Prices

February 16, 2020

SMU Market Trends: No Clear Direction for Steel Prices

Written by Tim Triplett

Steel prices finished 2019 on an upward trajectory, giving the market hope for a stronger 2020. That trend proved short-lived, however, as prices stalled in January and February, leaving both buyers and sellers wondering what to expect in the weeks and months ahead.

Steel prices rose in November and December on a series of price hikes by the mills with the benchmark price for hot rolled hitting $610 per ton by early January, up from a low of $470 per ton in October. As of Feb. 11, the price had lost that momentum and backtracked by about $30 per ton. Most of the service center and manufacturing executives polled by Steel Market Update at that time predicted prices would continue to move sideways or decline even further in the near term. By that point, SMU shifted its Price Momentum Indicator from Higher to Neutral on all flat rolled and plate products, waiting for the market to establish a clear direction.

According to SMU’s canvass of the market this past week, spot orders of hot rolled coil had an average price of $580 per ton ($29.00/cwt) FOB mill, east of the Rockies, with lead times of 3-5 weeks. Cold rolled orders were averaging $740 per ton ($37.00/cwt) delivered with 5-8 week lead times. Galvanized was at $770 per ton ($38.50/cwt) with 4-8 week deliveries. Galvalume was slightly higher at $790 per ton ($39.50/cwt) with 7-8 week lead times. The average price for steel plate, with 4-5 week lead times, was $700 per ton ($35.00/cwt).

Which direction will steel prices move from here? That’s the question on steel buyers’ minds. Is today the best time to buy or will steel be cheaper tomorrow?

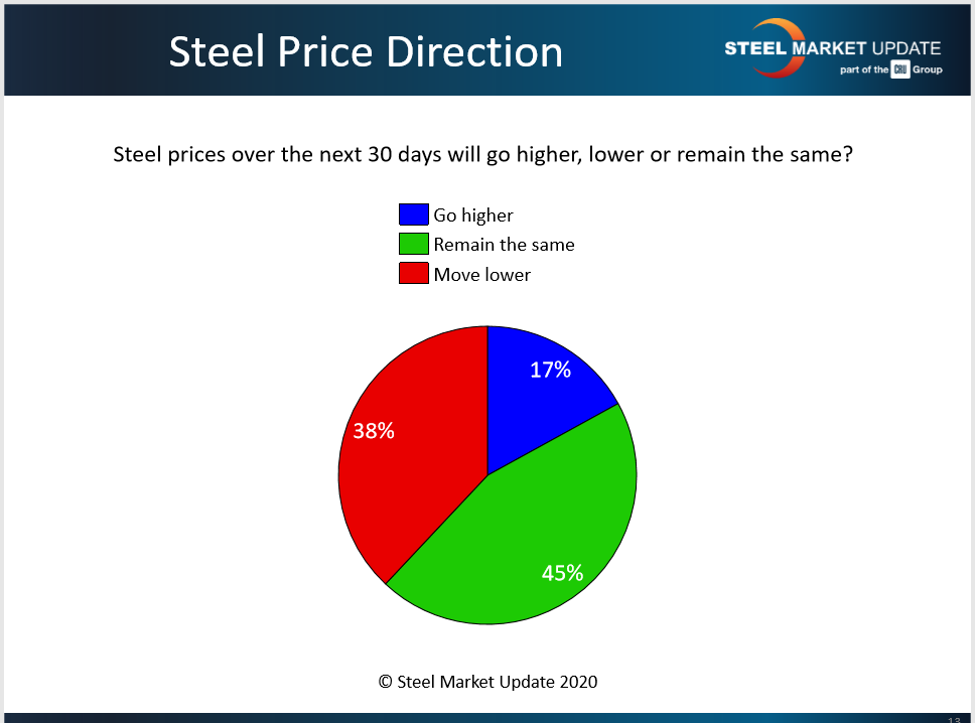

Polling the market in early February, SMU asked: Will steel prices over the next 30 days go higher, lower or remain the same? Forty-five percent of those responding said steel prices would remain the same. Given that steel prices rarely ever remain the same for long, that essentially meant that a near majority of the market opted not to even venture a guess on the direction of steel prices. Thirty-eight percent expected prices to move even lower; just 17 percent higher (see chart). Thus, twice as many of those sharing a prediction expected further declines in steel prices.

