Market Data

August 4, 2022

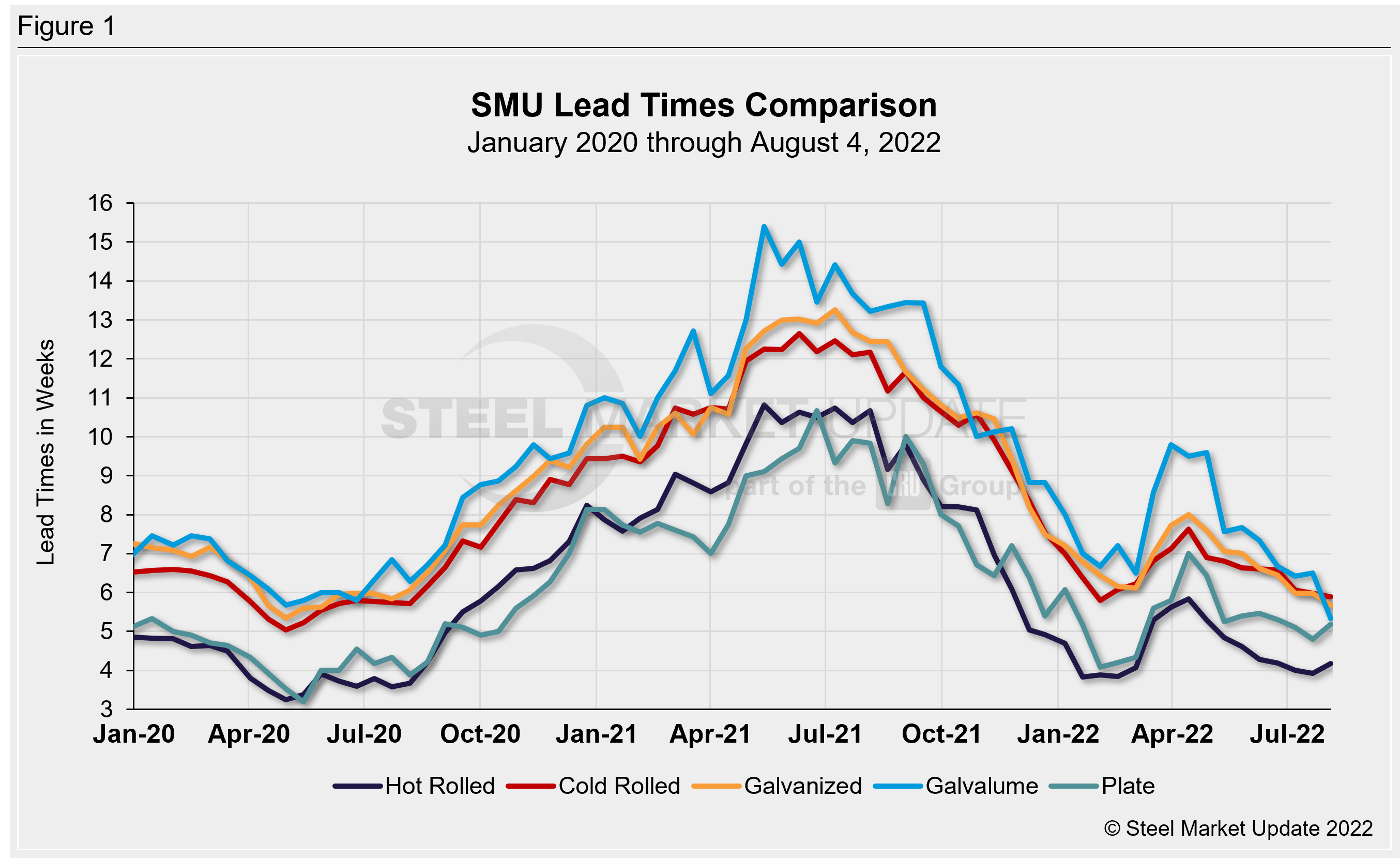

Slight Blip in Steel Mill Lead Times

Written by Brett Linton

Steel mill lead times were mixed this week, with some products slightly up and others down, according to SMU’s latest market check. Hot rolled and plate lead times rose compared to what we saw two weeks ago, while cold rolled and coated lead times inched further downward. Is this just a blip or the start of a new trend?

On average this week, lead times declined by 0.2 weeks across the board compared to mid-July and are down an average of 0.3 weeks compared to one month ago. Having gradually declined from the April peak, July lead times generally remain in line with early 2022 levels.

Buyers surveyed this week reported mill lead times ranging from 3–6 weeks for hot rolled, 4–8 weeks for cold rolled, and 4–7 weeks for galvanized, Galvalume, and plate.

SMU’s hot rolled lead times rose 0.3 weeks compared to two weeks ago, now averaging 4.2 weeks. HR lead times are up 0.2 weeks compared to one month prior, down from a peak of 5.8 weeks in April. The lowest hot rolled level this year was 3.8 weeks seen in January and in February. The record low in our ~11-year data history was 2.8 weeks in October 2016.

Cold rolled lead times declined 0.1 weeks to 5.9 weeks, now the lowest level seen since early February. Galvanized lead times eased 0.3 weeks compared to mid-July to 5.7 weeks (they were as low as 6.1 weeks back in March, and our record low was 4.8 weeks in February 2015). The average Galvalume lead time dropped considerably, down 1.2 weeks from mid-July to 5.3 weeks. Note that Galvalume figures can be more volatile due to the limited size of that market and our smaller sample size. One month ago Galvalume lead times were 6.4 weeks.

