Market Data

November 3, 2020

CRU Economists: Our Top Ten Calls for 2021

Written by Jumana Saleheen

By CRU Chief Economist Jumana Saleheen and Principal Economist Alex Tuckett, from CRU’s Steel Monitor

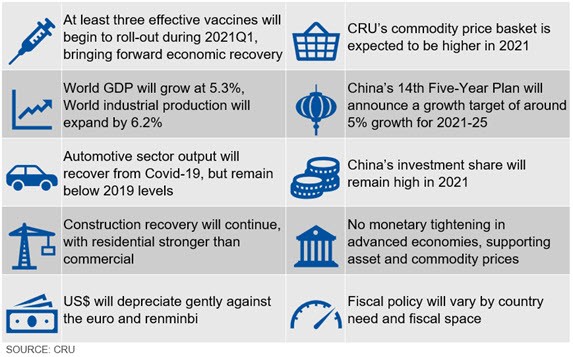

In this Global Economic Outlook, we look ahead to 2021 and outline our top ten calls for the global economy. These include predictions on Covid-19 vaccines, world growth, the auto and construction sectors, the U.S. dollar, monetary and fiscal policy, commodity prices and China.

At Least Three Vaccines Will Begin to be Rolled Out from Q1

Recent weeks have brought good news on vaccines. The Pfizer-BioNTech, Moderna and Oxford vaccines have all shown high efficacy rates in Phase III trials. Although none yet has regulatory approval, this could come quickly.

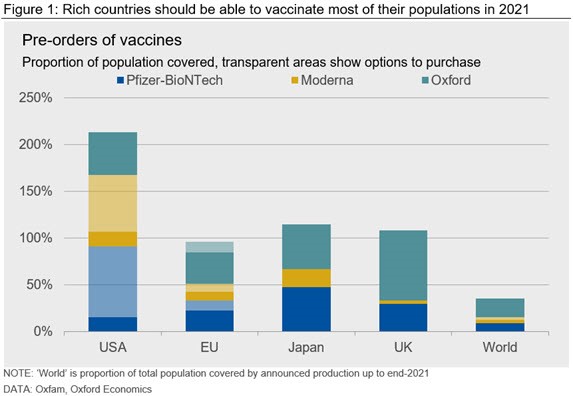

Many advanced economies have already placed pre-orders (see Figure 1), large enough to vaccinate substantial sections of their populations. Developing countries will face a longer wait. We expect vaccination of some groups to start in the USA, Europe and Japan during Q1, with most of the population in advanced economies vaccinated by end-2021. However, roll-out of the vaccine to the global population is likely to stretch into 2022 at least. Based on current projections, production of the current vaccines in 2021 will cover at most a third of the global population. However, further vaccines using similar technology are in the pipeline.

We have revised our previous judgement that a vaccine will be widely available, from the middle of next year to the first half of next year. The substantial risk of a vaccine failing to appear is now almost gone. Although vaccines will not resolve the pandemic in Q1, we expect the encouraging vaccine news to provide a boost to confidence and spending in Europe and the USA, which has led us to raise our growth forecasts in the first quarter of 2021.

Global Recovery to Continue in 2021

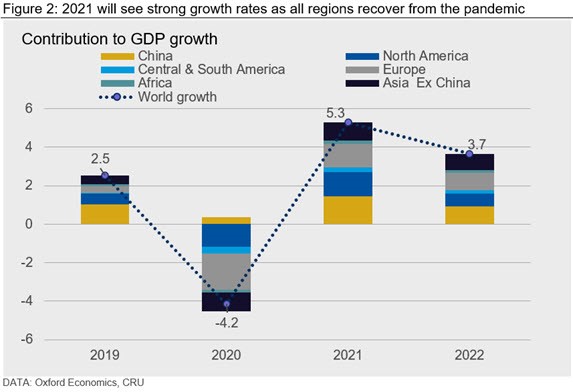

We expect the world economy to grow by 5.3% in 2021. However, the high year-on-year growth rate reflects how bad 2020 was, with GDP falling by 4.2%. The bulk of growth will come from China, which continues its strong relative performance through the pandemic, and from recoveries in Europe and North America (Figure 2).

Industrial production is expected to grow by 6.2% in 2021. As with world GDP, strong annual growth in 2021 will mainly reflect the severe contraction of 4.5% in 2020. Overall, industrial production has remained resilient compared to previous global recessions when it typically fell more sharply than overall GDP.

