Prices

July 17, 2018

SMU Price Ranges & Indices: Sideways or Modest Gains

Written by Brett Linton

We saw either sideways or modest gains in flat rolled steel pricing this week. Lead times continue to be extended by historical standards and, of course, the 25 percent tariff on most of the foreign steel coming into the United States continues and it does not appear it will be withdrawn at any time soon. We live in interesting times.

Here is how we see prices this week:

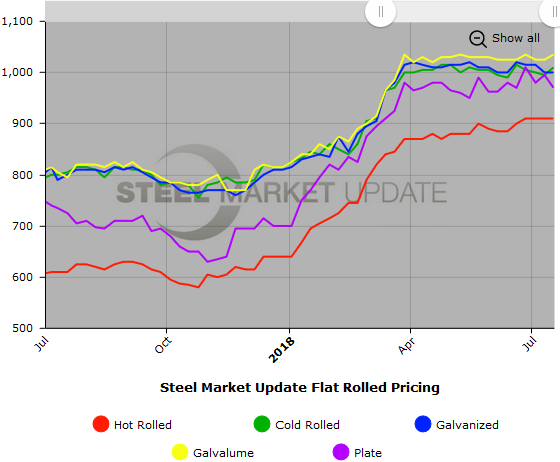

Hot Rolled Coil: SMU price range is $890-$930 per ton ($44.50/cwt-$46.50/cwt) with an average of $910 per ton ($45.50/cwt) FOB mill, east of the Rockies. The lower end of our range fell $10 per ton compared to one week ago, while the upper end rose $10 per ton. Our overall average is unchanged compared to last week. Our price momentum on hot rolled steel is Neutral meaning the product is potentially in transition. We are not predicting which way prices will move over the next 30 to 60 days. Our initial expectation is for prices to move sidewise over the short term.

Hot Rolled Lead Times: 4-8 weeks

Cold Rolled Coil: SMU price range is $980-$1,040 per ton ($49.00/cwt-$52.00/cwt) with an average of $1,010 per ton ($50.50/cwt) FOB mill, east of the Rockies. The lower end of our range rose $20 per ton compared to last week, while the upper end increased $10 per ton. Our overall average is up $15 per ton compared to one week ago. Our price momentum on cold rolled steel is Neutral meaning the product is potentially in transition. We are not predicting which way prices will move over the next 30 to 60 days. Our initial expectation is for prices to move sidewise over the short term.

Cold Rolled Lead Times: 5-10 weeks

Galvanized Coil: SMU base price range is $47.50/cwt-$52.50/cwt ($950-$1,050 per ton) with an average of $50.00/cwt ($1,000 per ton) FOB mill, east of the Rockies. The lower end of our range fell $10 per ton compared to one week ago, while the upper end rose $10 per ton. Our overall average is unchanged compared to last week. Our price momentum on galvanized steel is Neutral meaning the product is potentially in transition. We are not predicting which way prices will move over the next 30 to 60 days. Our initial expectation is for prices to move sidewise over the short term.

Galvanized .060” G90 Benchmark: SMU price range is $1,036-$1,136 per net ton with an average of $1,086 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 5-12 weeks

Galvalume Coil: SMU base price range is $51.00/cwt-$52.50/cwt ($1,020-$1,050 per ton) with an average of $51.75/cwt ($1,035 per ton) FOB mill, east of the Rockies. Both the lower and upper ends of our range rose $10 per ton compared to last week. Our overall average is up $10 per ton compared to one week ago. Our price momentum on Galvalume steel is Neutral meaning the product is potentially in transition. We are not predicting which way prices will move over the next 30 to 60 days. Our initial expectation is for prices to move sidewise over the short term.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1,311-$1,341 per net ton with an average of $1,326 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 6-11 weeks

Plate: SMU price range is $940-$1,000 per ton ($47.00/cwt-$50.00/cwt) with an average of $970 per ton ($48.50/cwt) FOB the customer’s facility for orders to be delivered during the month of September. This is the first time we specified the exact month of delivery and that may have thrown off some of our data providers, so we are not overly concered about our average dropping this week. We are of the opinion that ultimately we will have a stronger number in the future. The lower end of our range fell $30 per ton compared to one week ago, while the upper end fell $20 per ton. Our overall average is down $25 per ton compared to last week. Our price momentum on plate steel is for higher prices once the mills open their October order books. The plate mills are on controlled order entry and are expected to remain that way over the next 30 days or longer.

Plate Lead Times: 4-9 weeks, allocation/controlled order entry

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, Galvalume, and plate price history. This data is available here on our website with our interactive pricing tool. Note that plate prices are not yet available on our website, but we are in the process of adding that dataset. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or 800-432-3475.