Prices

May 16, 2019

SMU Market Trends: Demand Disappoints

Written by Tim Triplett

Although not a disaster, steel demand has fallen short of expectations so far in 2019, contributing to the downtrend in steel prices. The benchmark price for hot rolled steel has declined by double digits since the beginning of the year.

Steel Market Update’s canvass of the market over the past week reveals that many service center and OEM executives are concerned about the auto, agriculture and construction markets in particular, and expect the disappointing demand, and pricing, to persist into the third quarter.

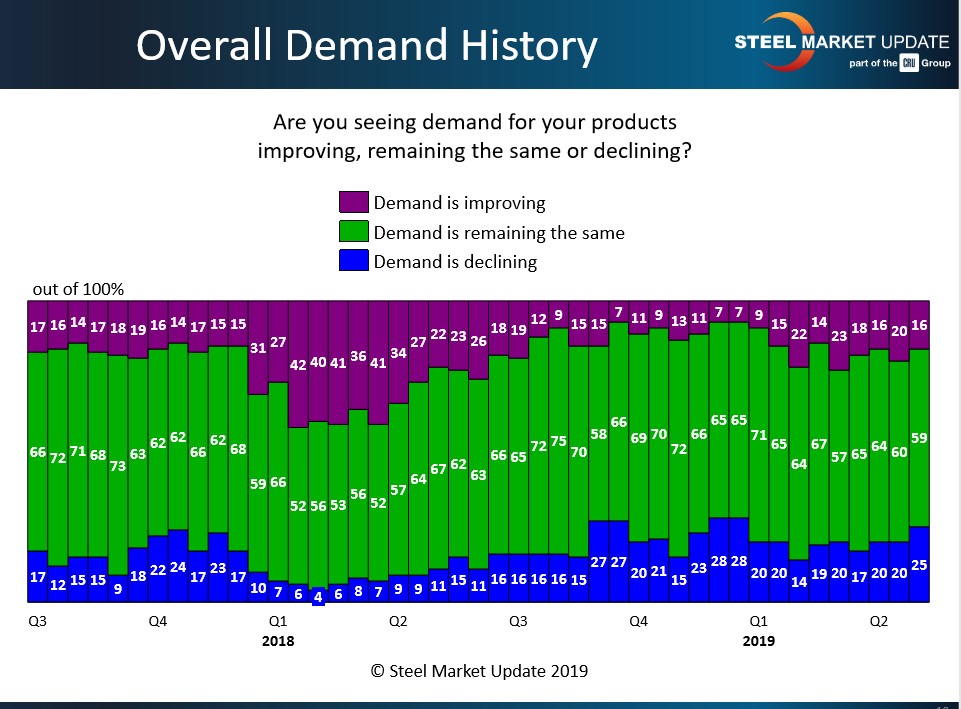

About one-quarter of those responding to Steel Market Update’s market trends questionnaire last week reported that demand for their products is declining. The majority, 59 percent, see flat demand. Only 16 percent see demand growing. “Many customers are not taking the steel they have ordered. Either they are buying it elsewhere at cheaper prices and not fulfilling their commitments or the demand is lower. I suspect the answer falls somewhere in the middle,” commented one respondent. “Some accounts are increasing and some are declining. Seasonal demand is a month behind 2018,” added another.

Polling its sources this week, SMU asked: Where do you see flat rolled and plate prices going over the next two to three months? Following are some insightful responses:

• “We’ve seen weakness emerge in the last 4-6 weeks, following what was a steady level of demand beginning with January. Quite a few companies are being much more cautious in their forward views and planning. Part of this has to do with steel being much more readily available on short notice (mills or wholesalers) and buyers going into hand-to-mouth mode. Unfortunately, reading demand will be all the more difficult now, since it typically gets weaker in the summer.

“Yes, we’re anticipating slowing conditions in the third quarter, and that’s a change in outlook from not that long ago. It’s well known that automotive is pulling back and that’s still winding its way through the supply chain. We’re seeing additional risk factors now weighing on market sectors and companies, in particular the China trade deal not coming to fruition and the threat of yet more tariffs with the Section 232 automotive decision due by May 18. The more uncertainty that gets piled up, the more companies and sectors will pull back and take fewer risks. This phenomenon (trade wars) is something that most likely has not been seen in the career of anyone working today.

“The plate mills are advising that the energy segment is not taking off like they assumed it would. The ag machinery market is poised to take a hit very soon, given all of the challenges facing the farming industry. Automotive’s direction for H2 is very much up in the air, and the Big Three face what will likely be a very contentious labor contract negotiation in September. Lastly, construction has been moving along at a steady but below-expectations pace. The non-residential construction sector has continued to disappoint and not achieved levels that have been predicted for multiple years.

“I think flat rolled and plate prices going down an additional 10 percent from today’s levels is more likely than not. Comments from readers in recent articles have stated that ‘imports are way down.’ However, they’re not really down that much, especially in light of the multiple constraints put in place through trade suits and tariffs. Throw in increased domestic output, falling scrap prices, and questionable demand, and it’s not that perplexing to see why prices are falling.”

• “We are seeing some slowdown in business and expect it to continue into the summer months. As to what the third quarter holds, I don’t have a crystal ball for that far out.”

• “We are down approximately 10-15 percent so far this quarter vs. Q1. We anticipate slowing conditions due to the typical holiday and changeover shutdowns. We are worried about agriculture with all the China noise going on and the financial condition of farmers. I think we’ll see hot rolled down to $600 per ton or close to it by the end of June, then it will bounce sideways for a month, then uptick in late Q3 and Q4 possibly back to $650 levels.”

• “Shipments are down slightly; not a big drop-off, but a little sluggish. We think automotive is slowing and pockets of the agriculture market are down a bit. If the mills keep capacity strong, we see more price weakness coming. Flat rolled and plate prices are heading lower.”

• “Our actual volumes are up from last year, but several of our customers have not reached the forecasted growth numbers they predicted earlier. There does seem to be a general slowing or flattening. Nothing appears horrible, but auto is seeing a slight ebb and construction, although healthy, is not growing. With imports continuing to slow, non-tariff slabs reducing, and several maintenance outages coming in the summer, we’d expect things to bottom out soon, at least temporarily, but don’t know for how long.”

• “We just need the weather to cooperate a little bit better. The fourth quarter is going to be a tough one to rely on agriculture to spend much money for new construction or expansions, although I don’t think we’ll feel that until Q1 2020.”

• “From a manufacturer’s standpoint, our year-to-date numbers are off forecast, although demand has picked up marginally in May. The rainy weather this spring has been a factor; how much remains to be seen. There are still some questions revolving around demand in the second half of 2019. Here in Canada, a stress test for first-time home buyers was put in place late in 2018 to cool down what was considered an overheated housing market. It has had an effect. Although there is still some economic optimism, macro numbers suggest the economy’s leveling off, at best. Supply and demand will take over steel prices. There’s only one direction: down.”

• “Compared to 2018 (and I cringe when anyone compares 2018 to this or any other year) we are down 40 to 80 percent over last May in some cases. Our customers are telling us that quotes are very good and orders are pending, but they’re waiting for things to get settled so people can make good business decisions and move forward. People cannot run their businesses when they feel they are a tweet away from feast or famine, orders or layoffs, investment or pullback. The market needs stability and direction. It seems when the market is uncertain, the pessimists’ drums beat louder and the optimists’ drums go silent. We need NAFTA to be settled. We need China agreements settled. We need an infrastructure bill signed, sealed and delivered this year.”