Automotive Output Recovers from Covid-19, But Not from Pre-existing Conditions

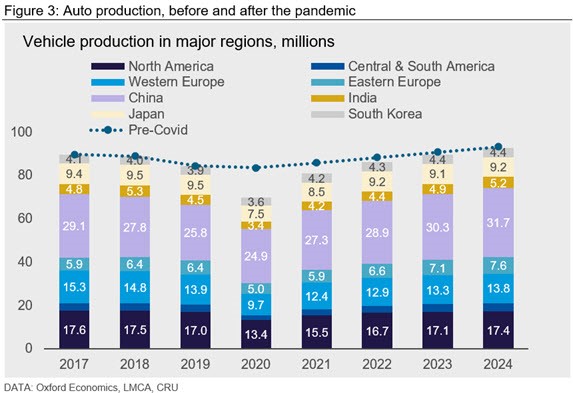

Auto production was one of the hardest hit sectors within industrial production during the pandemic. Complex supply chains suffered severe disruptions, social distancing closed showrooms in many countries and uncertainty reduced demand. The second half of 2020 has seen a sharp recovery. Monthly production is now up on a year earlier in China; it has fully recovered in the USA and is only marginally down in Western Europe. We expect global production in 2021 to be 16.6% higher than in 2020. However, production will still be below 2019 levels (see Figure 3). This partly reflects long-term challenges the industry faced before the pandemic, and in particular the energy transition and the tightening of environmental regulations in Europe, China and India. Before Covid-19 we had forecast a fall in production in 2020, followed by only modest growth in 2021.

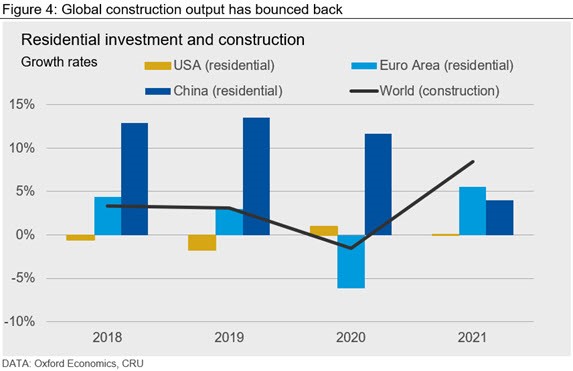

Construction Recovery Will Gain Momentum

We expect global construction output to increase by 8.4% in 2021, after contracting by 1.5% in 2020. As with GDP, the strong growth rate in 2021 partly reflects the depth of the 2020 recession, rather than strong momentum through the coming year.

Construction is a highly cyclical industry, tending to fall by more than GDP in a recession. Construction has been more resilient in this crisis than normal, for three reasons. First, construction has been less affected than consumer services by social distancing restrictions. Secondly, in advanced economies the economic crisis has disproportionately affected younger, lower-income workers. This group is less likely to own their homes, and so has less impact on demand for new housing or upgrades. Finally, falls in interest rates and fiscal transfers have supported the buying power of those able to buy homes.

In 2021, residential construction will continue to support growth, but non-residential construction will also join the recovery. Demand for industrial and infrastructure projects will be stronger, but demand for retail and office space will remain weaker.

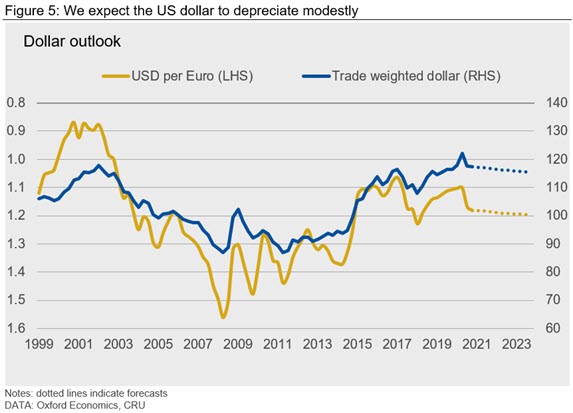

The Dollar Will Depreciate Gently Against Euro and Renminbi

Several measures of fair value suggest that the U.S. dollar is modestly (5-10%) overvalued against the Euro. For this reason, we expect a gentle depreciation of the dollar against the Euro in 2021, reaching $1.19/Euro by the end of 2021 (Figure 5).

