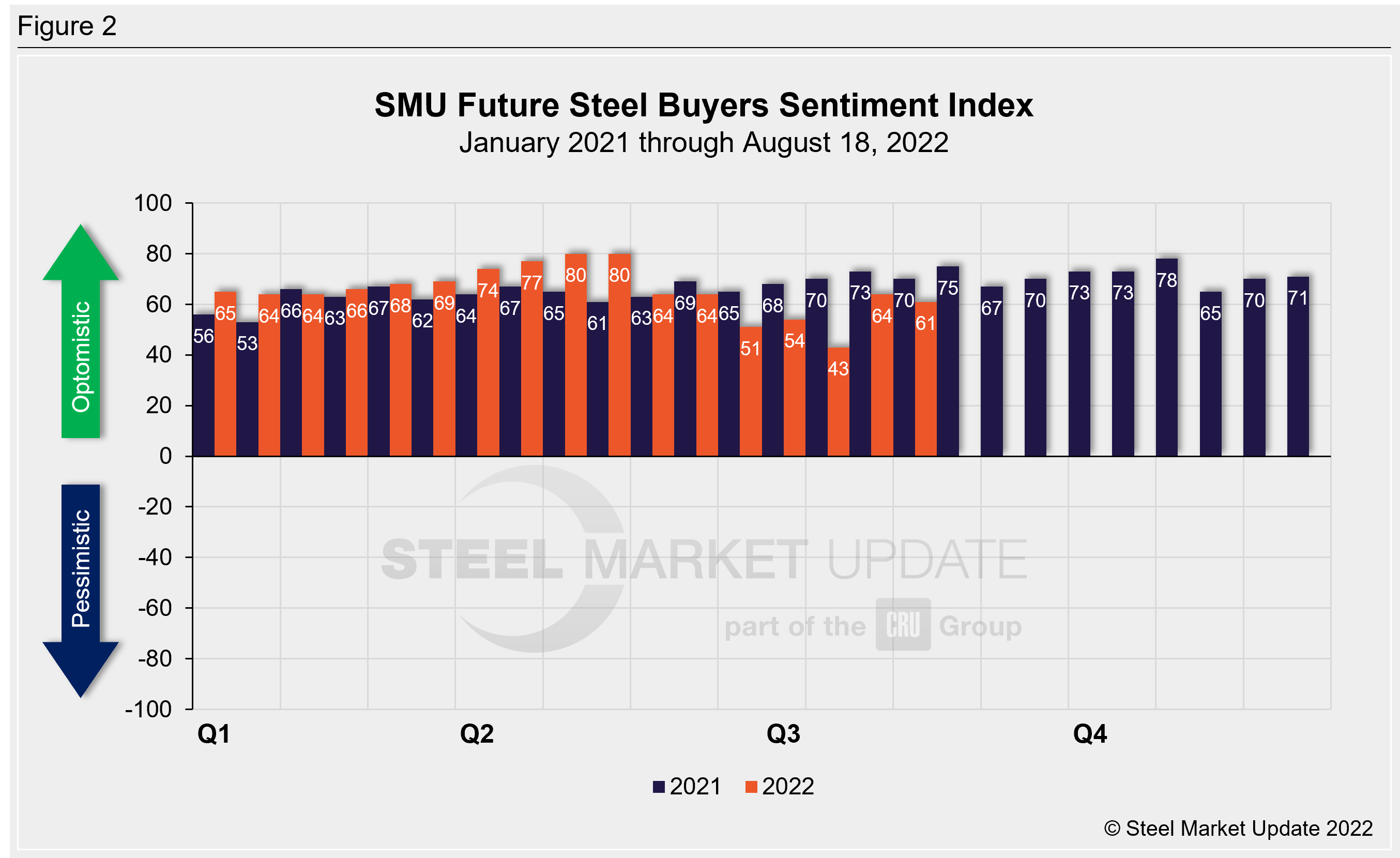

SMU’s Future Buyers Sentiment Index, which measures buyers’ feelings about business conditions three to six months in the future, declined three points from our previous survey and now stands at +61 (Figure 2). In mid-July, our Future Sentiment Index had fallen to near a two-year low at +43. In early-August, Future Sentiment rebounded 21 points to +64. Earlier this year we saw the highest Future Sentiment readings recorded in our 13.5-year history: late April and early May both registered +80.

