Overseas

August 6, 2019

CRU: Increasing Trade Tensions Negatively Affect Market Sentiment

Written by Tim Triplett

By Josh Spoores, CRU Principal Analyst

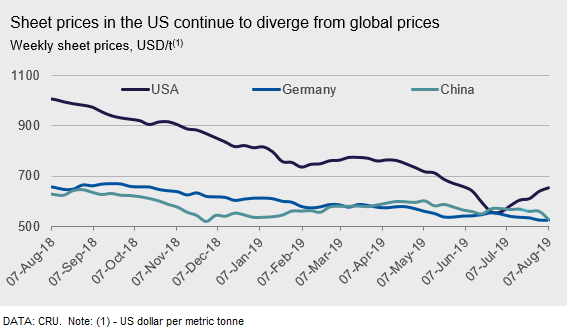

Sheet prices have continued to rise, but the bullish trend is clearly fading. Overall volume of spot transactions last week was the lowest recorded all year. Furthermore, manufacturing is now in recession based on the last two quarters of IP activity, while recent PMI data shows weakness in new orders and production. Additionally, recent order activity since late June was notably large in terms of volume, and with a lack of demand emerging it is likely that sheet inventories will soon need to be worked down.

U.S. West Coast prices remained flat this week, as buyers were comparing Midwest prices to West Coast mill offerings and holding off on purchases. Buyers said the West Coast mills have had more success raising CR and HDG coil than HR coil.

Europe

Sheet prices kept falling in Europe in the past week despite peak holiday season reducing activity levels. Week by week the price falls are small, but they add up—over the past six weeks HR coil prices have fallen by a total of €14 /t in Italy and €18 /t in Germany. It is difficult to see what would change this pattern in the coming month, as demand is unlikely to pick up until the holidays end while raw materials costs are now falling once more. Mills did not manage to pass on the increases in raw materials costs, but that does not mean steel prices will be protected as those costs decline. Margins could simply remain low.

China

Chinese sheet prices started to fall this week following bleak demand and bearish sentiment. On one hand, sheet demand was hurt by weakening manufacturing performance with steel PMI dropping by 0.3 point in July to 47.9. On the other hand, market sentiment was also hit after Trump’s punitive tariffs on another $300 billion in Chinese goods escalated the U.S.-China trade tension. Steel and iron ore futures have plummeted since then, triggering similar movement in the spot market, although transactions have remained limited. In addition, participants were also concerned about a significant loosening of supply restrictions as the upgraded policy this year might make exemptions from production cuts for those producers who met ultra-low emission targets. However, we do not expect a significant loosening of supply restrictions, because steel mills with better emission results that produce higher-end products were granted permission to produce as normal in the past winter period and it should be similar this year. Though with stricter emission targets being set, we expect the amount of these exemptions to be less than in the past. Therefore, we believe the current price correction will be short-lived and the market will return to supply/demand driven trajectory in the coming weeks.

Asia

The imported sheet market in Asia declined sharply last week because of the trade tension between the U.S. and China.

For HR coil SAE1006, Indian mills continued to be the most competitive sources. Last week, offers were in the range of $505-510 /t CFR Vietnam with buying indication at $500 /t CFR Vietnam. However, buying indication dropped further on Friday, according to traders, as it would be now too difficult to sell at 500 /t CFR Vietnam. Chinese materials were offered in the range of $510-515 /t CFR Vietnam for the same grade.

For HR coil SS400, Chinese materials were offered at $515 /t CFR Vietnam earlier last week, then fell to $510 /t CFR Vietnam. As of Monday, stockists said some sellers were willing to accept $505 /t CFR Vietnam, but they would want to monitor the situation.

CRU assessed HR coil prices at $500 /t, CFR Far East Asia, down $10 /t w/w. CR coil prices were assessed at $545 /t CFR Far East Asia, down $5 /t w/w, while HDG prices were assessed at $590 /t CFR Far East Asia, down $3 /t w/w.