Market Data

September 19, 2013

Global Steel Production for August 2013: An Analysis

Written by Peter Wright

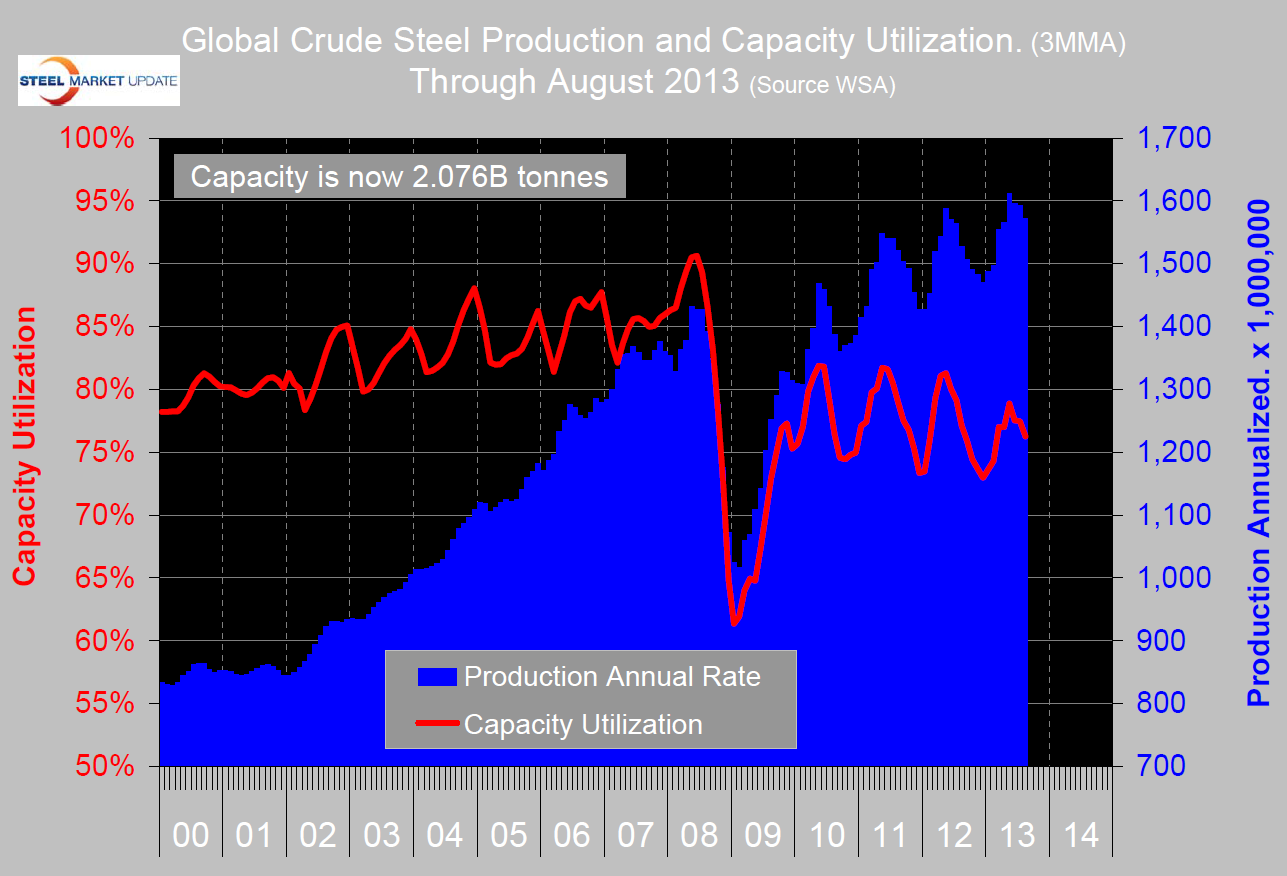

In August China’s steel production exceeded 50 percent of the global total for what we believe to be the first time. Global production in August was 130.352 million tonnes with a capacity utilization of 76.0 percent. In three months through August production was at an annual rate of 1.572 billion tonnes with a capacity utilization of 76.3 percent.

