Beige Book: Majority of districts see modest economic growth

Economic activity across the US increased at a light-to-modest pace in seven of the 12 Federal Reserve Districts, according to the US Federal Reserve’s latest Beige Book report.

Economic activity across the US increased at a light-to-modest pace in seven of the 12 Federal Reserve Districts, according to the US Federal Reserve’s latest Beige Book report.

The US surpassed Japan in annual steel production in 2025 for the first time in 26 years, according to the World Steel Association (worldsteel).

Tariff-related litigation in the US and around the world reflects the willingness of the president to act without consulting Congress or our trading partners. We're seeing the impulse to act without congressional approval in international relations too.

Entering 2026, tin has led a frenzied base metal rally during a historic phase for commodities. Frothy market conditions, driven by volatile investor positioning and shifting macro risk sentiment, pushed several metals—including tin—to record highs in January, before a sharp correction in February.

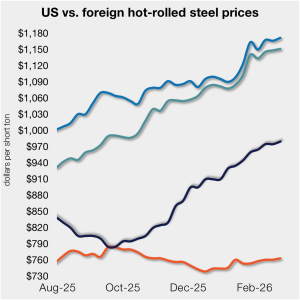

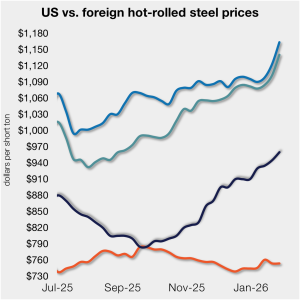

The price gap between US hot-rolled coil (HR/HRC) and landed offshore product remained largely flat again this week, as price movements stateside and abroad mirrored each other.

Leaders of the Steel Manufacturers Association (SMA) and the Canadian Steel Producers Association (CSPA) used this year's Tampa Steel Conference to outline the North American steel industry's central challenges: growing pressures, tariff realignments, and the upcoming USMCA review.

SMU’s Steel Demand Index slipped from earlier in the month, but remains above expansion territory, according to late-February indicators.

The wait for an answer is finally over (sort of). In a six-to-three decision, the Supreme Court invalidated the Administration’s use of the International Emergency Economic Powers Act (IEEPA) to impose tariffs.

On Friday, the Supreme Court released its long-awaited decision on the IEEPA (International Emergency Economic Powers Act) tariffs imposed by president Trump beginning last April. As most of you already know, by a six-to-three majority, the Court ruled against the president.

A look at some of the results of our most recent survey with market participant comments.

The latest 10% tariff is expected to be enacted over the next several days using Section 122.

SMU's Steel Buyers’ Sentiment Indices continue to show that steel buyers are optimistic for their businesses’ chances of success.

Waiting for possibly more changes to tariffs.

Barry Zekelman used his Tampa Steel Conference fireside chat to deliver one of the bluntest assessments yet of the forces shaping North American steel. He warned that a flawed tariff structure and an impending power crunch threaten the industry more than most realize.

The US House of Representatives voted on a resolution on Wednesday, Feb. 11, to disapprove of President Trump's national emergency declaration that led to the imposition of tariffs on Canada.

Last week, news stories (first in the Financial Times) appeared that the Trump administration was working on adjustments to steel and aluminum derivative tariffs. Ostensibly, these tariffs are only imposed on the steel or aluminum “content” of derivative products. But Customs has not provided clear guidance on how to calculate content. Confusion and controversy are running rampant.

Strategic Resources also discussed its project in Quebec, which will include a 4-million-ton/year DRI-quality iron ore pelletizer. It also plans to build a plant to produce DRI, then convert it to pig iron in an EAF.

Hot-rolled coil hovering near $970 per ton could push toward $1,000, but Timna Tanners cautioned at the Tampa Steel Conference that anything “much above that” becomes difficult to sustain. Still, she argued that mills’ slow, disciplined price increases are working in their favor.

Earlier this week, SMU polled steel buyers on an array of topics, ranging from market prices, demand, and inventories to tariffs, imports, and evolving market events.

The price gap between US hot-rolled coil (HR/HRC) and landed offshore product was largely flat this week, as price movements stateside and abroad mirrored each other. Still, the premium for US hot band over imports has remained in a relatively tight band since early December.

President Trump signed an Executive Order (EO) on Feb. 6 allowing the administration to impose tariffs on countries that do business with Iran.

Former smelter sites have become increasingly attractive to data center developers competing for electricity to support AI.

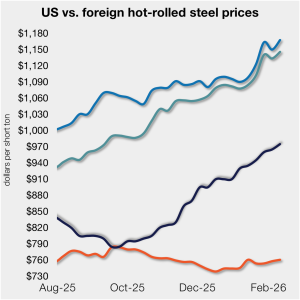

The price gap between US hot-rolled coil and landed offshore product narrowed this week, as price movements stateside and abroad diverged.

The latest Institute for Supply Management (ISM)’s Manufacturing PMI report found manufacturing activity expanded in January 2026. The preceding 26 consecutive months’ reports showed manufacturing activity in contraction.

The Tampa Steel Conference will kick off just a few days after the Super Bowl, and I think it’s fair to say that we could be reacting to market developments in real time – again.

There is no evidence that unofficial talks are taking place to secure tariff reductions on Canadian aluminum or steel. One of the biggest challenges is simply understanding what the US actually wants from Canada.

Tariffs affect different parts of the economy differently. Tariffs on steel imports have contributed to price increases from domestic mills, improving their bottom lines. But orders from customers are slowing down, hurting downstream industries’ profitability and job prospects.

This news item was first published by CRU. To learn about CRU’s global commodities research and analysis services, visit www.crugroup.com. Canada’s Algoma Steel signed a binding Memorandum of Understanding (MoU) with Hanwha Ocean to support Canada’s submarine program and Algoma’s diversification strategy. A new structural steel beam mill may result. Financial support, subject to conditions being […]

A coalition of US steel industry CEOs has formally urged President Trump to maintain—and fully enforce—current Section 232 tariffs on steel and steel‑containing goods.

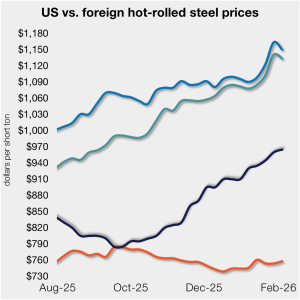

The price gap between US hot-rolled coil and landed offshore product inched higher, even as prices stateside and abroad mostly moved in tandem vs. last week.