There are substantial uncertainties around this view. A resurgence in global risk appetite – for example if vaccines become available beyond advanced economies – could push down the value of the dollar against a range of currencies. A disappointment in U.S. fiscal stimulus could push the dollar down against the Euro (and a reverse surprise could have the opposite effect). The re-emergence of fiscal risk within the Eurozone could push the dollar up.

We also expect the dollar to fall modestly against the Renminbi. As China has led the global recovery, it has experienced strong capital inflows from international investors. The Chinese authorities will want to avoid sharp appreciation of the Renminbi against the basket of currencies that they monitor. However, the dollar depreciating on a broad basis would be consistent with the Renminbi-dollar exchange rate rising modestly to around 6.5 by the end of 2021.

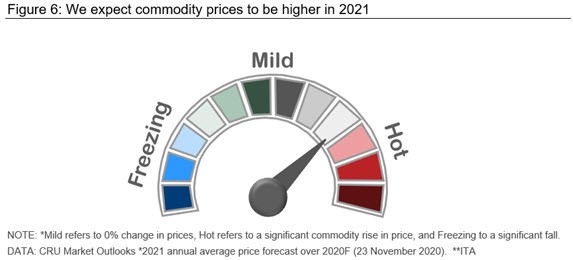

The Outlook for Commodity Prices in 2021 is Strong

As the economic recovery continues, CRU’s basket of 38 mining, metals and fertilizer prices is expected to rise by 7.2% y/y in 2021. Much of this apparent strength will be driven by the average for 2020, which fell 9.4% as a result of Covid-19. All components are higher compared to last year; precious metals are 9.7% higher y/y, raw materials 8.1% higher, metals 7.5% and fertilizers 3.9%. Strong free cash flow generation will benefit some producers as demand recovers, while others will be held back by a lack of investment and by market imbalances. Commodity producers will also continue to adapt to changing ESG standards, as these become more important for investors.

The oil price has rebounded in response to the news on vaccines, in anticipation that this will speed the recovery in economic activity and travel. However, actual demand volumes remain weak and will take time to pick up. We forecast that Brent crude will average $51/bbl over 2021.

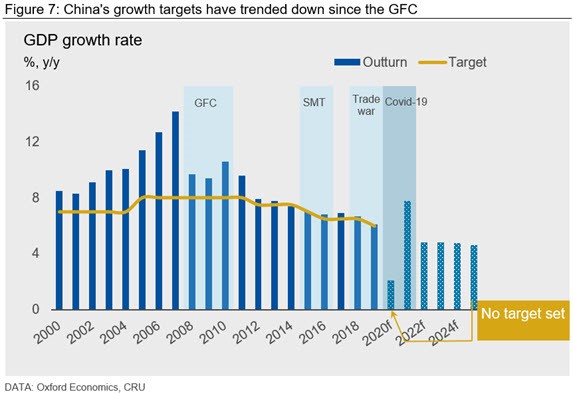

China Will Announce a Five-Year Growth Target of Around 5%

2020 will see the announcement of China’s 14th Five-Year Plan (FYP), probably in March. FYPs generally feature the announcement of a range of targets covering economic, social and environmental goals, including an explicit target for GDP growth. Our previous analysis has found that China achieved around 70% of the goals set out in its 13th FYP.

We expect the Chinese government to announce a target for average growth of around 5% over the period 2021-25, significantly lower than the target of 6.5% set in the 13th FYP for the period 2016-20. This reflects the cold reality of growth convergence. As China catches up with advanced economy levels of income, growth rates will inevitably slow. Many of the easiest gains from transferring labor from rural agriculture to urban services and manufacturing have already been achieved. Additionally, demographic change means the working age population will begin to shrink. The government will be mindful that pushing growth above its potential will build up imbalances, such as further sharp rises in debt.

China will almost certainly exceed the target in 2021; the pandemic reduced the level of GDP in 2020 so the comparison will artificially inflate the 2021 growth rate. Thereafter, annual growth rates will be more modest.

Also, look out for a range of targets for environmental metrics, as China begins the long path towards limiting carbon emissions to meet its target of carbon neutrality by 2060.

