Product

April 28, 2019

Five Items to Watch to Help Sort Out Pricing Confusion

Written by John Packard

When I was in Atlanta, the questions on the minds of the members of the Association of Specialty Cold Rolled Steel Producers were connected to trying to get a better handle on this market. The questions were less about the direction of flat rolled prices, but rather why are steel prices tumbling with Section 232 in place and the domestic mills running at capacity utilization rates of 83 percent, probably even higher on flat rolled. Add into that mix falling imports of flat rolled and plate steels, and a stronger than projected First Quarter 2019 GDP. Plus the MSCI reported very low inventory numbers at 2.1 months of supply.

So, why are steel prices falling?

The way the steel market works doesn’t always seem to follow the rules of common sense. Sentiment and momentum have always played critical roles. As one of our steel trading friends used to tell SMU, “If prices aren’t going up, they are going down. There is no in between.”

OK, that might be a bit extreme, but it is probably accurate 98 percent of the time. There are those occasional periods when prices move sideways. A good example of that could be seen in plate prices earlier this year. They peaked and just stayed there for a couple of months before finally moving lower.

{loadposition reserved_message}

So, what does Steel Market Update look at, and listen for, as we evaluate the market and where we think prices will move in the coming weeks? Here are five of our own indicators we watch very carefully, and suggest you do the same.

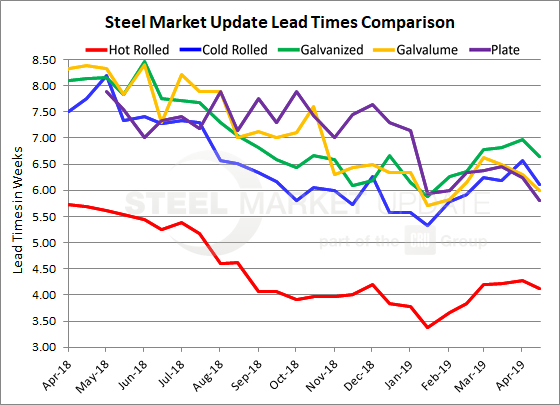

- Lead Times. Lead times are an indicator of the strength of the order books at the domestic steel mills. As you can see from the graphic below, lead times are below year ago levels. For prices to reverse course, the mill lead times need to move out (and they are on most coated products).

- What drives the mill order book? The need by service centers to restock inventories. The SMU Service Center Inventory Analysis completed for the month of March had distributors at 2.7 months of supply of flat rolled. We also captured a rising trend with inventories on order. Without a significant increase in demand supported by shipments, inventories will remain balanced to high, in our assessment muting the amount of steel needing to be purchased. Our inventories data is not available to our members right now. It is only being shared regularly with the service centers who are providing their data to us. If you would like to learn more about how to become a data provider please contact us at info@SteelMarketUpdate.com