Recall that as steel prices peaked last September, Current Sentiment reached an all-time high of +84, while Future Sentiment peaked two months later at +78. The lowest levels over the past decade both occurred in April 2020, at -8 and +10 respectively.

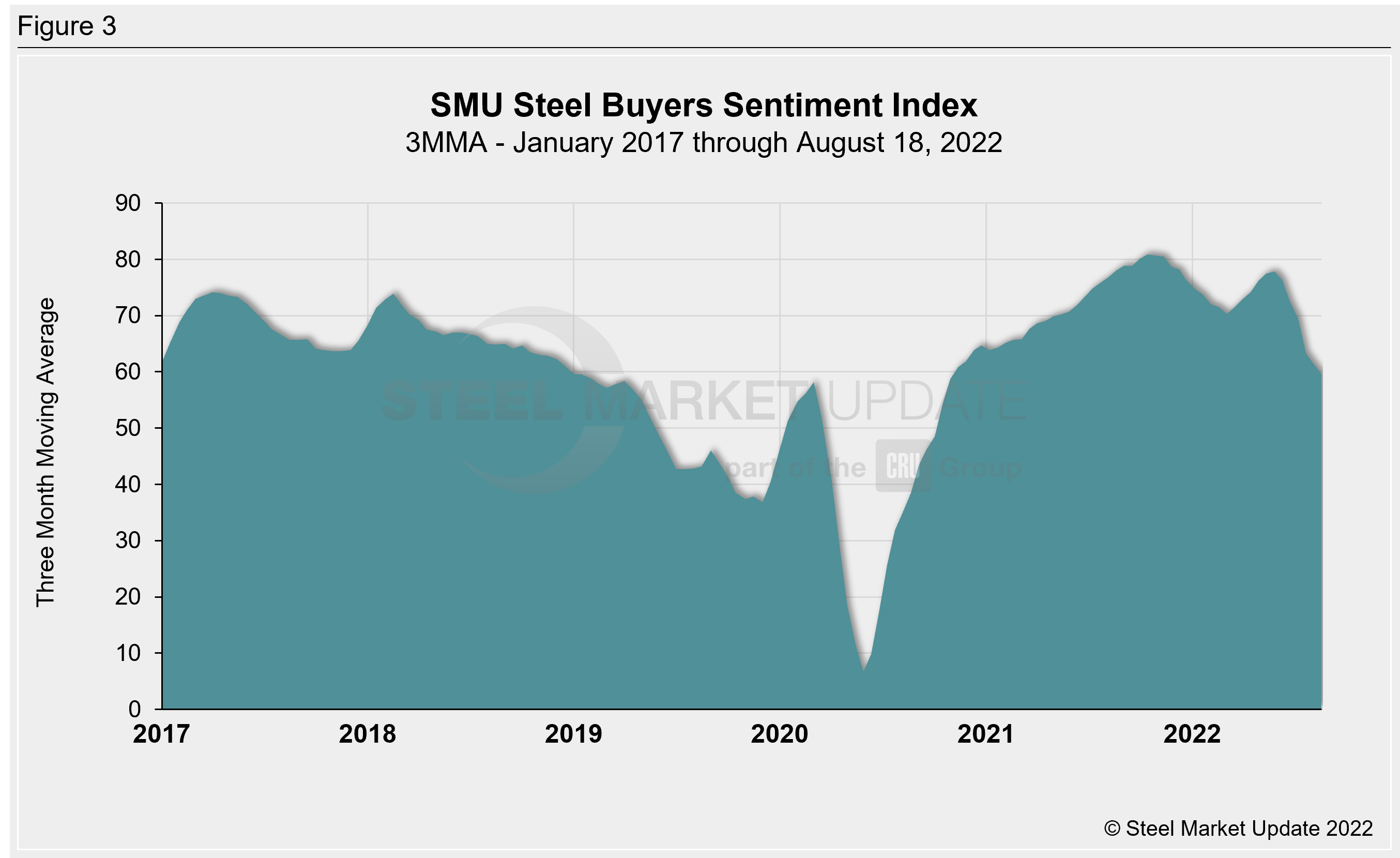

Measured as a three-month moving average, the Current Sentiment 3MMA decreased two points to +59.67 last week, a four-point decline compared to one month earlier (Figure 3). This is the lowest reading since October 2020 when it was +58.67. Three months ago, the Current Sentiment 3MMA peaked at +77.83, the highest level since December 2021.