Mill lead times for plate rose by 0.4 weeks to 5.2 weeks, up 0.1 weeks from one month ago. Recall that in mid-July, plate lead times fell to 4.8 weeks, the first time seeing a sub-5 week figure since early March. The lowest plate lead time this year was 4.1 weeks in early February. In our four-year history of plate lead times, the lowest figure we have recorded was 3.2 weeks in May 2020.

Approximately 61% of the executives responding to this week’s questionnaire told SMU they were seeing stable lead times, up from 55% in our previous survey. 36% said lead times were slipping, down from 45% in mid-July. Less than 5% of buyers reported lead times as extending. Here is what a few of our respondents had to say:

“I think we are at the bottom of lead time compression.”

“Lead times are at levels as low as they might be comfortable for mills. They will take out capacity if they shorten much more.”

“Only stable because lead times can’t get much shorter.”

“They will continue to slip as the mills battle each other to go lower.”

“Hopeful mills will adjust output to match current demand.”

“Mill outages on the horizon.”

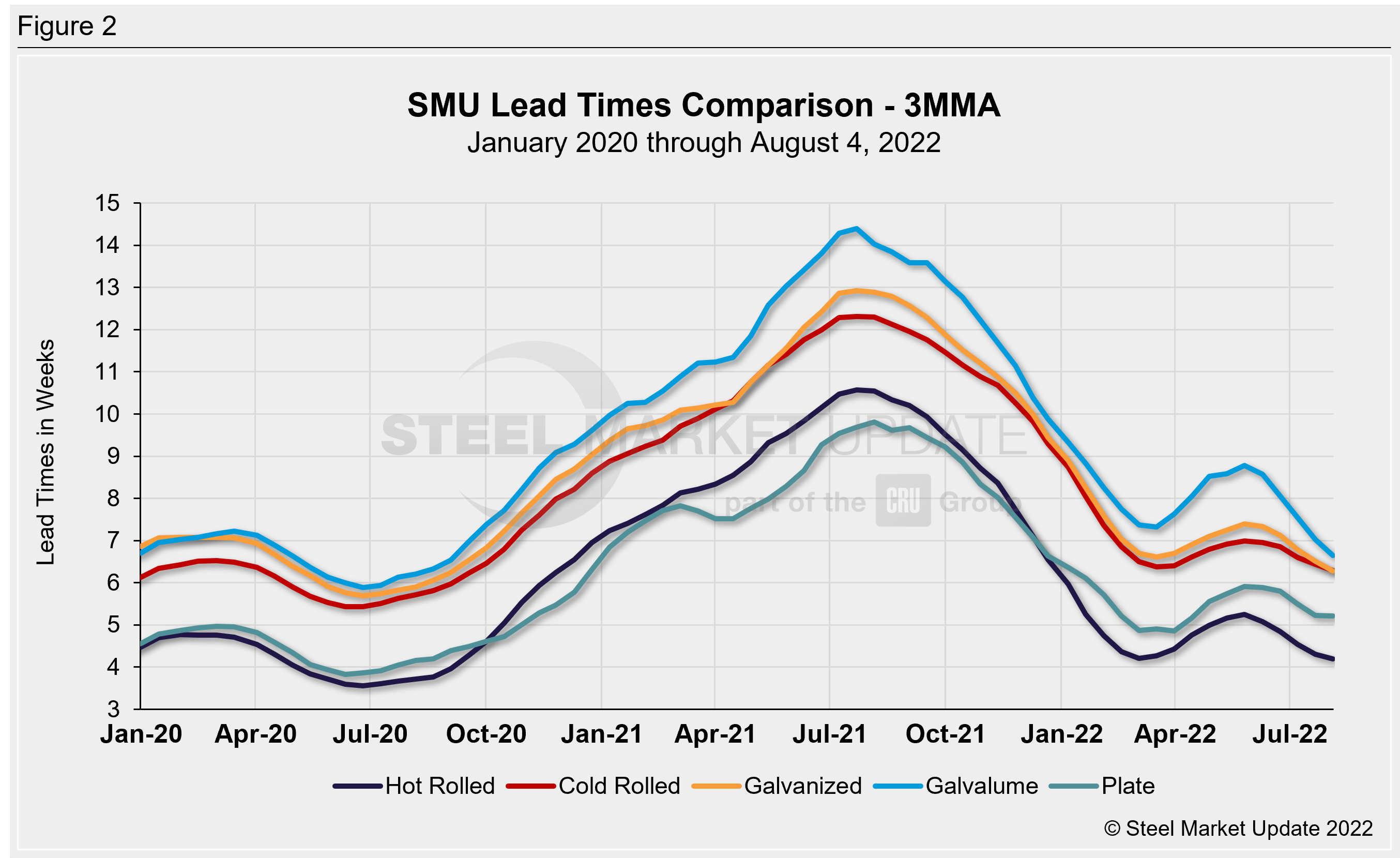

Looking at lead times on a three-month moving average can smooth out the variability in the biweekly readings. As a 3MMA, all products were flat to down 0.3 weeks compared to two weeks prior and down as much as 0.8 weeks compared to early July. The current 3MMA for hot rolled is down 0.1 weeks to 4.2 weeks, cold rolled eased 0.1 weeks to 6.3 weeks, galvanized is down 0.2 weeks to 6.3 weeks, Galvalume declined 0.3 weeks to 6.7 weeks, and plate was flat at 5.2 weeks.

Note: These lead times are based on the average from manufacturers and steel service centers who participated in this week’s SMU market trends analysis. SMU measures lead times as the time it takes from when an order is placed with the mill to when the order is processed and ready for shipping, not including delivery time to the buyer. Our lead times do not predict what any individual may get from any specific mill supplier. Look to your mill rep for actual lead times. To see an interactive history of our Steel Mill Lead Times data, visit our website here.

By Brett Linton, Brett@SteelMarketUpdate.com