Product

July 20, 2021

SMU Steel Price Ranges & Indices: Hot Rolled Hits $1850

Written by Brett Linton

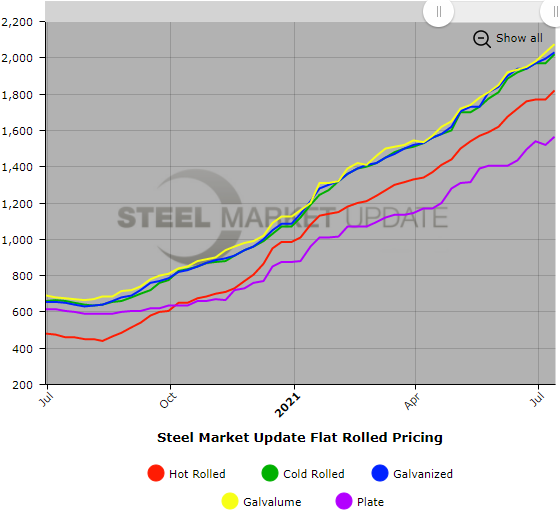

Flat-rolled steel prices continue to shoot upward – with no signs of the summer doldrums, the chip shortage or fears of a correction blunting their momentum. U.S hot-rolled rolled coil prices now stand at $1,850 per ton ($92.50 per cwt), up $30 per ton from a week ago. Cold-rolled coil and galvanized base prices notched similar gains and now average $2,060 per ton ($103 per cwt). With lead times long, inventories lean and no new capacity coming until the fourth quarter, most market participants contacted by Steel Market Update don’t see prices slipping anytime soon. “They’re not even negotiating what tons we can get, let alone pricing. The mills definitely have the upper hand,” one respondent to our survey said. Reflecting such sentiment, SMU’s Price Momentum indicator continues to point toward higher prices for all steel products over the next 30 days.

Here is how we see prices this week:

Hot Rolled Coil: SMU price range is $1,800-$1,900 per net ton ($90.00-$95.00/cwt) with an average of $1,850 per ton ($92.50/cwt) FOB mill, east of the Rockies. The lower end of our range remained unchanged compared to one week ago, while the upper end increased by $60. Our overall average is up $30 per ton from last week. Our price momentum on hot rolled steel is Higher, meaning prices are expected to rise in the next 30 days.

Hot Rolled Lead Times: 9-13 weeks

Cold Rolled Coil: SMU price range is $2,000-$2,120 per net ton ($100.00-$106.00/cwt) with an average of $2,060 per ton ($103.00/cwt) FOB mill, east of the Rockies. The lower end of our range increased $60 per ton compared to last week, while the upper end increased $20 per ton. Our overall average is up $40 per ton from one week ago. Our price momentum on cold rolled steel is Higher, meaning prices are expected to rise in the next 30 days.

Cold Rolled Lead Times: 10-14 weeks

ARTICLE CONTINUES BELOW

{loadposition reserved_message}

Galvanized Coil: SMU price range is $2,000-$2,120 per net ton ($100.00-$106.00/cwt) with an average of $2,060 per ton ($103.00/cwt) FOB mill, east of the Rockies. The lower end of our range remained unchanged compared to one week ago, while the upper end increased $60 per ton. Our overall average is up $30 per ton from last week. Our price momentum on galvanized steel is Higher, meaning prices are expected to rise in the next 30 days.

Galvanized .060” G90 Benchmark: SMU price range is $2,069-$2,189 per ton with an average of $2,129 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 12-15 weeks

Galvalume Coil: SMU price range is $2,030-$2,120 per net ton ($101.50-$106.00/cwt) with an average of $2,075 per ton ($103.75/cwt) FOB mill, east of the Rockies. The lower and upper ends of our ranges remained unchanged. Our overall average is unchanged from one week ago. Our price momentum on Galvalume steel is Higher, meaning prices are expected to rise in the next 30 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $2,321-$2,411 per ton with an average of $2,366 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 12-14 weeks

Plate: SMU price range is $1,440-$1,710 per net ton ($72.00-$85.50/cwt) with an average of $1,575 per ton ($78.75/cwt) FOB mill. The lower end of our range remained unchanged compared to one week ago, while the upper end increased $20 per ton. Our overall average is up $10 per ton from one week ago. Our price momentum on plate steel is Higher, meaning prices are expected to rise in the next 30 days.

Plate Lead Times: 6-10 weeks

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume and plate price history. This data is available here on our website with our interactive pricing tool. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com.