Market Segment

July 14, 2020

CRU: How Russian Steelmakers Could Capitalize in a Post Covid-19 World

Written by Iris Speelmanns

By CRU Analysts Irina Melkonyan and Iris Speelmanns, from CRU’s Steel Sheet Products Market Outlook

Russia is among the biggest steel exporters in the world, delivering to a wide range of destinations. However, steel demand in all regions diminished as the world was hit by Covid-19 and most steel producers globally have struggled. Unlike steelmakers in other regions, Russian producers did not idle capacity but extended maintenances and lowered capacity utilization in order to reduce output. Going forward, however, they will have to decide whether to take more decisive measures to keep production restricted, dependent on their ability to leverage their cost competitive advantages and the growth opportunities that export markets present.

Given that domestic steel demand is expected to remain weak in 2020, we believe that Russian mills will increase exports due to their low-cost advantages. There will be stronger exports to the EU, with expanded quota volumes, and to Southeast Asia, where demand is expected to recover faster than in other regions. This will not be enough, however, to sustain 2019 output levels and production in Russia will decline by 8 percent y/y.

Even during 2021, Russian demand is not expected to recover to pre-pandemic levels and output will be dependent on export demand. There is a risk of lower exports to the EU ultimately, due to the possible introduction of carbon border tariffs that could, feasibly, be introduced during the year. Sales to Southeast Asia, however, will be strong as demand there will be rising fast. As a result, net exports will rise and steel production will return to pre-Covid-19 levels by end-2021.

A Strong Domestic Market Premium Reduced Russian Steel Exports in 2019

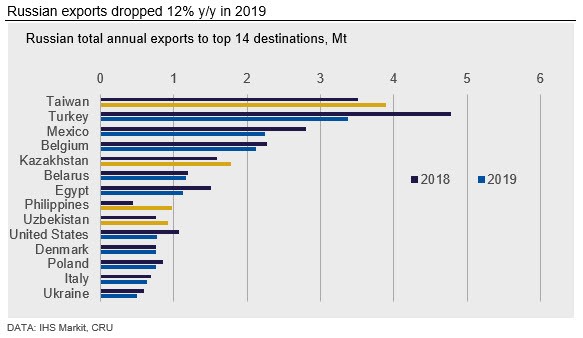

In 2019, carbon steel exports from Russia reduced by 12 percent y/y, to 27 Mt, as sales to traditional markets, such as Turkey, North America and the EU, fell sharply. On the other hand, exports to Asia rose by 9 percent, with Taiwan remaining the main destination and receiving over 3.5 Mt of material.

Total exports were lower for a few reasons. Firstly, domestic demand for finished steel products in Russia increased by almost 10 percent during the year, while crude steel production remained virtually unchanged due to an already high capacity utilization. This pulled the domestic market premium higher—for rebar it was $55 /t in 2019 compared with just $5 /t in 2018 and, for HR coil, the premium was $107 /t in 2019 compared with $55 /t a year earlier. With high premiums, producers naturally diverted more material to the domestic market to maximize profits.

Secondly, traditional export markets for Russia shrunk through the year, as Turkey faced an economic downturn and exports to the EU were restricted by safeguard measures. In the USA, the problem was twofold: end-user demand fell, while local steelmaking capacity had been increased following the imposition of Section 232 tariffs, partially offsetting the need for imports. This led to a decrease in total steel imports, including a 28 percent drop in imports from Russia.

Domestically, the construction sector showed a particularly strong performance, stimulated by legislative changes regarding how companies could raise money for new projects. According to Rosstat, the Russian statistical service, residential construction rose by 5 percent y/y in 2019. While residential construction primarily supported demand for long products, strong infrastructure construction boosted demand for longs, sheet and plate.

