Market Data

April 28, 2022

Steel Mills More Willing to Negotiate Lower Prices on New Orders

Written by Brett Linton

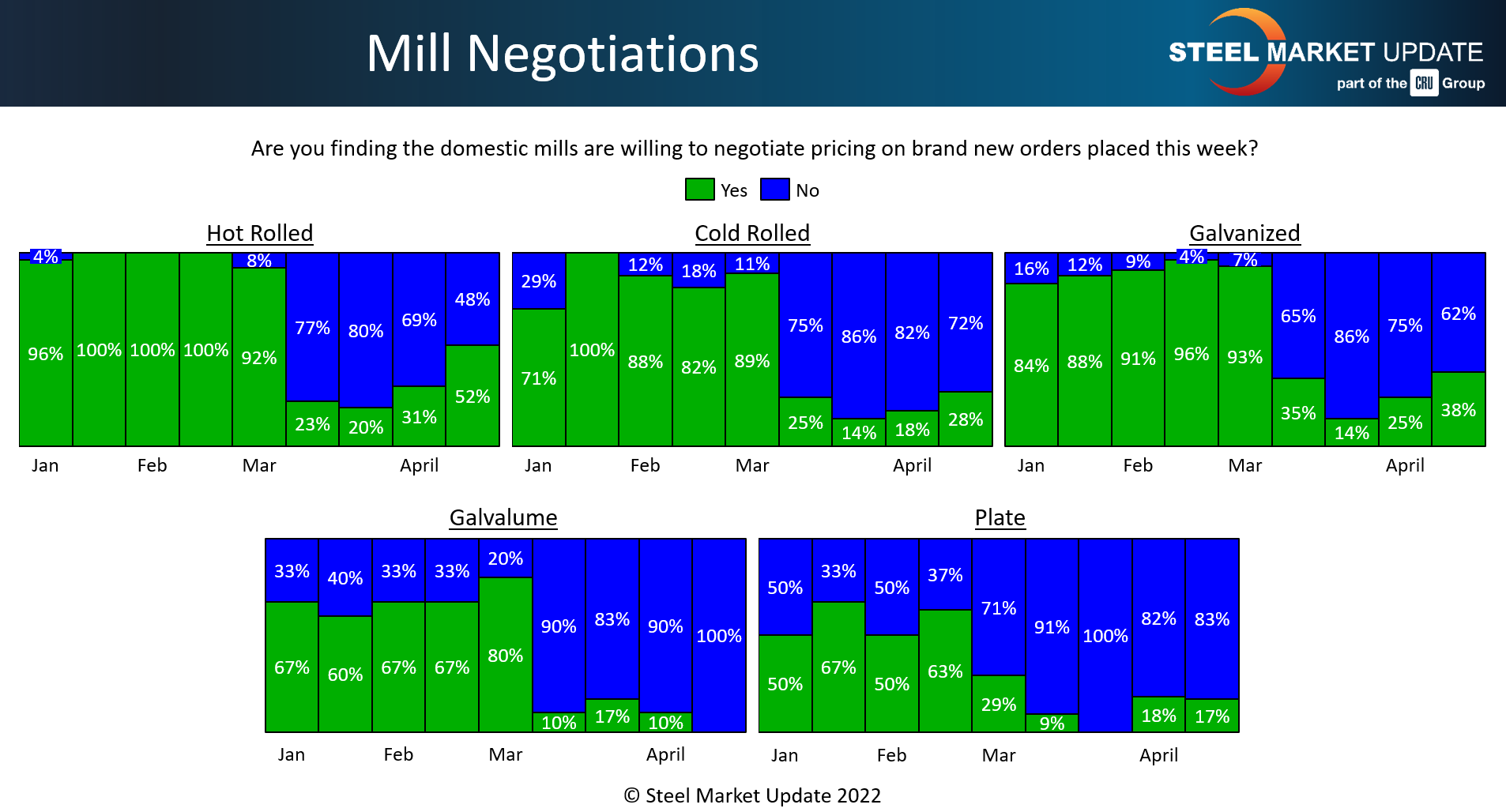

Steel mills appear to be loosening their firm grip on price negotiations, according to buyers polled in our latest steel market survey. Over half of hot rolled steel buyers now report that mills are willing to talk price to secure an order.

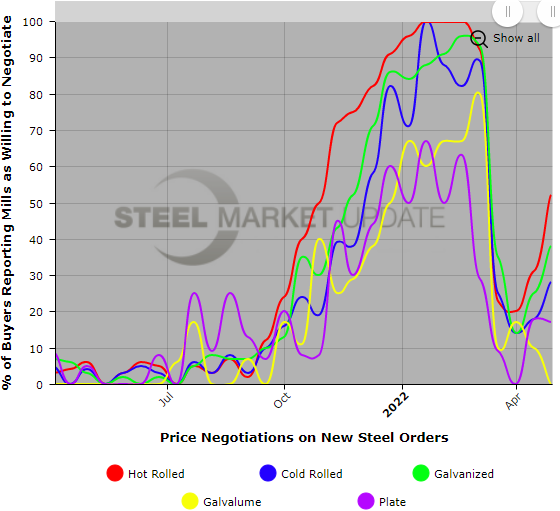

Every two weeks, SMU asks respondents: Are you finding domestic mills willing to negotiate spot pricing on new orders placed this week? On average this week, 65% steel buyers reported that mills are not willing to negotiate lower prices on new orders. While somewhat high, this rate has declined in each of our market checks over the past month. As we saw in mid-April, multiple buyers commented that they expect mills to begin to budge more on price to secure new orders in coming weeks.

52% of hot rolled buyers surveyed responded that mills were willing to negotiate on new order price, up from a rate of 31% two weeks prior. In the cold rolled and galvanized segments, roughly one third of buyers report that mills are now negotiable, both up compared to weeks prior. Negotiations on Galvalume products appear to be null, but due to the more limited size of that market and our small sample size, this figure can be more volatile.

Negotiations were never quite as loose in the plate market and have been tightening since early March. Our latest survey shows that 83% of plate buyers reported mills are not willing to bargain, unchanged versus two weeks ago.

SMU’s Price Momentum Indicator remains at Neutral, indicating prices may be in transition over the next 30-60 days. We will keep our Momentum Indicator at Neutral until the market establishes a clear trajectory.

Note: SMU surveys active steel buyers twice each month to gauge the willingness of their steel suppliers to negotiate pricing. The results reflect current steel demand and changing spot pricing trends. SMU provides our members with a number of ways to interact with current and historical data. To see an interactive history of our Steel Mill Negotiations data, visit our website here.

By Brett Linton, Brett@SteelMarketUpdate.com