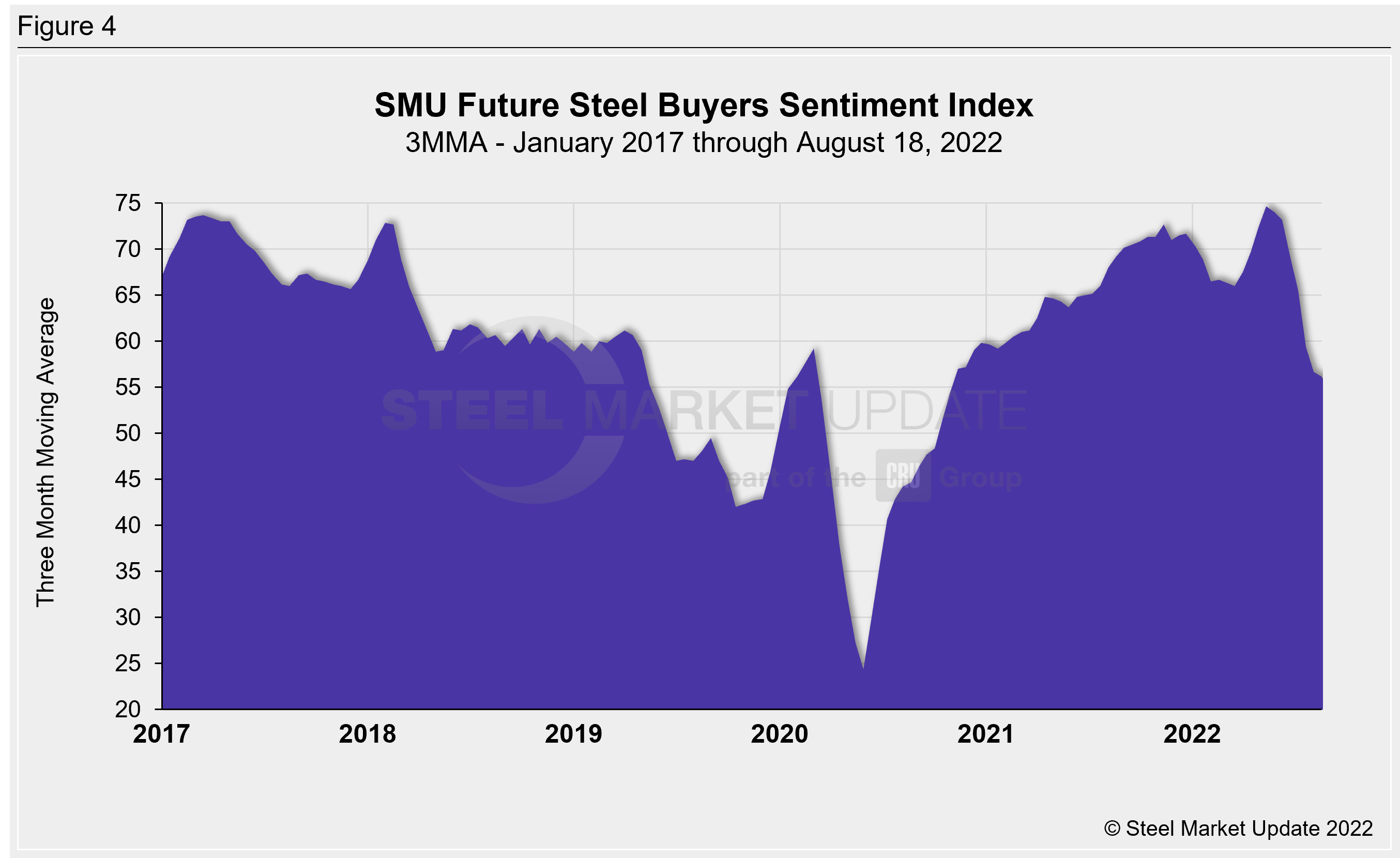

The Future Sentiment 3MMA declined half a point this week to +56.17, down three points from one month prior (Figure 4). This is also the lowest reading seen since October 2020 when it was +54.50. Three months ago, the Future Sentiment 3MMA reached a record high of +74.67, surpassing the previous record of +73.67 in March 2017.

