CRU

October 7, 2021

CRU: Iron Ore Prices Rebound After Chinese Holiday

Written by Erik Hedborg

By CRU Principal Analyst Erik Hedborg, from CRU’s Steelmaking Raw Materials Monitor

Iron ore prices have increased in the past week on post-holiday optimism that a real estate collapse can be avoided and the fact that steel production is increasing after the Chinese holiday. CRU has assessed the iron ore price at $132.0 /dmt, up by $16.5 /dmt in the past week.

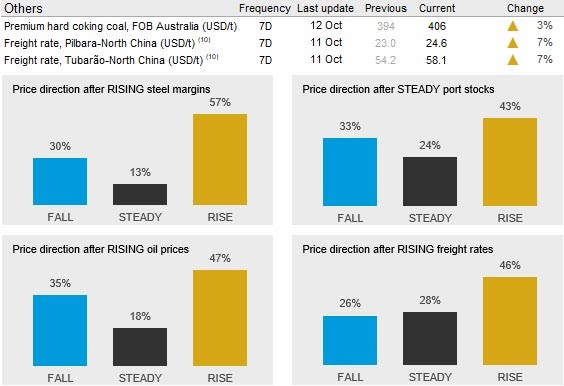

Chinese steel demand fell to a multi-year low during the China National Day holiday (Oct. 1-7), but post-holiday restocking pushed up steel prices that are now more than RMB100 /t higher than pre-holiday levels. In contrast to demand weakness, steel and hot metal production lifted, primarily driven by hot-idling BF restarts in Shandong and Jiangsu province. There will be more upside on steel production after a request to stop the “one-size-fits-all” style of steel production cuts was made in the recent state council meeting. Higher hot metal production and post-holiday restocking led to busier iron ore buying activity after onsite inventories were drawn down during the holiday. That said, iron ore outflow from ports to mills fell due to rainy weather, helping build up port inventories again.

In the past week, iron ore supply has been at its weakest point since Q1 this year. Shipments from both Australia and Brazil have been low recently and there are rumors in the market that Rio Tinto’s PBF and PBL shipments will be low in October and November due to continued quality issues. This has helped to drive up the lump premium in the past week, together with an announcement in Hebei that sintering would be restricted for three days at the end of this week. Going into the winter, our sources are expecting strong demand for direct-charge material in China and there are concerns around pellet availability due to the low exports coming from Brazil. In September, the country only exported 1.3 Mt of pellet, the lowest number since February this year (1.1 Mt) and considerably below the March-August average of 1.7 Mt per month.

For the next week, we expect iron ore prices to pull back as the post-holiday restocking will be over and inventories have climbed to a more comfortable level. Although seaborne supply has been weak, there is no shortage in China at the moment and the long vessel queue means offloading activities will remain at high rates even if iron ore arrivals decline in the coming weeks.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com