Market Segment

November 5, 2014

The Evolution of US Steel Production

Written by Peter Wright

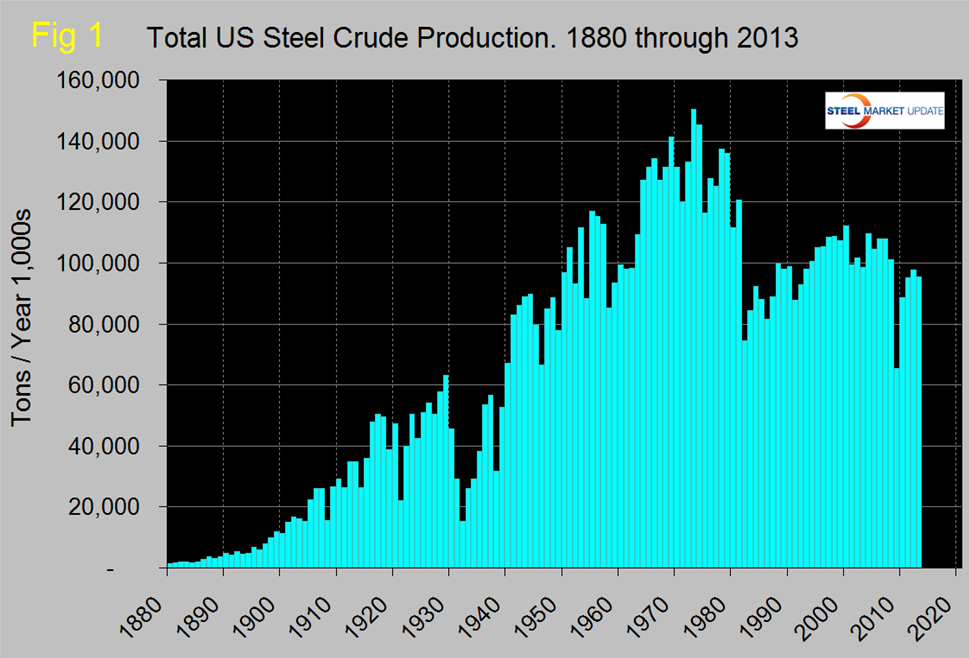

The World Steel Association published its 2014 statistical year book this week with data through 2013. Figure 1 shows total crude steel production in the U.S. since 1880 in short tons. The peak production was 150,483,000 tons in 1973. The final total for 2013 was 95,566,000 tons, down by 2.05 percent from 97,565,000 in 2012. In 2013, 98.8 percent of total steel produced in the US was continuously cast up from zero in 1970. Continuous casting has been the first of three revolutions in steel in the last four decades.

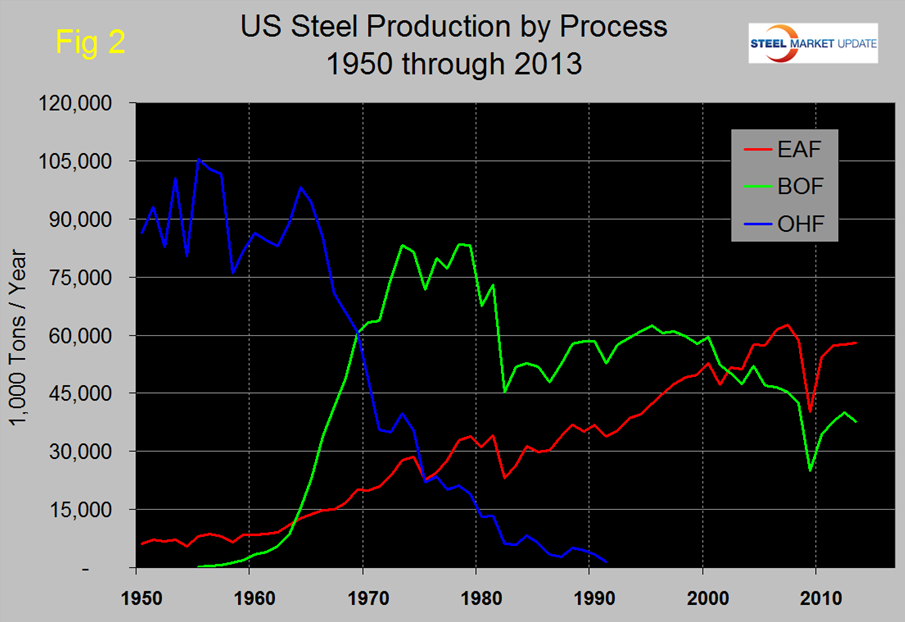

The second revolution was the evolution of the steel making process. Figure 2 shows the mix by process since 1950. The last open hearth furnace was shut down in the US in 1991, though in 2013 Russia and Ukraine still produced 10,653,000 tons by this process. In 2013 EAF furnaces produced 57,905,000 or 60.6 percent of the total. Basic oxygen furnaces produced 37,661,000 tons. 2002 was the first year that the tonnage of liquid steel from EAFs exceeded the BOF process.

In 2013 the US produced 95,223,700 tons of hot rolled products down by 0.6 percent from 2012, imports of semi-finished in 2013 were 7,301,800 tons. Of the hot rolled production 6,960,800 tons was plate, 21,557,800 tons was hot rolled sheet and strip, 19,361,100 was other metallic coated and 2,054,800 was tin mill products.

The third revolution in steel was the introduction of thin slab casting at Crawfordsville in 1995. This development was the single most significant driver of EAF production since that time. This is an ever changing and dynamic industry. As a result of the three revolutions, through process yield was increased from around 75 percent in the early 80s to the mid 90 percent range today and between 1950 and today total energy consumption was reduced from 45 million BTUs per shipped ton to 15 million BTUs.

This article was written by Peter Wright of Steel Market Analysis and one of the instructors for our SMU Steel 101: Introduction to Steelmaking & Market Fundamentals workshop. Peter is a metallurgist and expert in long products, marketing and market/economic analysis. Our next Steel 101 workshop will be held in Mount Pleasant, South Carolina adjacent to Charleston, SC as well as Berkeley, South Carolina which is where we will tour the Nucor Berkeley steel mill. The Nucor mill has a thin slab casting process that Peter wrote about above. Registration is open for the January 20 & 21, 2015 workshop on our website or you can contact our office at: 800-432-3475.