Russian Mills Cut Q1 Output During Planned Maintenance

At the beginning of 2020, it was announced that Russian steel production would be reduced during the first half of the year due to repairs at several mills, including extensive maintenance at MMK—Russia’s biggest sheet mill. According to our estimates, output at MMK would reduce by 2.5 Mt starting from March. The market rapidly priced in the news of lower sheet supply and some restocking took place during the typically quiet Q1 period. This supported Russian prices in Q1 and resulted in strong margins during the period (see chart). Given that Russia was producing at high capacity, exports had to fall as mills were redirecting sales to the more profitable domestic market. Thus, Russian total steel exports fell by almost 8 percent y/y in Q1, and ~70 percent of the reduction was due to lower sheet and slab exports.

Low Cost Russian Mills Have an Advantage During an Economic Downturn

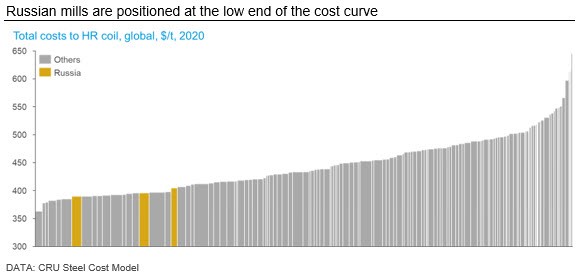

The Covid pandemic started in Q1, reducing normal economic activity and diminishing global steel demand. Large exporters, such as Russia, were affected, with exports falling from March onwards. However, Russian producers are very low cost, which makes their products highly competitive in export markets. Steelmakers in the country benefit from economies of scale and, while many are also vertically integrated for raw materials, all benefit from structurally lower domestic raw material prices. Compared with some other regions, Russian mills also have the advantage of lower labor, electricity and fuel prices. The Russian ruble, which can be viewed as a source of risk and volatility, can also be beneficial, as its depreciation deflates ruble-denominated costs.

During economic expansion and periods of high prices, lower costs mean higher margins. During a downturn, such as the one in which the world now finds itself, many of the above factors can favor Russian mills (i.e. low energy prices, depreciated ruble etc.) to consolidate their position on the cost curve. This means that Russian mills can sustainably lower their prices to a greater degree than competitors in the export market to maintain market share.

Introduction of Scrap Quotas Will Reduce Costs Only Temporarily

Scrap is one of the raw materials that is easily accessible domestically and provides competitive advantage to Russian producers. However, currently, the Russian government is considering a change to the structure of the scrap market. Our view is that the changes proposed will reduce steelmaking costs initially, but will be detrimental longer term.

Russia is a key exporter of scrap, shipping an average of 5.2 Mt/y over the past five years. In late-2019, after a four-month experiment with scrap quotas, the Russian government announced its intention to keep scrap exports restricted either by introducing a “scrap exchange” or prolonging the quotas. It is clear that this decision was lobbied by some local steelmakers that are seeking to keep material availability high. However, currently, there is no consensus on what exactly the measures will be.

If changes to scrap market structure do go ahead, it is likely that scrap exports will be restricted and this should reduce scrap prices in the short term, which will improve the overall cost competitiveness of the steel sector. Over the longer term, however, we expect that lower scrap prices will reduce the economic incentive to collect, transport and process scrap, limiting supply availability and, potentially, leading to shortages. Ultimately, restricted supply and consistent demand from domestic producers should increase scrap prices, but the mills would then face a smaller pool of material from which to choose.

In our view, while this policy will give a cost advantage to Russian steelmakers, as scrap prices will drop temporarily, it will have negative impact in the longer term.

Russian Demand Falls 28 Percent During the Q2 Lockdown

Before the start of the pandemic, Russian GDP was forecast to grow by 1.6 percent y/y in 2020, due to expected strong performances of the construction and infrastructure sectors, as well as potential for a recovery in domestic auto production. These hopes were quickly eradicated by the significant reduction in economic activity from March to May, when Russia was in lockdown and industrial production was restricted in some regions. Official statistics for the second quarter are not yet available, but we expect Q2 GDP to fall by ~9.5 percent y/y, while annual GDP is expected to fall by 5 percent y/y.

