Prices

March 24, 2019

SMU Market Trends: Concerned About Steel Prices?

Written by Tim Triplett

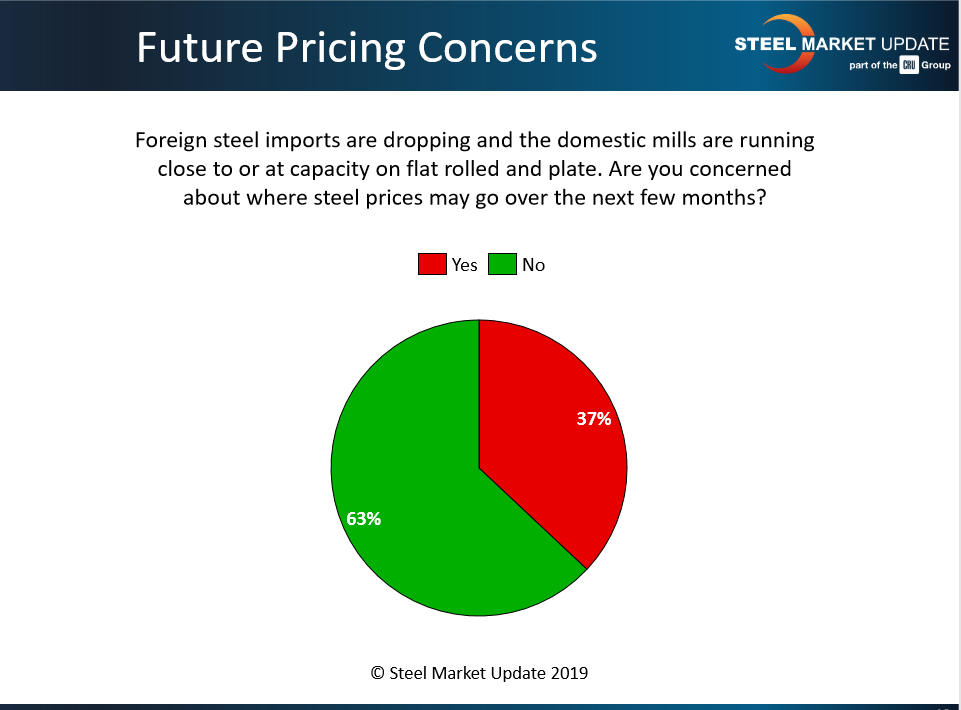

Steel Market Update asked: With steel imports dropping and domestic mills running close to capacity, are you concerned about where steel prices may go over the next few months? Surprisingly, nearly two out of three respondents to SMU’s market trends questionnaire earlier this week said they are unconcerned about a big swing in prices. Their comments—organized below from the perspective of service centers, manufacturers and traders—do show some worry about weakening demand, the staying power of the tariffs and what would happen in the event of a disruption to domestic production.

Service Centers/Distributors:

“I’m not concerned unless the tariffs come off.”

“I don’t think current steel demand will impact pricing over the next few months.”

“I believe prices will remain stable. Imports are the great equalizer.”

“As long as domestics stay under the import price plus tariffs, they can enjoy a captive market. I still doubt service centers are going all in on foreign after the margin rout we all took in Q4 ’18 and still in Q1 ’19.”

“I think the mills have taken steady orders since late January, that lead times are consistent, and that demand will also be consistent (not high or low) as the mills have been busy in February and March. If service centers placed large contracts early this year, then the coming months could see occasional spikes in spot buys, but not a sudden long-term surge in demand.”

“Mills operating at 83-85 percent capacity utilization still leaves a lot of room unless they have been lying about the capacity anyway.”

“I believe we need a longer period to evaluate the mill capacity numbers that have been kicked around.”

“If prices start to go up again, imports will find their way into the market. Demand is steady, but not increasing. There’s not likely to be a shortage.”

“The lack of imports is keeping the market from falling further, but I am concerned that demand, in automotive especially, is declining. So, I don’t see disruption unless there is an unforeseen event.”

“There’s plenty of steel domestically barring a blast furnace explosion.”

“We are one major mill or furnace outage away from a real spike in prices.”

“I’m not concerned as prices on plate will stay around current levels during 2019.”

The tariffs are helping to keep prices up to some degree, but demand is declining and supply is increasing.”

“There’s significant risk that domestic prices will enjoy only a temporary uptick and then recede again if Section 232 is removed from Canada and Mexico.”

“We see demand slowing down, so steel prices may only see small increases.”

“We are seeing the mills attempt to collect increases while demand feels weak. That doesn’t usually end up working.”

“I’m always concerned, as that’s my job, but I don’t think anything dramatic is going to happen in the next three months.”

“With all the tariff uncertainty and drama, we’ll be a moving target.”

“It’s simple supply and demand. The steel mills in the U.S. are famous for feast or famine. How about an operating cost that allows everyone to be profitable all year round?”

OEMs/Manufacturers:

“I’m not overly concerned. There seems to be enough foreign options for light-gauge galvanized to keep prices stable for the short term.”

“Prices will rise the next few months, peak, then start falling again.”

“There’s lots of availability at the moment in Canada and if the tariffs get removed there will be even more availability in Canada.”

“We’re hearing from many people that demand overall is sluggish. I think it’s more about the underlying demand than the supply side. We’ve seen the supply side push increases over the last few years, which then crash when demand reality sets in.”

“The price shock related to the Vale accident will have subsided. Scrap prices will lower from better collection activities.”

“If demand jumps, there’s the risk of increases sticking. If the demand is lackluster, and new capacity is brought on line, they will buy their way into the market.”

“It will be a short-term rise. Prices will normalize once third-quarter imports resume.”

“We’re always concerned about price increases. The closer the mills get to capacity, the higher the price will be.”

“Section 232 distorts the market and disadvantages steel-consuming manufacturers. Pricing will stay high or go up further, not based on market conditions but on price coordination between steel suppliers in a protected industry.”

“Mills said they were full 8-9 months ago and used tariffs and a shortage of foreign steel to raise prices. If the price rises too much, foreign mills will re-enter our market and compete with domestic mills even if they pay tariffs.”

“Foreign will pick up any overflow. Pricing will be at or below domestic to get the orders.”

“Our industry cannot continue to pay more for steel. We sell nice-to-have products, not got-to-have products.”

“I think movement in pricing will happen at some point, but unless demand rises it shouldn’t be a large increase or decrease.”

“It will continue to be this game where the mills keep pushing the prices as high as they can without making the foreign market tempting.”

“Import pricing is not attractive at all. I’m getting concerned about supply heading into the summer. With mills at 84 percent capacity, we may see a supply shortage driving prices up into the summer. It all depends on demand, which is not great at the moment. It will take a few weeks to see if that is truly due to the weather.”

Trading Companies:

“Reaction to lower imports has been slower than I forecasted. It’s inevitable as the weather improves that we will have a situation that supports increased prices.”

“Domestic mills will get bullish in the short term and raise prices, but the doors will open for foreign as internationally most markets are soft. Imports will be readily available and start flowing in again in the third and fourth quarters.”

“It’s a price roller coaster. I see increases in the short term in the second and third quarters, then a potential crash in the late third and fourth quarters, depending on Section 232 with Canada and Mexico.”

“Domestic lead times remain at more or less normal levels. Given the domestic mills’ fight for market share, prices will come under pressure once demand tails off. Import is a non-factor to overall market pricing.”