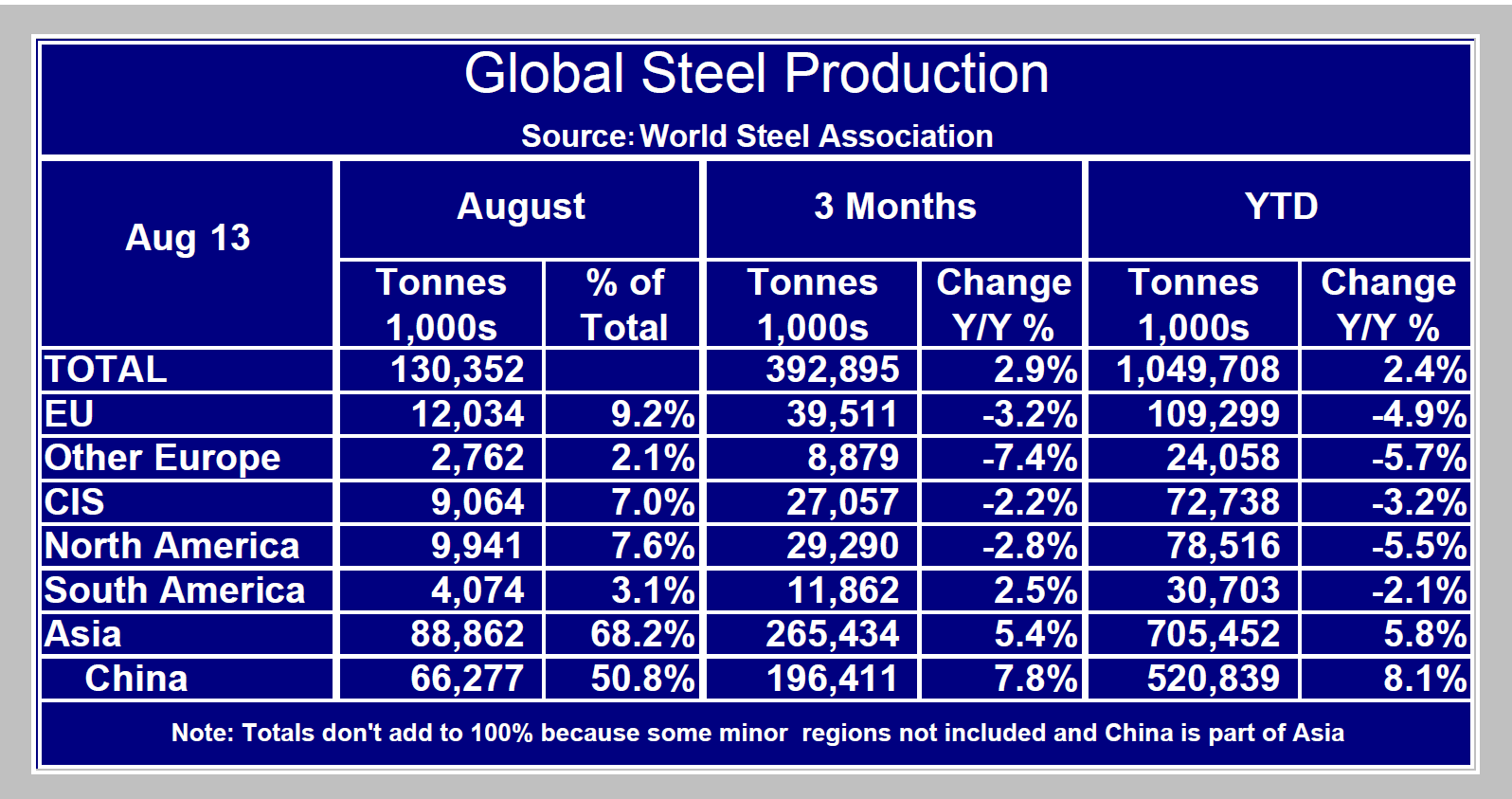

Capacity is now 2.076 billion tonnes (Figure 1). Global production this year is following the same pattern as the last three years by declining in the second half. Global growth in three months through August was 2.9 percent year over year, all regions except Asia and South America declined. Asia was up by 5.4 percent led by China up 7.8 percent. South America was up by 2.5 percent led by Argentina up 182 thousand tons and Brazil up 134 thousand tons. YTD eight months through August global growth was 2.4 percent but in the absence of China global growth was negative 2.7 percent (Table 1).

Capacity is now 2.076 billion tonnes (Figure 1). Global production this year is following the same pattern as the last three years by declining in the second half. Global growth in three months through August was 2.9 percent year over year, all regions except Asia and South America declined. Asia was up by 5.4 percent led by China up 7.8 percent. South America was up by 2.5 percent led by Argentina up 182 thousand tons and Brazil up 134 thousand tons. YTD eight months through August global growth was 2.4 percent but in the absence of China global growth was negative 2.7 percent (Table 1).

On Tuesday this week, the National Association of Manufacturers reported as follows regarding global manufacturing. “The world economy appears to be stabilizing somewhat from weaknesses in the past few months, with the latest data indicating improvements in manufacturing activity in several countries. Europe, which had been in a recession for nearly two years, has now had two straight months of slow—but positive—growth. The Eurozone Manufacturing Purchasing Managers’ Index (PMI) increased from 50.3 in July to 51.4 in August, with growth in new orders, exports and output. Other macroeconomic variables reflecting gains include real GDP and retail sales. Nonetheless, hiring growth continues to lag behind, and from the U.S. perspective, manufactured goods exports to Europe have been lower year-to-date. Industrial production declined 1.5 percent in July, suggesting that significant weaknesses remain even with a more upbeat outlook.