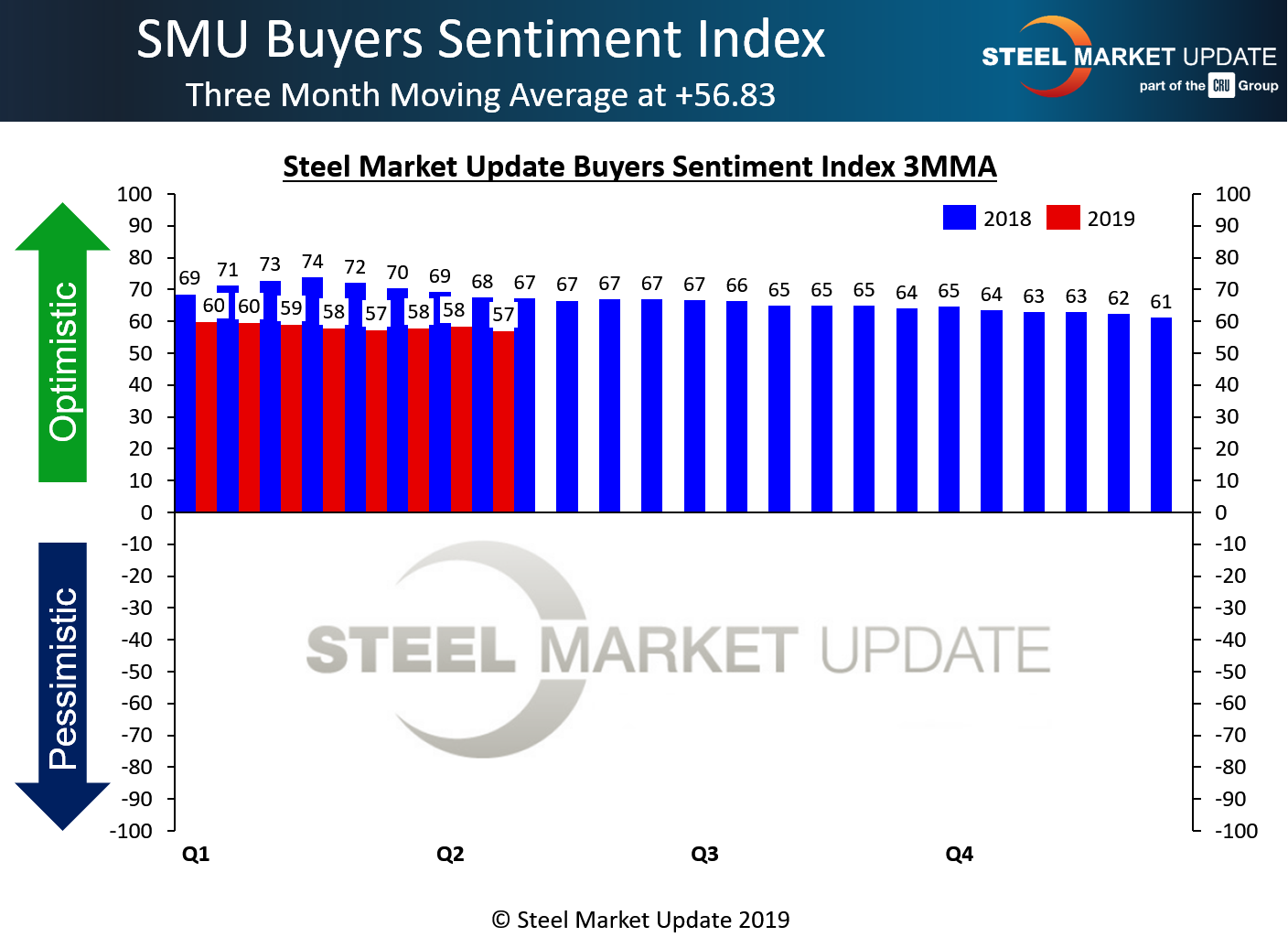

- Sentiment as measured by the SMU Steel Buyers Sentiment Index. Buyers and sellers of steel have been notably less optimistic about their company’s ability to be successful based on current market conditions. It is difficult to push prices higher when you have waning Sentiment.

- Steel buyer commentary supports the waning Sentiment captured during our surveys. SMU canvasses steel buyers daily to better understand how they are reacting to conversations amongst their suppliers as well as their customers. The introduction of new forms of data, such as daily indexing on hot rolled coil, has not helped ease the confusion, but rather has added to it. “Pricing continues to ebb and flow a few dollars every day and the major trade publications are now publishing daily rumors and unconfirmed transactions which lead to even more confusion, but generally supply and demand are in relative balance with future pricing contingent on demand…”–Service center executive. “I think things are getting looser for sure. Lead-times have stalled and have come backwards in some cases. When we consider the myriad maintenance outages being taken between now and June, and we still see lead-times weakening, it portends bigger challenges ahead. Lower scrap prices and still relatively high imports are only adding to the challenges the mills are and will face in the weeks ahead. There’s also newer indications that demand levels may be weakening on a more broad and sustained basis, but it’s difficult to discern whether this is temporary or a more long term issue. Hearing that customers are catching up on past due order books and that future outlooks aren’t as rosy as hoped. The exception remains to be in the Energy sector where large projects are still being consummated, and a number of them on the board for the coming months…”–second Service Center executive.

- Service Center Spot Pricing based on SMU survey. This is another clear indicator of the level of support for domestic steel prices. This should be watched by everyone involved in purchasing or sales of flat rolled steel. We are seeing a clear indication of steel distributors selling off higher priced inventories (another supporting argument for our SC Inventories Analysis mentioned above). This is a sign of building price pressure at the domestic steel mills as they react to their clients complaining of losing orders at lower and lower pricing by their competition (i.e. they must be buying better than we are, therefor Mr. Mill you have to adjust your price to me so I can compete). You can read more about this proprietary product in the next article in tonight’s edition of Steel Market Update.

These are just five items of the dozens Steel Market Update watches on a daily, weekly and monthly basis.