Market Segment

June 19, 2014

Canadian Service Center Shipments and Inventories in May

Written by Brett Linton

Canadian shipments for all steel products in the month of May were 509,700 net tons, an increase of 2.7 percent from the month before, but a decrease of 1.0 percent from May 2013. Inventories at the end of the month stood at 1,384,900 tons, down 3.3 percent from last month and down 9.0 percent from the same month one year ago. The daily average receipt rate for May was 22,097 tons (21 day month), up from 21,682 tons the month before (21 day month). Total May receipts were 6,800 tons higher than the April figure. According to the MSCI, total months on hand stood at 2.7 months.

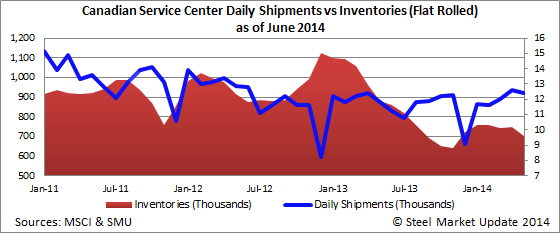

Flat Rolled

Canadian shipments of flat rolled products for the month of May were 259,700 tons, a decrease of 2.0 percent from the month before, but an increase of 0.1 percent from the same month one year ago. Inventories at the end of the month were 701,700 tons, down 6.1 percent from last month and down 20.2 percent from the same month one year ago. The daily receipt rate for May was 10,237 tons, down from 12,914 tons the month before. Total tonnage received was 214,400 tons, down from 271,600 tons the month before. Flat rolled inventories stood at 2.7 months at the end of May.

Plate

Canadian shipments for plate products in the month of May were 96,400 tons, an increase of 13.1 percent from the month before, but a decrease of 2.6 percent from May 2013. Inventories at the end of the month were 259,700 tons, a decrease of 2.6 percent from last month, and a decrease of 0.9 percent from the same month one year ago. The daily average receipt rate for May was 4,273 tons, back up from the 1,716 tons the month before. Plate inventories stood at 2.7 months at the end of May.

Pipe and Tube

Canadian shipments for pipe and tube products in the month of May were 55,200 tons, an increase of 3.8 percent from the month before, but a decrease of 4.1 percent from the same month last year. Inventories at the end of the month were 148,200 tons, up 5.4 percent from last month, and up 12.4 percent from the same month one year ago. The daily average receipt rate for May was 2,999 tons, up from 2,729 tons the month before. Total months on hand for pipe and tube inventories stood at 2.7 months.