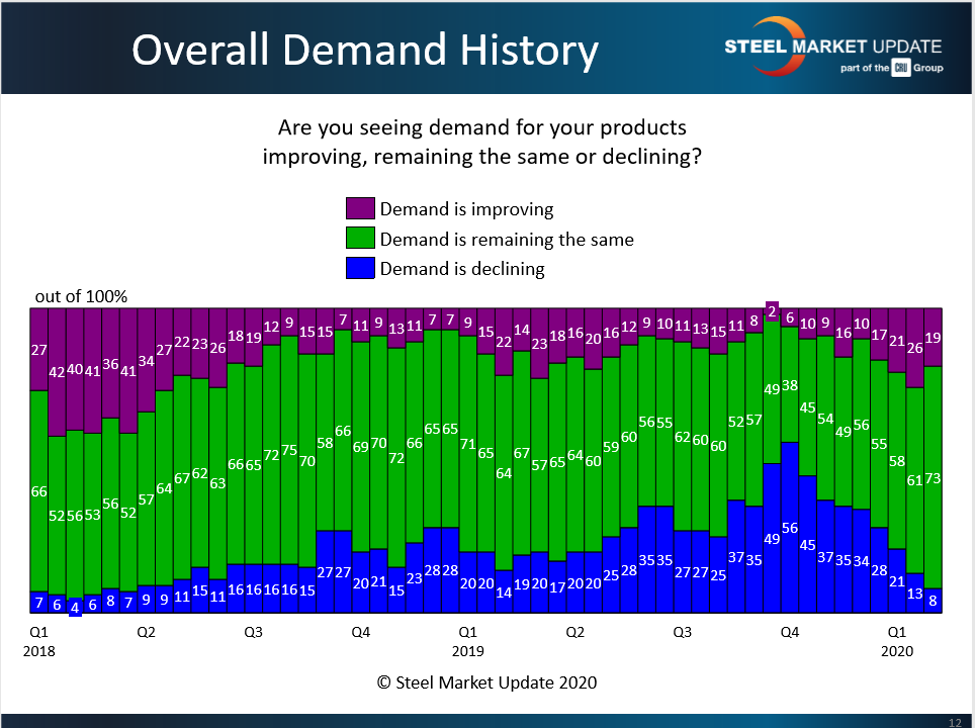

Obviously, steel prices are heavily influenced by demand. SMU asked executives: Are you seeing demand for your products improving, remaining the same or declining? Roughly three out of four steel buyers (73 percent) characterized demand as flat or stable, while 8 percent saw demand from their customers declining. Only 19 percent saw demand improving (see chart). Thus, the flattening of steel prices seemed to mirror the flattening of demand.