Likewise, China’s economy has also rebounded from recent softness. The HSBC China Manufacturing PMI shifted from contraction (47.7) in July to very slight growth (50.1) in August. This marked the first expansionary figure since April. The Chinese economy has decelerated from past years, with year-over-year real GDP growth of 7.5 percent in the second quarter, down from double-digit rates of growth just a couple years ago. Production, fixed asset investments, and retail sales have also all picked up the pace in July from weaknesses in prior months.

The higher levels of activity in China have helped to boost much of the rest of Asia, as well. While several Asian countries continue to contract, they are also beginning to stabilize. There are some exceptions to this, of course. For instance, India’s economy is suffering from a sharp devaluation in the rupee and its own economic policies. The HSBC India Manufacturing PMI declined from 50.1 to 48.5, its first contraction since March 2009. The other outlier, Japan, increased from 50.7 to 52.2 and has been expanding each month since March, according to the Japan Manufacturing PMI. In general, these gains mirror improvements in the Japanese macro economy since the end of last year.

Despite some better data abroad, the U.S. trade deficit widened in July on higher goods imports and a slight decrease in goods exports. As we have been saying all year, growth in manufactured goods exports have been frustratingly slow in 2013, up just 1.6 percent through the first seven months of the year relative to the same time period last year. This compares to 15.9 percent and 5.7 percent growth in 2011 and 2012, respectively. Exports to China have been one of the bright spots, but other regions have seen some significant easing compared to last year’s pace. Hopefully, as the global economy continues to improve, manufacturers will see demand for their goods increase.”

SMU Comment: The growth of China’s steel industry is apparently greater than their growth in GDP and this in the face of what is supposed to be a restructuring of their economy away from fixed asset investment, (the big steel consuming sector) towards more consumer consumption. This situation continues to bode badly for future US net steel imports.