Prices

November 8, 2019

U.S. Steel Exports Dip in September

Written by Brett Linton

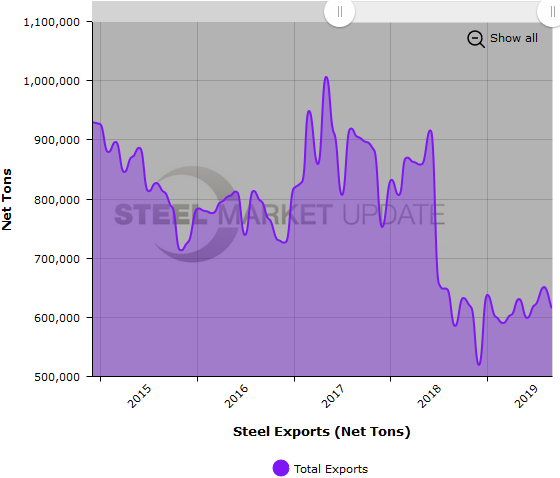

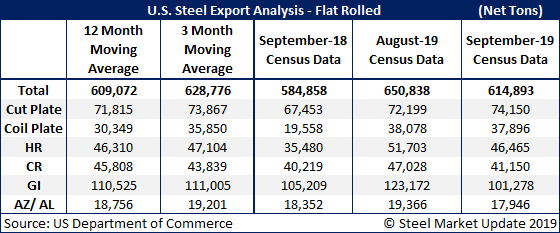

The U.S. exported 614,893 tons of steel in September, according to final Census data, a 6 percent decline from August, but up 5 percent from the same month one year ago.

September exports were right in line with the 2019 average of 615,874 tons, but remain significantly muted compared to recent years. It was just over one year ago when exports dropped from their 850,000+ ton levels down to sub-700,000 levels, as shown in the purple line graph below.

Total September exports were below the three-month moving average (average of July, August and September), but above the 12-month moving average (average of October 2018 through September 2019). Here is a breakdown by product:

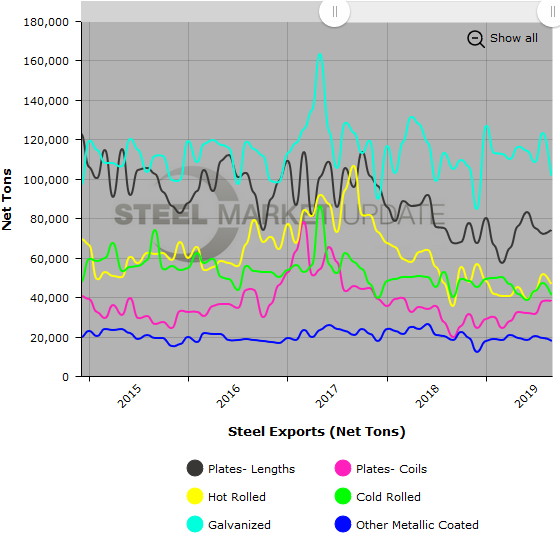

Cut plate exports rose 3 percent from August to 74,150 tons, also up 10 percent compared to one year ago.

Exports of coiled plate were 37,896 tons in September, flat over last month but up 94 percent year over year.

Hot rolled steel exports declined 10 percent over August to 46,465 tons, but were up 31 percent over September 2018.

Exports of cold rolled products were 41,150 tons in September, down 12 percent from August, but up 2 percent over the same month last year.

Galvanized exports decreased 18 percent month over month to 101,278 tons. Compared to one year ago, September was down 4 percent.

Exports of all other metallic coated products were 17,946 tons, down 7 percent from August, and down 2 percent compared to one year ago.

Below are two graphs showing the history of U.S. steel exports, in total and by product. To use their interactive features, view the graphs on our website by clicking here. If you need assistance logging into or navigating the website, contact us at info@SteelMarketUpdate.com.