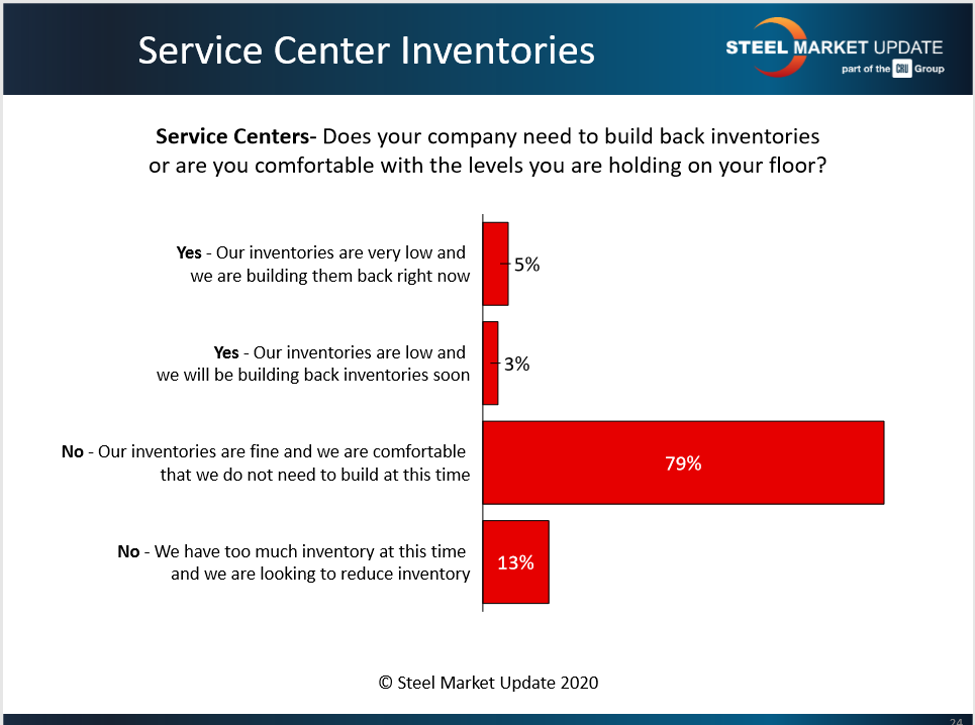

One big component of steel demand is how actively service centers are buying. Polling the distributors, SMU asked: Does your company need to build back inventories or are you comfortable with the levels you are holding on your floor? By far the largest group, about 79 percent, said they are satisfied with their current stock levels, while 13 percent are looking to reduce inventories. Only 8 percent said they were in a buying mode (see chart). Muted demand from the distribution channel has likely contributed to the recent weakness in steel prices.

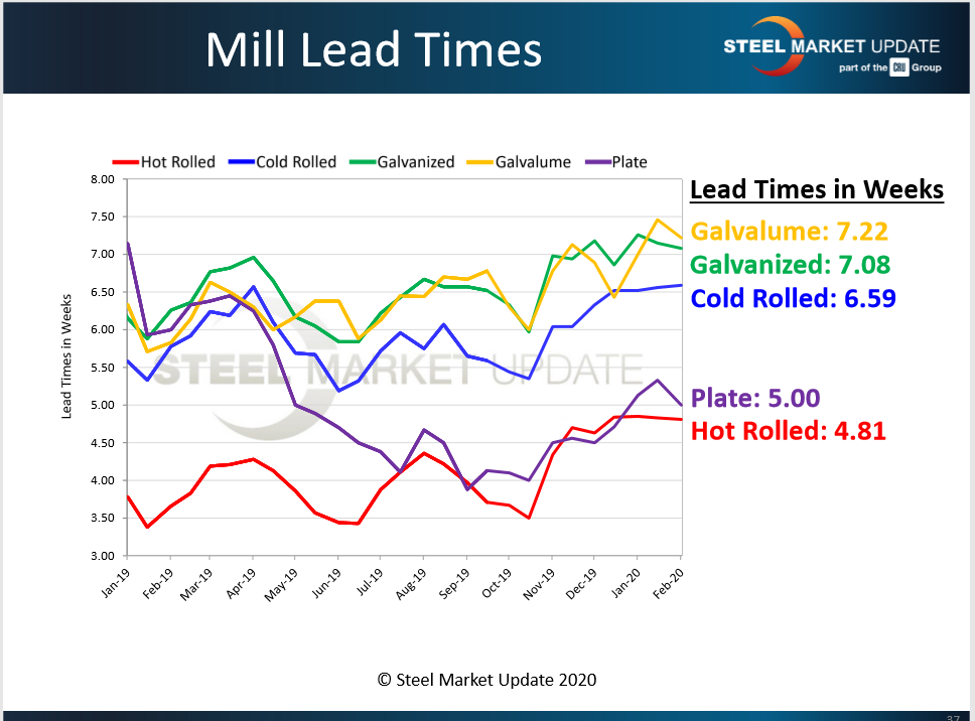

Also unusually flat in recent weeks have been lead times for spot orders from the mills. Lead times for steel delivery are an indicator of demand at the mill level. The longer the lead time, the busier the mill, and the less likely the mill is to negotiate on price. Hot rolled orders had an average lead time of 4.81 weeks in SMU’s latest survey, little changed from the 4.85 weeks in early January. The same was generally true for cold rolled and coated steel products. While the numbers suggest relatively healthy order levels, their lack of movement has made it difficult to gauge the market’s direction (see chart).