Such a reduction in economic activity implies a drastic drop in domestic steel demand and, according to CRU’s June estimates, Russia will lose 28 percent y/y of total finished steel demand in Q2. In many countries, for example China, Japan, Germany and the USA, the reduction in demand was accompanied by the idling of assets, as negative margins prompted producers to cut marginal sales and minimize losses. In Russia, production was already lowered due to maintenance at MMK and more reductions were made through maintenance being pulled forward at other mills or via lower capacity utilization. This allowed producers in Russia to avoid idling capacity while reducing output. However, while demand in Q2 is expected to have fallen by 28 percent, production is expected to have declined by only 20 percent y/y.

This response means that the Russian steel market has been, and continues to be, oversupplied and the excess production will keep putting pressure on domestic prices and profitability; which brings us back to the question: will Russian producers be able to expand export sales or will they be forced to keep output reduced?

Revised EU Quotas Create Some Opportunities for Russian Export Growth Post Covid-19

As of June, Russia has lifted its national lockdown and normal economic activity can continue, but only modest and delayed governmental support for citizens and businesses is likely to result in a higher unemployment rate, bankruptcies and reduced aggregate consumption. Under these circumstances, the export market will play a bigger role for Russian steel producers and, in order to avoid further output reductions, Russian mills will need to expand their presence in export markets.

The EU is Russia’s single largest steel export market and sales to the region accounted for a quarter of total exports in 2019. Russian exports to the EU in 2020 will depend on both end-use demand in the region and extant trade protective measures.

Over the last few months, European finished steel demand fell to its lowest point in over a decade as European economies were forced to enact lockdown measures to combat Covid-19. The pandemic has primarily affected manufacturing activity in the auto and engineering sectors, while construction activity has performed comparatively better. Thus, European longs demand has performed marginally better than sheet demand so far this year. We expect that steel demand will begin to gradually recover in 2020 Q3, as Europe loosens its lockdown measures and steel consuming sectors become more active. However, growth will remain relatively subdued for the rest of the year, with demand only growing significantly from 2021 onwards.

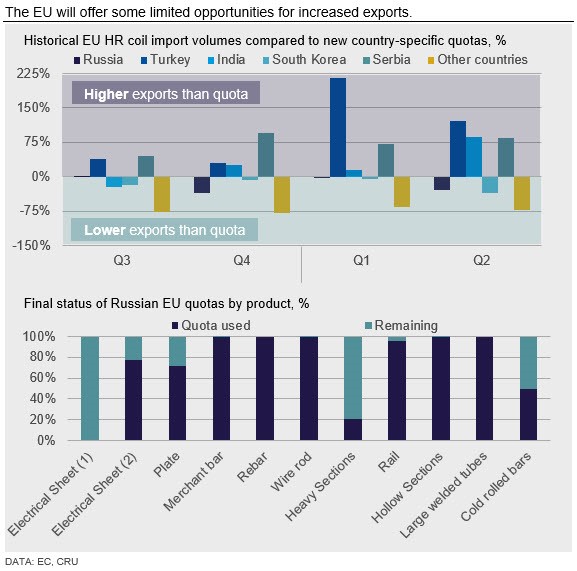

Given the change in circumstances, the European Commission (EC) has revised its safeguard quotas for the period from July 1 onwards and, contrary to the expectations of many market participants, quota volumes have not been reduced, despite the fall in demand due to Covid-19. In fact, total volumes for rebar, rod and wire will be increased by the 3 percent established in an earlier revision of the quota for the period July 1, 2020, to June 30, 2021. In the last quota year, from July 1, 2019, to June 30, 2020, Russia filled its quotas for rebar, wire rod and wire, hence the 3 percent increase will benefit these product groups.

More structural changes were made to the HR coil quota, which was converted to a series of country specific quotas, but Russian exports of HR coil in 2019 were lower than the updated 2020-2021 quota will now allow. This means that Russian mills will have an opportunity to export even more than they have historically, given that some of Russia’s competitors in the export market, especially Turkey, are dealing with much tighter quota volumes.

