Market Data

December 22, 2019

SMU Market Trends: Pricing, Demand, Forecasts

Written by Tim Triplett

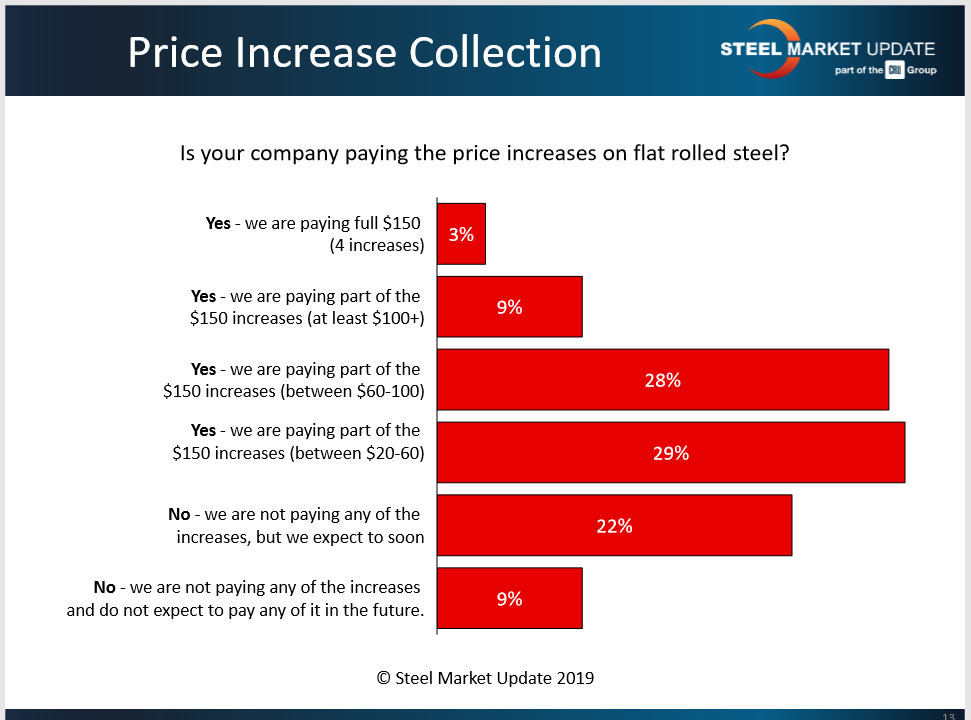

In four rounds of price increases since late October, flat rolled steel mills have raised prices by a total of $150 per ton. How much are they collecting? Some, but certainly not all, according to the service center and manufacturing executives who responded to Steel Market Update’s questionnaire this week.

SMU data places the average benchmark price for hot rolled steel at $570 per ton. That’s about $100 more than the trough in October when the mills announced their first increase.

SMU asked steel buyers—service centers and OEMs—how much of the increased prices they are paying. The consensus appears to be roughly half the $150 total.

About 12 percent said they are paying an extra $100 or more. Twenty-eight percent said they are paying less than $100 but more than $60. Another 29 percent are paying a small increase for steel, from $20 to $60, while about one-third (31 percent) are paying no increase at all, at least not yet.

Buyers are not all happy about the higher prices. “We’re increasingly reliant on imported material,” said one OEM. “I don’t see manufacturers accepting these huge cost increases—maybe half at best. They will fight all the way until it corrects again,” said a trader. Added a service center exec: “As the frequency and size of these announced price increases continues, the market gets numb and the likelihood of collecting them goes out the window. The mills are crying wolf a little too often. The market needs time to digest and settle.”

Demand Helping or Hurting Prices?

Customer demand for steel is unchanged for the majority (55 percent) of the service center and manufacturing executives who responded to SMU’s questionnaire this week. More report demand on the downturn than on the upswing, which is not a positive for mills looking to collect higher prices. About 28 percent of respondents said demand for their product is declining, while just 17 percent said demand is improving.

“We have several customers lowering their forecast for Q1,” commented one service center exec. Another said activity is slowing because first-quarter contract pricing is better than spot. “Demand had been steady but due to trade risk factors, my imports are noncompetitive,” complained one trader.

Nearly all (88 percent) of the service centers surveyed by SMU say they are having difficulty passing along the higher prices to their customers. “The mills are trying for too much too fast. It’s a very irrational strategy that makes people just go to the sidelines and look hard for import opportunities. The domestic steel industry is its own worst enemy. Trump threw them a lifeline and they have done very little with it!” said one distributor. “Many of our customers are also faithful SMU subscribers. They anticipate this type of ‘stop the bleeding’ increases. They also anticipate the mandatory follow-up increases the mills pass in an effort to collect at least a portion of a prior increase. It happens twice per year, every year.” Added another respondent: “We’ll lose the order if we raise the full amount.”

