CRU

January 15, 2021

CRU: European Prices Approach a Peak

Written by Matthew Watkins

By CRU Principal Analyst Matthew Watkins, from CRU’s Steel Sheet Products Monitor

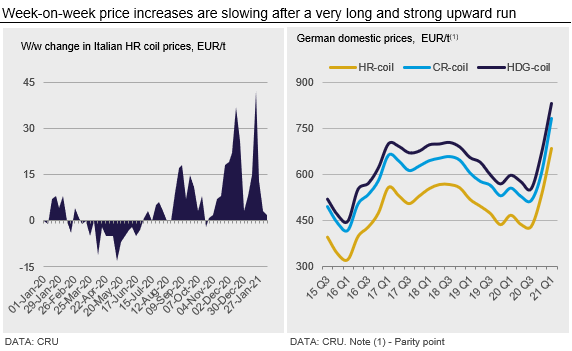

Prices in Europe have surged higher once more over the past month, though the pace of weekly increases is showing signs of changing.

Overall, our 2nd Wednesday price in February is much higher m/m for all sheet products across Europe. This continues what is now an unusually long upward run. It is now 16 weeks since European HR coil prices last fell w/w, which is comparable to the run seen in early 2016. Moreover, that last w/w fall was a single-week event during October, before which there had been another 16-week period of constant increases. Prices are now at least €300 /t higher than their low point of late-June, which is a total increase of 62-88% in that time, depending on product.

Higher steel prices have brought higher input costs, but also higher margins. Despite a slight pullback in recent weeks as peak iron ore prices have fed through, our modelled spot EBITDA margin for a German steel mill remains higher than almost anything seen in the last boom period of 2017-18.

These very attractive margins are incentivizing supply to the market. All Covid-19 related asset idlings are accordingly now reversed in Europe with the recent restart of Taranto BF2, while Gent BF B will also shortly resume following a reline. Moreover, USS Košice is running on three furnaces again, which was not the case since before the pandemic hit. Each furnace at Košice is larger than the one at ArcelorMittal Kraków that was permanently closed in 2020, meaning that switch is a modest net addition.

Outside the European sheet market there have been some very visible moves lower. These are most obvious in scrap, where Turkish import prices have dropped by almost $80 /t in three weeks. Turkish steel prices have followed and steel prices in Asia have also been falling for several weeks. So far in Europe, these changing dynamics have not registered in price falls, but in the most recent weeks the pace of price increases looks to be slowing. Buyers have become much more cautious and are no longer willing to accept whatever price increase the mills request.

Outlook: A Fall is Likely…But Will We Now See a Double Top?

Of course, if buyers urgently need the steel then they can act as cautious as they want but will ultimately have to pay its price. But our market is revealing a rising number of buyers that have now secured input material to cover the next several months and do not necessarily need to buy again right away.

Moreover, with lockdowns still in effect across much of Europe and auto production being interrupted from the global semiconductor shortage, the near-term downside risk to demand remains clear.

Until now these have been factors that helped drive our forecast for a steep price fall. And they still are, but as we have previously discussed there is considerable uncertainty about when this fall will happen; basically, we expect it sometime before mid-year. Our Asian team is becoming more bullish on demand prospects in China and the wider region after New Year. If prices in Asia were to go back up once holidays are over, it seems somewhat less likely that prices in the West would go through a large collapse. Accordingly, we are starting to think about a scenario where we see a double top in prices; a pullback now, in line with the softening already seen in the East, but followed by a resurgence and then the big price fall comes a bit later, probably still before mid-year.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com