CRU

July 29, 2021

CRU: U.S. Zinc Demand Strength Continues Through Summer Months

Written by Helen O’Cleary

By CRU Senior Analyst Helen O’Cleary

U.S. refined demand continues to impress through the traditionally slower summer months, with market contacts reporting still-strong off-take under long-term contracts into August. We hear that many consumers continue to take the higher end of their contracted metal tonnage, with some still buying additional spot quantities. A further increase in U.S. domestic steel sheet prices in early July reflected the strength of demand. Manufacturing and construction activity remains strong despite sky-high freight rates and serious reliability issues in the sector, coupled with a tight labor market.

Mexican Smelters Beset by Production Issues

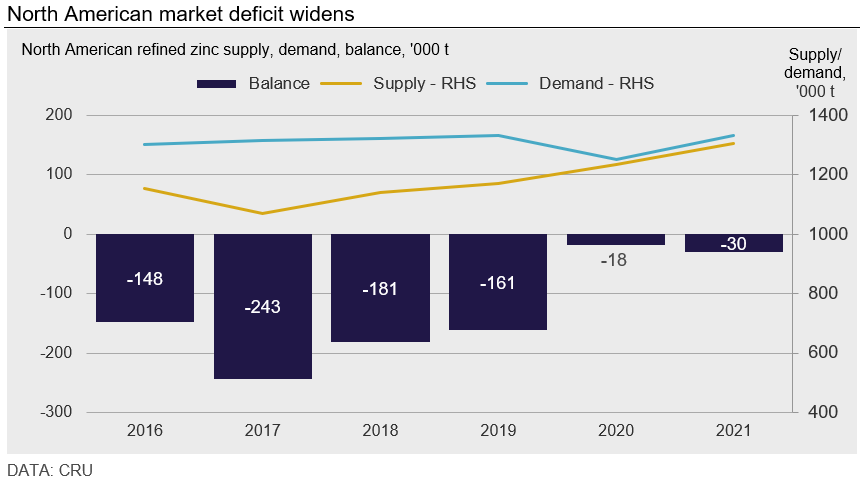

While U.S. demand has gone from strength to strength so far this year, North American supply has underperformed, largely due to issues in Mexico at Peñoles’ Torreon and Grupo Mexico’s San Luis Potosi smelters. We were expecting the ramp-up at Torreon to get back on track this year, but it has been beset by issues which have constrained output. Last month we reported that the smelter was having quality issues and this month we heard that one of the smelter’s three roasters is out of action, which is likely to disrupt refined output. We also heard that San Luis Potosi is also still struggling to return to full utilization. The combined capacity of these two smelters is 457,000 t, but we have reduced our expectation of Mexico’s refined output in H1 to 177,000 t and 391,000 t for the year.

We have not heard of any disruption to smelter output elsewhere in North America, but risks are to the downside. Wildfires in British Columbia are a potential threat to Teck’s Trail smelter operations, and we understand that there have been some railway freight issues. Also, the recent fatality at Nyrstar’s Tennessee mine could affect concentrate supplies to Clarkesville, and further refined output losses in the region could lead to another increase in spot metal premia.

Strong demand and further downward adjustments to refined output have led to a further tightening of the North American market, which we now estimate will record a 30,000 t deficit in 2021. It is possible that we will see more outflows from LME stocks to meet end-use demand. On July 9, LME stocks in the USA stood at 96,550 t (88,400 t in NOLA and 8,150 t in Baltimore) and in May, U.S. off-warrant stocks as reported by the LME were 20,000 t.

The USA’s refined net imports fell 22.3% y/y in January-May, from 337,000 t to 262,000 t. It is worth noting that last year’s net imports were high due to COVID-19-related stock movements, but regular imports for end-use consumption from Canada, Mexico, Peru and Brazil are all lower this year, the latter two due to lower-than-expected output from Nexa and strong demand in Brazil.

Our assessment is unchanged this month at 8.75¢/lb.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com