Prices

January 3, 2019

November Raw Steel Production: Utilization Rate at New High

Written by Brett Linton

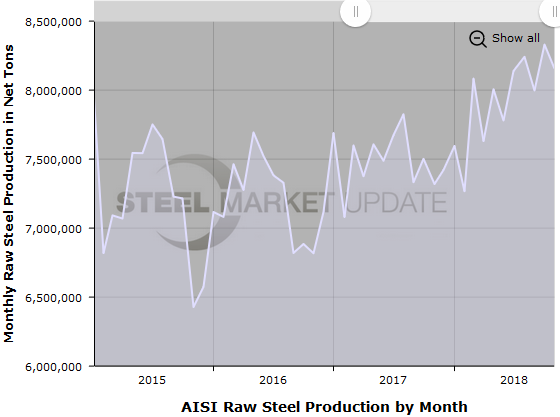

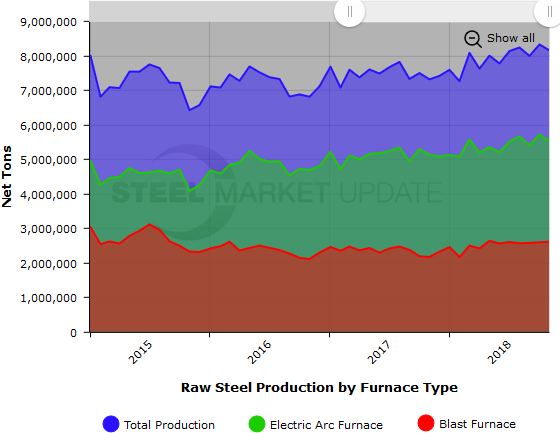

Total raw steel production for the month of November was 8,156,077 net tons. Broken down by production method, 5,533,449 tons (67.8 percent) were produced by electric arc furnaces (EAFs) and 2,622,628 tons (32.2 percent) were produced by blast furnaces. November production was 174,428 tons or 2.1 percent lower than October, but 836,610 tons or 11.4 percent higher than the same month last year, reports the American Iron and Steel Institute in Washington. AISI’s monthly estimates are different than the weekly estimates we report; the monthly estimates are based on over 75 percent of the domestic mills reporting versus only 50 percent reporting for the weekly estimates.

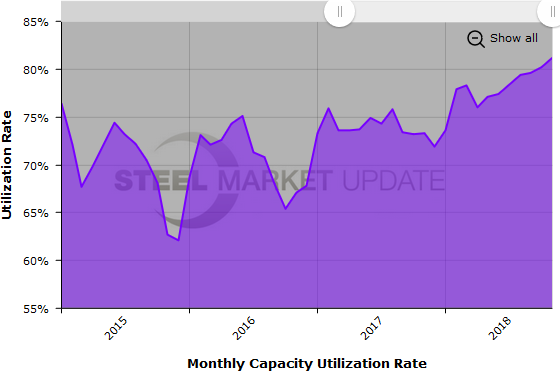

The mill capacity utilization rate for November was 81.2 percent, up from 80.2 percent in October, and up from 73.3 percent one year ago. This is the highest monthly production rate tracked by SMU in the past nine years, with the next highest level occuring in April 2012 when 8,629,531 tons were produced at a capacity utilization rate of 80.9 percent.

The chart below shows total monthly steel production (blue) broken down by electric arc furnace production (green) and blast furnace production (red).

SMU Note: Interactive versions of the raw steel production graphics above can be seen in the Analysis section of our website here. If you need assistance logging into or navigating the website, contact us at info@SteelMarketUpdate.com.