Other factors have contributed to the downward pressure on prices. Domestic steelmakers continue to crank out steel at a capacity utilization rate averaging more than 82 percent for the year. Which raises the question: Are they in danger of oversupplying the market? Ferrous scrap prices also declined in February, making it more difficult for the mills to justify higher finished steel prices.

Yet, despite all the market’s uncertainty and the disturbing headlines on presidential impeachment and the deadly coronavirus in China, steel buyers remain fairly optimistic. SMU’s Current Sentiment Index registered +61, while the Future Sentiment Index was at +63—down slightly from January but still very positive compared with six-year lows in the +30s in September and October 2019. Steel buyers still feel pretty good about their companies’ ability to be successful today, as well as three to six months into the future. That prevailing attitude could change, for better or worse, depending on how steel prices play out in Q1 and Q2.

What Steel Buyers are Saying

“Many people in our specific industry (ag and roofing panels) have a good outlook for 2020 based on quotes in the hopper and contracts already signed for building projects in 2020. Hence, I believe most of us are willing to pay smaller increases as we think we are getting ahead of some potentially more aggressive increases as the seasonal demand picks up in Q2.” Manufacturer

“In the immediate term I expect lower prices, but with low velocity. The main question is whether or not we see that trend extend or whether we see a more pronounced drop. Mill output is still pretty robust and holding up at over 80 percent capacity utilization, and January imports were as strong as expected, with an influx of slabs. Demand seems weaker than we (and our customers) expected, so that is a concerning development.” Service Center

“Where prices will go depends on the particular market. HR will go down into the $550s… and a case can be made that we are already there. CR and HDG will directionally follow Houston imports. The HR/CR spread is uncomfortably high; weakness in energy markets considered, the spread will likely remain high. We need oil at or over $60/bbl for the HR/CR spread to begin compressing back to more comfortable levels.” Manufacturer

“It seems like lead times are about the same, but our pre-painted number has risen by $1.00/cwt each of the past few orders. I feel like the pricing will continue to move higher, but I do not get the impression that the increases will be really aggressive.” Manufacturer

“Lead times for coated steel seem to be lengthening somewhat. Supply is fairly tight. Hot roll is still bouncing around six weeks. I think prices will move sideways through February. If scrap goes up in March, we will likely see the mills try to push for another $40/ton.” Service Center

“Lead times are holding. I keep watching for them to decrease, but no visible signs yet. Mills on occasion delay reductions on their lead time sheets, which hides reduced order books. The question remains: How are the mill bookings? Prices are slightly down due to buyer resistance. Consumption is down 15 months in a row, but mills have decent tonnage due to fewer imports.” Service Center

“The mills have some holes to fill. Prices to move sideways to lower. Demand seems to be lower than the mills expected.” Service Center

“Lead times are totally location-dependent. There are some holes at certain mills. Prices will move lower from here; lack of demand.” Service Center

“Lead times vary from steel mill to steel mill. We have from mid-March to April ship dates. It appears that steel prices are starting to move down due to reduced order entry. We are hearing that the pipe and tube mills are backing off.” Manufacturer

“If lead times are an indicator of market strength, then the mills are poised for more increases.” Service Center

“Prices will move sideways to down. Q1 demand was pulled forward with Q4 buys. Scrap is falling. The demand environment overall is stable, but not robust.” Service Center

“Pretty fragile. Mills want about equal to resale for replacement, so if the price doesn’t move up (and I expect flat to slightly down), a current buy requires you to eat the freight. The only thing better than last year is that service center inventory values shouldn’t fall $300/ton this year.” Service Center