Higher Exports to Turkey, However, Are Not an Option

Turkey is another major export destination for Russian mills and the country imported 3.4 Mt of Russian steel in 2019—mainly sheet products. Such high imports create strong competition for Turkish producers in their domestic market. The recent state of the economy and political instability caused end-user demand to fall, reducing opportunities for Russian exporters, and the Covid-19 outbreak has diminished these even further.

Although we expect Turkey to recover at a faster pace from Covid-19 compared with other European countries, this recovery comes off a lower base as the country emerges from recession. However, Turkey itself is an important supplier of steel to the EU and limited export opportunities there—now further reduced following the quota revision—are already causing Turkish mills to run at lower capacity utilization rates.

Within this poor demand and constrained trade environment, we expect Turkish steel demand to be mainly served by domestic production as mills will likely lower their prices, undermining the potential attractiveness of the market for even low-cost imports.

Growth in Russian Export to be Supported by Strong Asia Demand

Asia has become an increasingly important export destination for Russia from 2016 onwards, as other markets implemented protective measures that affected Russian exports (e.g. U.S. S232, antidumping duties in the EU) and, in 2019, exports to Southeast Asia rose to over 5.5 Mt. This export performance was helped by both the rapid growth in steel demand in Asia but also oil price falls that made freight cheaper, thus rendering Russian material more price competitive.

Another reason behind the rapid growth in exports to Asia is lower competition from China—previously the primary exporter to this market. China’s reduced cost competitiveness, a strong domestic market and supply-side reform of its steel sector reduced Chinese export volumes, helping Russian—and Indian—mills gain a higher market share.

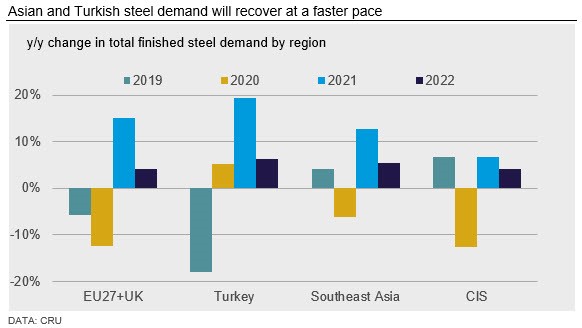

Currently, Southeast Asia is a desirable market for many producers globally, including Russia, as demand there appears to be recovering faster than in Europe or Turkey. However, competition among exporters to the region is likely to rise as both traditional suppliers to Southeast Asia, such as Japan, and newer ones, such as Russia, are experiencing problems in their domestic markets and are thus looking to expand sales. Despite the fierce competition, Russian producers that are very cost competitive are in a good position to secure market share in the region and maintain profitability.

In 2020, Russian demand will be low, but production, that reduced by 20 percent in Q2, will increase, partly as the major part of the fall can be attributed to MMK maintenance. As this mill restarts operations, the market will become oversupplied and the question as to whether other mills need to reduce output will depend on producers’ ability to expand exports.

As European demand slowly recovers through 2020 H2, we will see Russia lifting exports to the EU, while exports to the Turkish market will not be an option. The main opportunities for higher exports are to Asia and, due to its costs structure, Russia is in a good position to win a significant market share.

The Russian domestic market weakness, however, is not limited to 2020 and will persist through 2021 and onwards. While Asian demand growth will remain strong, making the Southeast Asian market even more important, opportunities for exports to the EU will be undermined assuming that a carbon border tariff is introduced.

Carbon Border Tariffs Threaten Russian Exports to the EU

The EU Emissions Trading Scheme is fundamentally altering the economics of steel production in Europe, reducing profitability and import competitiveness for EU producers. The EU carbon price has remained resilient in 2020, averaging €22 /tCO2, despite plummeting IP and energy prices.