Forecast for 2020

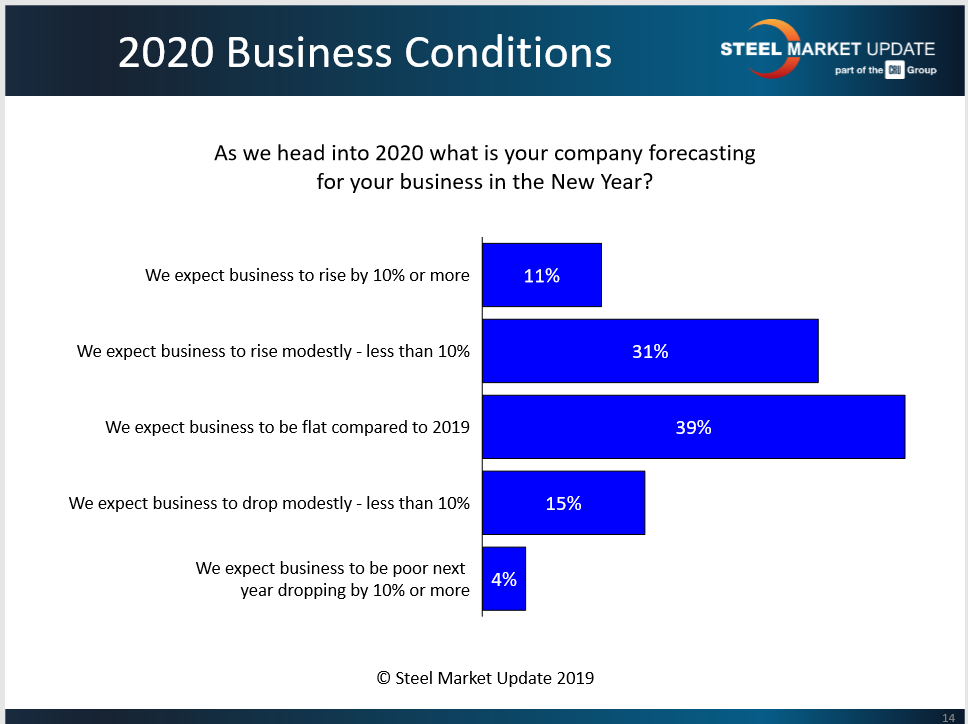

SMU asked: As we head into 2020, what is your business forecasting for the New Year? The results are somewhat bearish. Nearly 60 percent predict their business will be flat or decline next year. Of the 40 percent who see business improving in 2020, only 11 percent expect an increase of 10 percent or more.

Commented one service center executive: “If the mills would stop this wild and irresponsible pricing rollercoaster and let the market settle, maybe some confidence and credibility—and most importantly profitability—would return to our collective markets.” Expressing some optimism, one service center exec said: “With the new Canada/Mexico deal, the new China deal, and the 2020 Infrastructure spending, we fully expect a better year in steel plate fabrication overall.” But one trader remains guarded: “I hope to be flat, but who really knows. Maybe some small increases as I move onto other products and industries.”

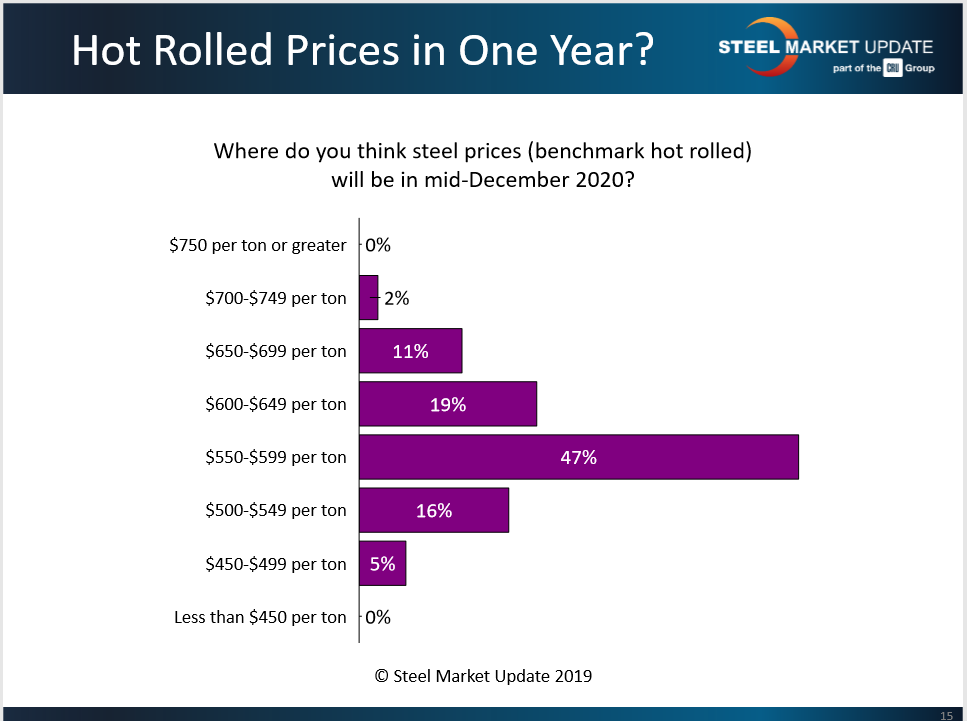

Steel Price Predictions

SMU asked: Where do you think the benchmark price for hot rolled steel will be in mid-December 2020?

While it’s impossible to predict steel prices a year in advance, the consensus view is for the price to fall in the $550-600 range where it is right now. Only about one-third of the respondents are guessing the HR price will be higher this time next year. Wishful thinking, perhaps?