Prices

November 3, 2020

CRU: Scrap Prices Rise as Global Steel Markets Recover

Written by Ryan McKinley

By CRU Senior Analyst Ryan McKinley, from CRU’s Steel Metallics Monitor

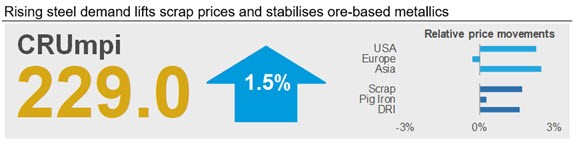

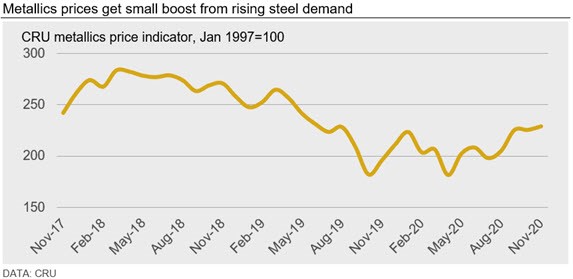

The CRU metallics price indicator (CRUmpi) increased by 1.5% m/m in November to 229.0. The increase in scrap prices in most regions has been driven by a continued recovery in steel prices and demand. Moving into December, we expect higher steel pricing and demand globally to lift scrap, pig iron and DRI/HBI prices once again.

Rising steel prices in most markets across the globe provided upward pressure for scrap prices in November. Stronger scrap demand means many scrap markets have either tightened or are poised to be tighter soon. Scrap prices in Brazil and Asia were the strongest, breaking all-time and 2020 highs, respectively. Meanwhile, relatively softer conditions were observed in the USA and Europe, more so for the latter.

Scrap prices in Brazil once again hit a record high after increasing by more than 10% m/m. Even with prices at a record level, scrap processors are having trouble collecting enough material to meet demand because industrial activity that would generate scrap is still slow. However, construction activity remains high and this has filled steel mill order books and expanded lead times. As a result, competition for scrap has continued to intensify among steelmakers in the country, causing prices to rise and export levels to plummet.

In Asia, prices in nearly every country we cover reached their highest level so far in 2020. Supply has become more limited in the region even as demand in countries like Vietnam, Japan and the Philippines continues to increase. Adding to upside price pressure in these markets are higher freight rates, as grain and garment exporters compete for container access. Meanwhile, in China, strong underlying steel demand has resulted in a sharp increase for both rebar and HR coil prices. This rapid increase in steel demand caused a quick destocking of scrap inventories, and prices are now at their highest point since January 2013.

Strong international steel demand also resulted in strong order books for Turkish mills, despite weakening demand in their own domestic market. In turn, this is has allowed them to accept higher import scrap offers and the most recent deals have concluded at levels that are about $20 /t higher m/m. Still, these import prices are somewhat weighed down by decent scrap availability in European markets.

Indeed, many European markets were exceptions to rising scrap prices internationally. Although demand is still recovering from Covid-19 lockdown lows and export volumes are stable, supply availability is high enough to balance the market. Only in Russia did prices increase, and this was driven by heightened mill competition as they try to fill their scrap inventories ahead of winter.

Across the Atlantic, domestic U.S. mills entered the market at unchanged prices this month, but some accepted higher price levels as trading continued through Nov. 10. Still, these increases varied greatly by region and grade, and were not uniformly accepted across the country. Despite an increase in #1 busheling prices, domestic finished steel prices are quickly outpacing gains in scrap, causing the HR coil premium to prime grades to reach a two-year high.

Pig iron buyers in both the U.S. and Europe were largely absent from the international market as prices remain at elevated levels. Although Chinese purchasing activity was subdued for much of October, recent negotiations indicate the prices are, and will continue to be, stable in the near term.

Outlook: Yet More Upside Price Pressure Ahead

With finished steel prices still on the rise and scrap markets seasonally tighter in many areas, we expect that both ore-based metallics and scrap prices will rise in December. An exception to this may again be in Europe as countries there go back into lockdown, although if this limits scrap supply, prices may still find some support.

Although Chinese buyers are now back in the international ore-based metallics market, supply availability may be weaker as Brazil moves closer to its rainy season. Additionally, we understand that pig iron supply from Russia may also fall after a blast furnace there was idled temporarily.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com