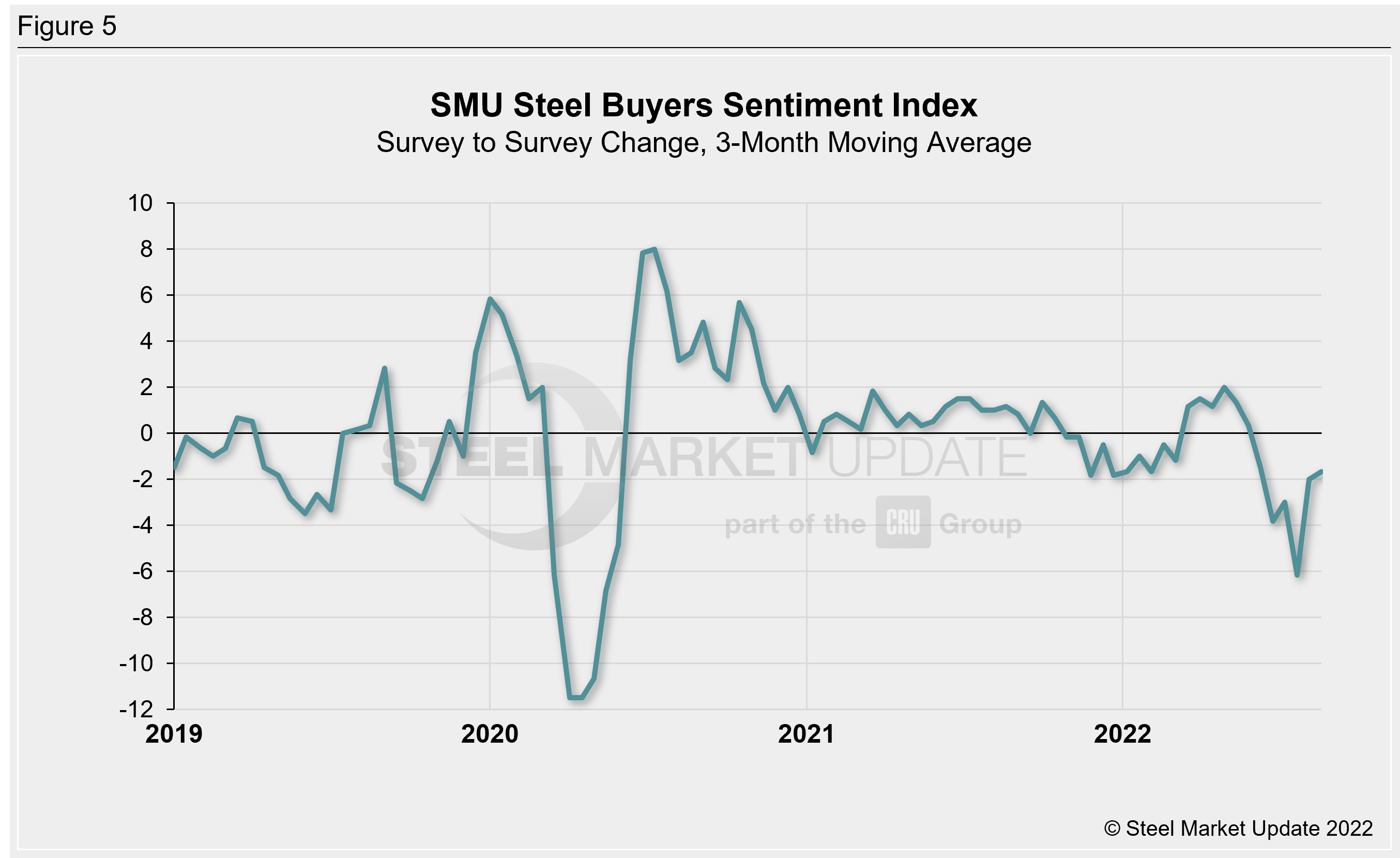

One helpful way to measure changes in Sentiment is to graph the survey-to-survey change in the Current Sentiment Index to measure the severity of Sentiment movements (Figure 5). On a 3MMA basis, the survey-to-survey change through last week is down two points compared to early-August. One month ago, we saw a six-point decline, which was the largest change seen since April 2020. Between November 2020 and June 2022, the survey-to-survey change in our 3MMA Sentiment readings was steady, never exceeding two points. In late June of this year, it began to exceed that range and did so through July.

What SMU Survey Respondents Had to Say

“Demand remains better than trade press articles suggest.”

“I am concerned about lack of real demand going forward. And added domestic capacity could oversupply the market.”

“Good—As long as pricing does not start trending down.”

“Inflation, high interest rates, falling prices and the threat of a recession have spooked the market and capital investments.”

“Prices will stabilize and demand will return.”

“Spot market demand will slow down by the end of September.”

“Future direction is unclear.”

“Whilst my margins have taken a hit, the order book is still strong and I’m making money.”

“Thinking about the beginning of 2023, we should be successful.”

“I am expecting H2 to be quite an uphill battle. Costs are just waaaayyy too high, both on inventory and general variable costs.”

About the SMU Steel Buyers Sentiment Index

SMU Steel Buyers Sentiment Index is a measurement of the current attitude of buyers and sellers of flat-rolled steel products in North America regarding how they feel about their company’s opportunity for success in today’s market. It is a proprietary product developed by Steel Market Update for the North American steel industry. Tracking steel buyers’ sentiment is helpful in predicting their future behavior.

Positive readings run from +10 to +100. A positive reading means the meter on the right-hand side of our home page will fall in the green area indicating optimistic sentiment. Negative readings run from -10 to -100. They result in the meter on our homepage trending into the red, indicating pessimistic sentiment. A reading of “0” (+/- 10) indicates a neutral sentiment (or slightly optimistic or pessimistic), which is most likely an indicator of a shift occurring in the marketplace. Sentiment is measured via Steel Market Update surveys that are conducted twice per month. We display the meter on our home page.

We send invitations to participate in our survey to more than 700 North American companies. Approximately 45% of respondents are service centers/distributors, 30% are manufacturers, and the remainder are steel mills, trading companies or toll processors involved in the steel business.

Click here to view an interactive graphic of the SMU Steel Buyers Sentiment Index or the SMU Future Steel Buyers Sentiment Index.

By Brett Linton, Brett@SteelMarketUpdate.com