In this context, the EC is planning to impose a carbon border tax adjustment (CBTA)—a tariff levied on carbon emissions embodied in imported goods into the EU—to “level the playing field” and ensure that imported goods are subjected to the same carbon costs as EU producers. Such measures have significant potential to redraw the competitive landscape and create both threats and opportunities for Russian producers, but the ultimate impact is difficult to predict and substantively dependent on policy specificities.

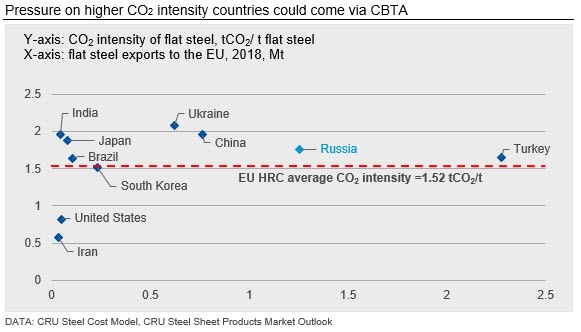

One proposed measure of implementing the CBTA is to charge importers on the basis of a single product wide benchmark. The chart below shows the CO2 intensity of HR coil production for the top 10 exporters to the EU. On average, Russian mills produce HR steel with a higher CO2 intensity than the average EU producer and, if a tariff were applied based on this relative intensity, Russian producers would be penalized overall, but less than exporters from China and Ukraine. Russian producers that can reduce the CO2 intensity of their steel production and/or redirect already low CO2 intensity steel to the EU market could improve their competitive position under this CBTA proposal.

The ability to measure carbon embodied in international metals and mining production is also a key issue and a set of robust technical benchmarks will be required to administrate a CBTA. The granularity and precision of these policy rules will be key in determining the impacts of any carbon-based tariffs. Can such rules accommodate, for example, heterogeneous carbon intensities within markets or will these be determined at the market level? A particularly challenging issue arises in downstream markets (e.g. domestic appliances, vehicles) where feedstocks can be more complex, flexible and opaque. For instance, Russia is a key exporter of semi-finished steel, such as billet, to Turkey, where it is then rolled to finished steel products (i.e. rebar) prior being exported to the EU. The market level determining the tariffs could be the one of the originating semi-finished steel from Russia.

The Speed of Global Demand Recovery Will Set the Tone for Russian Steel Producers

Russian mills sharply reduced output in Q2 through both planned maintenance and lower capacity utilization, which is typical. That is, Russian steelmakers do not usually idle assets—a common way for most producers to reduce output during acute crisis. However, as MMK is scheduled to resume operations, the market will become oversupplied. This could lead to closures by other market players unless exports can be lifted.

We expect that Russia will be able to lift steel exports in 2020 to some extent, increasing from the low levels seen in 2019. Russian mills have some opportunities to increase exports to the EU and could gain a bigger market share in Asia, but other markets, such as Turkey, will be less viable. As a result, we expect Russian net exports to grow by 15 percent y/y in 2020, but this will not be sufficient to sustain Russian output at 2019 levels, thus, in response, we expect that finished steel production will drop by 8 percent y/y.

In the medium term, Russia will face more difficulties. We don’t expect Russian demand to recover to 2019 levels until after 2021, thus, the level of production will be highly dependent on export demand. The possibility of a carbon border tariff into the EU—Russia’s largest export market—from 2021 onwards is expected to reduce the competitiveness of Russian steelmakers if implemented. Another factor is the possible introduction of scrap export restrictions that are also expected to negatively impact the cost position of Russian steel producers.

Having said that, we expect that Russian net exports will grow by 18 percent y/y in 2021, primarily through higher exports to Southeast Asia where the market will continue to grow, adding 13 percent y/y of steel demand according to CRU forecasts. This increase in export volumes will allow Russian output to return to 2019, pre-pandemic levels during 2021.

Additional contributions from Chris Bandmann and Ryan Smith.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com