Overseas

January 28, 2022

CRU: U.S. Sheet Prices Plummet Back Towards Global Average

Written by Ryan McKinley

By CRU Senior Analyst Ryan McKinley, from CRU’s Steel Sheet Products Monitor, Jan. 26

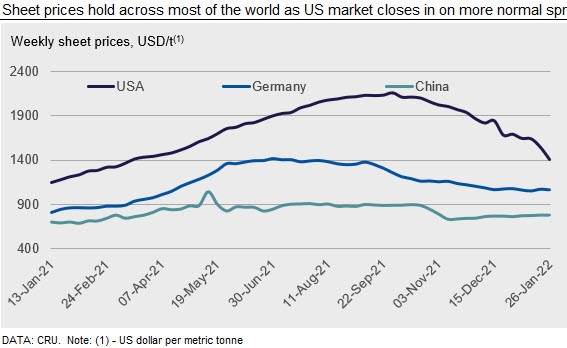

Steel sheet prices in the U.S. sank by about 9% w/w as they continued to fall towards the global average. CRU’s weekly HR coil assessment in the U.S. was $126 /s.ton lower than the prior week, and high inventory levels relative to demand will keep downside pressure on prices for the near term. Meanwhile, mills in Europe had mixed availability, which kept prices stable in southern Europe relative to the north. Prices were also largely stable across Asia as trading activity was subdued ahead of Lunar New Year celebrations, although we do expect to see an uptick in prices for some markets after the holiday ends as costs for zinc and coking coal spike.

USA

Steel sheet prices in the U.S. continued to fall this week, with HR coil down by $126 /s.ton w/w. We have seen a wider-than-normal price differential between HDG coil using HR substrate versus CR substrate. While CR coil prices have been falling, it has been at a slower pace than HR coil or HDG coil. In fact, there have been multiple instances of HDG CR-based coils selling at lower price levels than CR coils. We attribute a portion of this divergence to market share and mill margins. HDG coil accounts for 35% of sheet products as opposed to a 20% market share for CR coil. As steel buyers have become more aggressive in their negotiations, pricing in the larger market was impacted first. Mills have also been more willing to negotiate on HDG coil, even using CR as the substrate, because it is cheaper and faster to convert CR full hard coils to HDG coils than to fully processed CR coils. Many steel buyers expressed that inventory levels were too high when compared with demand, but felt that by 2022 Q2 the situation would be rectified. Until then they plan to cut back on new purchases as much as possible, instead utilizing their inventory in the most efficient manner they can.

On the U.S. West Coast, sheet steel prices fell this week as mills began soliciting March orders. HR coil prices decreased by $200 /s.ton m/m, while CR coil and HDG coil prices fell by less. Buyers felt the price decreases were established to compete with lower prices in other regions of the country and import offers. There has been a slight downward adjustment in Q1 2022 demand forecasts, but overall sentiment has yet to turn bearish for end-use demand. While inventories are somewhat heavier than normal, they appear to be more balanced than in the Midwest or South.

Europe

European sheet price directions were again mixed in our latest assessment. European HR coil prices increased by €1-5 /t w/w, while CR coil and HDG fell by €1-13 /t w/w, with most of the downward movements occurring in northern Europe. In our latest assessment, German and Italian HR coil were assessed at €938 /t and €849 /t, respectively.

Some mills are more booked up than others, and we have heard that one large European producer has relatively empty order books and is approaching customers with attempts to sell double the amount of volume as normal. Other European mills do not have as much availability. Market participants report that automotive sheet buyers settled their 2022 contracts at €520-570 /t higher y/y for HR coil & HDG. Settlements were heard to be above the spot market, though may reflect the real value that exists in securing long term supply from a domestic mill at a time when freight costs and the risk of logistics and production interruptions have been high.

China

Chinese domestic sheet prices were little changed amid a quieter market than a week ago. Limited transactions were recorded this week and offers also significantly reduced as many traders left the market to observe the Lunar New year holiday. In response, subdued purchases lead to an increase of 1.6% w/w for sheet inventories at major warehouses and mills. However, sentiment turned bullish as the central bank cut short- and medium-term lending rates to boost the economy and there has been some marginal easing of curbs in the property market. We expect the easing in policy will take a few months to feed through to an improvement in construction activity, so there will be little impact on the spot market and prices. Sheet prices will move closer to costs in the near future, and we foresee a price uptick after the holiday as demand gradually recovers.

Asia

Prices for imported sheet products in Asia increased this week on higher offers and bids, although trading activity is subdued ahead of the Lunar New Year holiday. For HR coil SAE1006, offers for Indian material remain the most competitive at $770-775 /t CFR Vietnam, while the highest bid was heard at $755 /t CFR Vietnam.

For SS400 HR coil, traders were offering Chinese material at $795-805 /t CFR Vietnam this week for March/early April shipment. A major Chinese steel mill was heard to have sold out their allocation to Vietnam last week at $790-800 /t CFR Vietnam for this grade, but this was mostly booked by traders as buyers in Vietnam have yet to accept this price level.

CRU assessed HR coil prices at $760 /t CFR Far East Asia, up by $ 15/t w/w. CR coil prices were assessed at $930 /t CFR Far East Asia, while HDG prices were assessed at $960 /t CFR Far East Asia, both up by $10 /t w/w.

India

HR and CR coil prices in India were unchanged w/w because traders held back on offering further discounts in anticipation of a possible increase in mill offers for February. Indian steelmakers are contemplating an increase in their sheet prices given the sharp upsurge in seaborne coking coal prices in the past few weeks. The benchmark premium hard coking coal price has increased from $357 /t on Jan. 4 to $438 /t on Jan. 25 on an FOB Australia basis, as per CRU assessment. This adds a significant cost pressure on Indian sheet producers, who have a strong reliance on imported coking coal for their BF-BOF steelmaking operations. Thus, mills are expected to pass on part of this cost rise to consumers in their February offers.

Meanwhile, coated sheet prices in India are already on the rise again. Market sources report that trade prices of HDG coil have increased by INR1000-1500 ($13-20) /t in the past week as steelmakers are promptly passing on the higher zinc costs. The LME 3-month Zinc price breached the $3,500 /t mark in late December and continues to remain strong because of ongoing supply shortages.

Near-term sheet market sentiment in India will be driven by the government’s FY2022-23 budget announcement on Feb. 1, 2022, wherein several taxation changes are anticipated for steel and steelmaking raw materials.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com