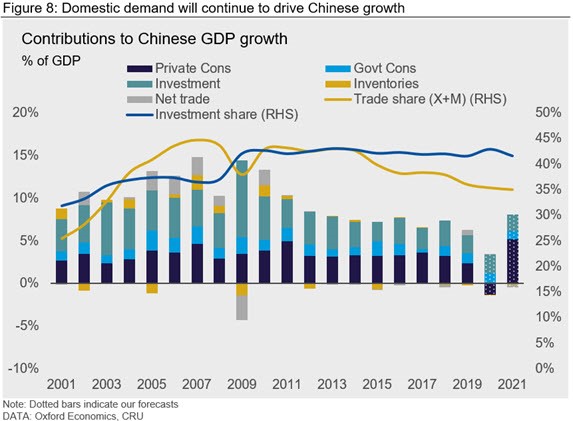

China’s Investment Share Will Remain High

China will be the only major economy to grow in 2020, and its rapid recovery from the pandemic has set it up for growth of 7.9% in 2021, the fastest rate since 2013. We expect domestic demand to remain the driving force behind growth (Figure 8). China’s industries will continue their long-term shift towards its huge internal market, in line with the “Dual Circulation” policy platform.

Dual Circulation aims to increase the share of private consumption in GDP. 2021 will see private consumption making its strongest contribution to growth in the post-WTO era. However, investment will still account for a high share of GDP in 2021 (Figure 8). The government will stand ready to underwrite the recovery with further stimulus, particularly if external demand fails to materialize as expected. Continued strong investment spending will boost demand for metals.

Monetary Hawks Remain an Endangered Species

During the downturn, monetary policy played an important supporting role in reducing stress in financial markets and improving funding conditions for companies. This limited corporate insolvency and, in the case of the Eurozone, fiscal risk.

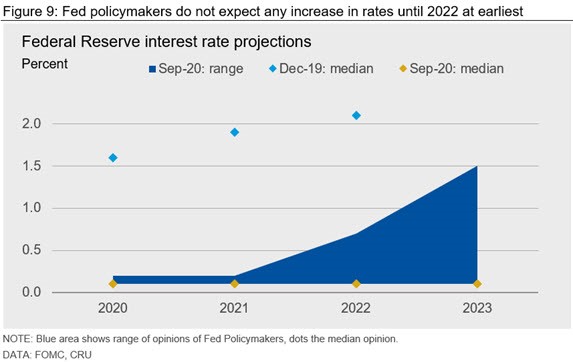

In 2021, we expect monetary policy to remain highly accommodative in advanced economies. Policy interest rates will not increase (Figure 9), and central banks will remain willing to use additional quantitative easing (QE) to support the recovery. By keeping short and long interest rates at historically low levels, central banks will continue to support asset prices, including prices of tradable commodities

So far, monetary policy in emerging markets has not been as loose as in advanced economies. Without the same confidence in institutions, and in the face of often large currency depreciations, policymakers have had to protect their credibility with investors. As with fiscal policy, a broad recovery in risk appetite could give emerging market central banks more leeway to support their domestic economies.

Fiscal Policy Determined by Country Need and Affordability

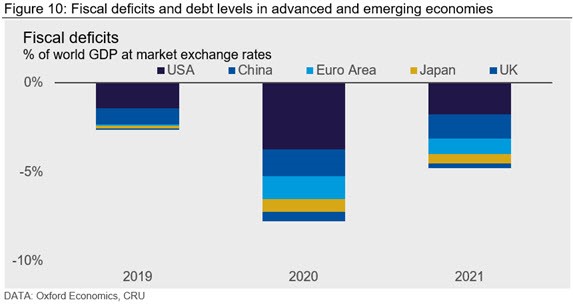

The pandemic has seen huge fiscal responses across most advanced economies, most dramatically in the USA (Figure 10). Governments will want to avoid the mistakes of the previous crisis when premature tightening of fiscal policy damaged the recovery in Europe. Furthermore, with interest rates so low, many advanced economies will be under little immediate pressure to reduce deficits. Nonetheless, we expect the picture for fiscal policy in 2021 to vary by country. Governments will pursue different strategies depending on the need to combat the pandemic or support the recovery, and depending also on fiscal space.

The degree of fiscal support in the USA will depend on politics, as set out in our recent insight. Other countries – such as Italy – lack fiscal space and will need to limit the increase in debt brought about by the pandemic. Emerging markets will continue to face a more delicate balance between supporting their economies and maintaining the confidence of financial markets.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com