Prices

November 3, 2020

CRU: Iron Ore Prices Continue to Rise on Buoyant Steel Market

Written by Eduardo Tinti

BY CRU Research Analyst Eduardo Tinti, from CRU’s Steelmaking Raw Materials Monitor

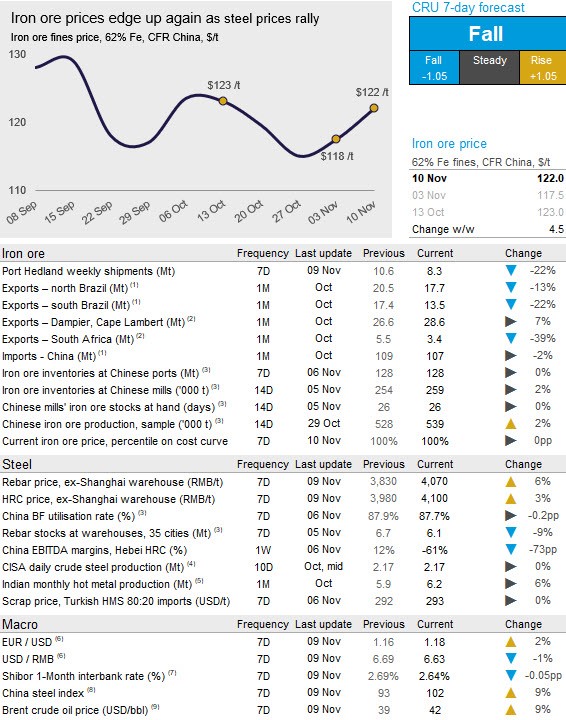

Iron ore prices edged up for the second consecutive week as Chinese domestic steel prices rallied and the seaborne iron ore supply weakened. On Tuesday, Nov. 10, CRU assessed the 62% Fe fines price at $122.0 /dmt, $4.5 /dmt higher w/w.

Chinese domestic HRC and rebar prices have both risen sharply over the past week, up by RMB120 /t and RMB240 /t w/w, respectively. Though underlying demand remained robust and steel production has fallen, mainly due to scheduled maintenance at rolling mills, such a strong price hike is surprising. According to market contacts, transaction volumes have been high in eastern China and, despite rising prices, some products were reported sold out. Such intense buying combined with lower production resulted in quicker inventory drawdown across the supply chain, particularly for rebar. Despite marginally stricter WHS restrictions in Tangshan city, Chinese BFs continue to operate at high capacity utilization rates. Robust hot metal production and iron ore restocking at steel mills have supported iron ore demand and prices over the past week. Meanwhile, iron ore inventories at ports remained steady at the highest level since May 2019 as the number of vessels queueing to offload continues to decline.

On the supply side, weekly shipments were at the lowest level since July. Port Hedland shipments declined by 2.4 Mt w/w to 8.3 Mt as exports from BHP and FMG fell while Roy Hill did not load any vessel during its scheduled quarterly 7-10 day port maintenance started last week. Brazilian iron ore exports also dropped w/w both from the north and from the southeast. In the north, market contacts mentioned rains and port issues as reasons behind lower weekly shipments.

In the coming week, we expect Chinese steel prices to remain high, underpinned by bullish market sentiment. Healthy margins will incentivize steel mills to continue operating at high run rates. On the other hand, we expect the seaborne supply to recover. Moreover, as the number of vessels waiting to offload at Chinese ports continues to decline, we believe more iron ore will be available to Chinese buyers, easing the pressure on prices. Consequently, we expect iron ore prices to pull back from current levels in the coming week.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com